I would also argue that finding a way to turn capital into a sustainable income stream is a much more satisfying way to engage with life. If you turned $125,000 in Florida lottery winnings into a 7.33% U.S. government bond, you would be receiving $4,581 payable to you every six months. You could take that money and spend it however you want with the satisfaction that six months later you will receive yet another payment for $4,581. Your consumption shouldn’t result in any guilt because the capital pile will remain for your use even after the consumption.

On the other hand, if you go out and enjoy a couple vacations and buy a nice car and make other expenditures in depreciating personal property, the clock is ticking. If you don’t find a way to replace the capital that you expended, you better enjoy what you just purchased because there will not be more for you in the future unless you come up with a new way to get your hands on more capital. That will require labor and savvy, which makes things a lot harder for yourself than just wielding pre-existing funds intelligently.

We are fortunate that we have options available to us where only modest sacrifices can result in great abundance.

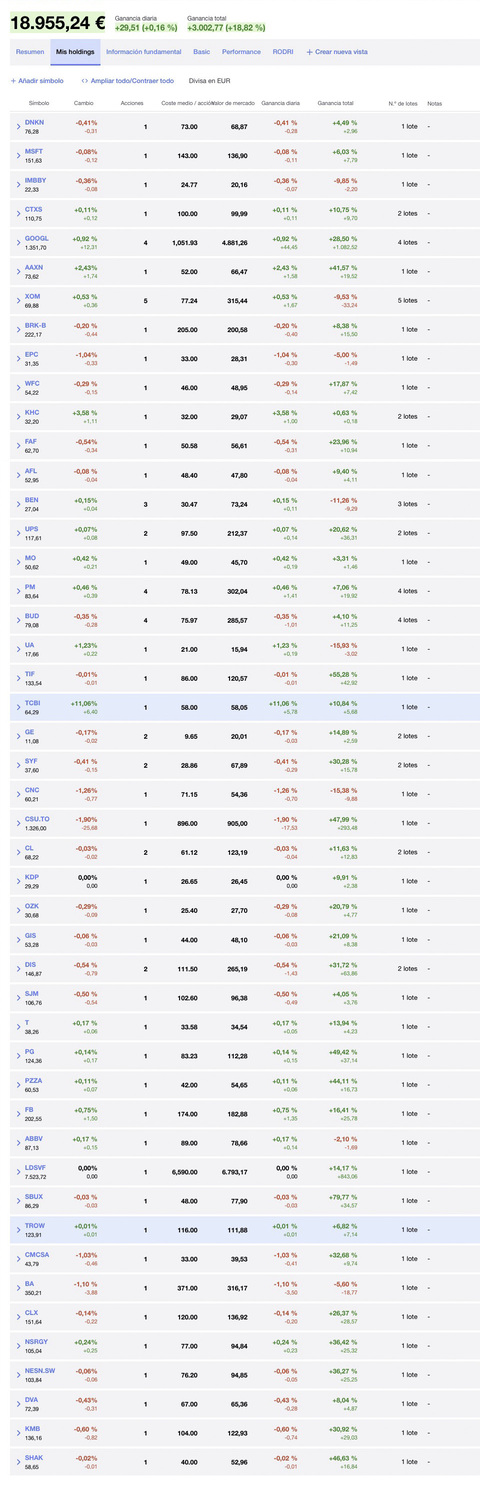

Sigo a McAleenan hace tiempo y me siento muy identificado con su estrategia. Estoy suscrito al sitio web que tiene de pago y he tenido la paciencia de ir anotando cada acción que según él está en compra y el precio al que lo compra (calculándolo más o menos por la fecha en la que escribe cada artículo) y he hecho una lista en Yahoo Finance (poniendo que compra una acción de cada empresa).

Los datos que me salen son bestiales: la primera compra que anoté fue en mayo de 2018, Shake Shack inc. a 40$ está ahora a 53$ (+46,6%). De 47 empresas saca un 18,8% sin contar dividendos, pero por supuesto la fiabilidad 100% no existe y tiene 8 en negativo… Está claro que está en pleno mercado alcista y que hay que ver esto a 10, 20 o más años vista, pero para llevar año y medio no lo hace nada mal.

Si a esa lista le añadiéramos todas las empresas de las que habla en la web pública desde el principio, estoy convencido que a más tiempo aún le saldrá mejor. Que tiene fallos, por supuesto, por eso incide en diversificar, pero que trata las mejores empresas del mundo es un hecho y que mejor para invertir que hacerlo en lo mejor de lo mejor.

Con GE yo no lo tengo muy claro, sigue siendo un gigante pero veo difícil calcular que va a ser de ella, parece que con el recorte de dividendo, la venta de partes de la empresa y finiquitando deuda terminará recuperándose, y aunque seguirá siendo un monstruo de empresa no será ni la sombre de lo que era.

