Fundsmith Equity Fund Annual Letter To Shareholders 2018

Fundsmith Equity Fund manages £14 billion on behalf of some of the world’s largest and most sophisticated wealth managers and private banks, as well as for prominent families, charities, endowments and individuals invested in our fund range, and is focused on delivering superior investment performance at a reasonable cost.

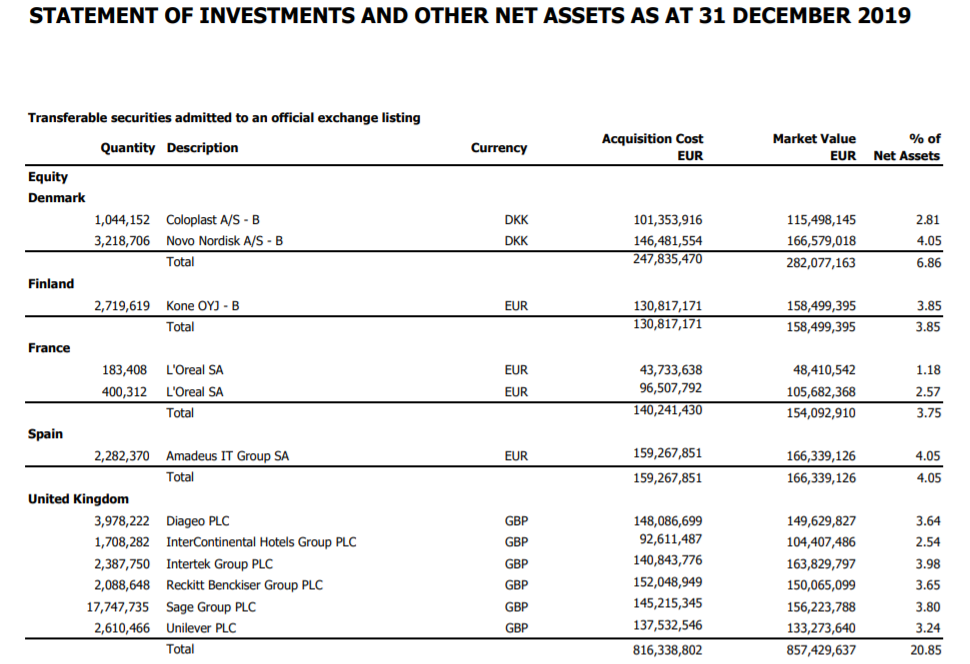