Con Heinz… es verdad que la calificación no es para tirar cohetes y que la empresa últimamente lo está haciendo regulín, pero también es verdad que sigue siendo un gigante alimenticio y que, aunque nos fastidiara a los que nos pilló dentro, recortar dividendo es lo más inteligente que ha podido hacer. Por cierto, llevo una temporada volviendo a ver anuncios de ellos en la TV, algo que parecían tenían de lado, otra buena señal. A eso es a lo que creo que se refiere el cuando habla de Kraft-Heinz, a las posibilidades que tiene a largo plazo, independientemente de lo que digan las agencias de calificación, ya sabemos todos que credibilidad tienen también…

Os pongo la lista de su cartera, no se si se verá bien.

Salu2

The lesson for me is that overvaluation comes in shades. You hear a lot of hand-wringing from investors when a P/E ratio crosses 20x earnings. That is often for good reason, but for a great company with above-average prospects, the dangers don’t really start to manifest until you cross the 25x earnings threshold. At that point, the terms of the investment become “Grow at 12% or greater or I will suffer mediocre compounding.” I’m not saying that Nike will not be a double-digit compounder over the next decade, but if it does, it will require 14% or greater earnings per share growth. That type of hurdle is placed too high for my taste.

Five years from now, Johnson & Johnson will be earning $30 billion in profits and generating $12 per share in profits. It just keeps chugging along at a high single-digit pace and paying out half of its profits as dividends which usually means a 2-3% dividend yield. It is on the short list of ‘Ole Reliables of the investing world. And with Schwab and other brokerage houses eliminating commissions, there is nothing stopping you from accumulating shares every month as you go through life. Considering the overwhelmingly high likelihood of success, the compounding rate at triple the rate of inflation is nothing short of incredible. And it just sits there, waiting for you to combine knowledge with action.

Bueno, eso es como todo, muy personal.

No escribe mucho, un par de artículos al mes y, a veces, se queda solo en uno.

Sus análisis son “muy de andar por casa”, es decir, no te da un sin fin de datos. Te comenta qué está comprando y por qué y hace mención a los datos que le gustan de esa empresa y ya está.

A mi me fastidia que escriba tan poco y que no cumpla a veces ni con el mínimo de dos artículos al mes, pero también tengo que decir que a mi me ha puesto varias veces en la pista de empresas que lo están haciendo francamente bien y que estoy haciendo un seguimiento de su cartera, simulada con Yahoo Financie apuntando cada compra de la que habla y el precio y los resultados no están nada mal.

Si lo que buscas es información de empresas con muchos datos económicos esta suscripción seguramente no sea para ti… De todas maneras leyendo su blog gratuito te puedes hacer una idea de lo que vas a encontrar en el otro.

Espero haberte ayudado.

For you, the lesson to take home is that there can be something of a false security that can be found when searching for sophisticated strategies or brand-name hedge funds. Once you hand your hard-earned money to a hedge fund manager or some other investment selector, there is still a requirement to pick an ultimate investment. More times than not, this means common stock, preferred stock, or bonds. And if you are paying a substantial fee for these investments, there can be even greater pressure to avoid investing in the so-called obvious blue-chip stocks because there can be a human tendency to assume that “complexifying” affairs must carry some wealth-creating benefit for being clever.

Nope! Someone who is quietly investing $300 per month in Johnson & Johnson stock every month like clockwork year after year has, and will continue, to achieve higher compounding rates than the Robert Wood Johnson investment fund.

“Right now, Wells Fargo is yielding over 4% (based upon a stock price of $49 per share). As part of the Fed’s limitations on its capital return policies, namely dividends and share repurchases, Wells Fargo is storing capital at a higher rate that will be unleashed in the future. It is positioning itself for long-term earnings per share growth of 7.5% with dividend hikes accordingly. For a yield that starts at slightly above 4%, high single-digit dividend growth and earnings per share growth over the long-term is likely to be a recipe for 10-12% annual returns. Given that Wells Fargo is already a trillion-dollar bank in terms of assets, that would be a colossal achievement. I expect that a day will come when all the heavy betters on Wells Fargo stock will have a period of sharp outperformance when the investor community wakes up and chooses to recognize that Wells Fargo and JP Morgan are coastal twins and deserve the same valuation.”

“I think the financial side of an investment portfolio can be fully satisfied by stocking up on some of the following: Visa, Mastercard, Discover Financial Services, Wells Fargo, JP Morgan, US Bancorp, and M&T Bank because those companies possess economies of scale and generally entrenched business models that won’t be leaving us anytime soon” The Conservative Income Investor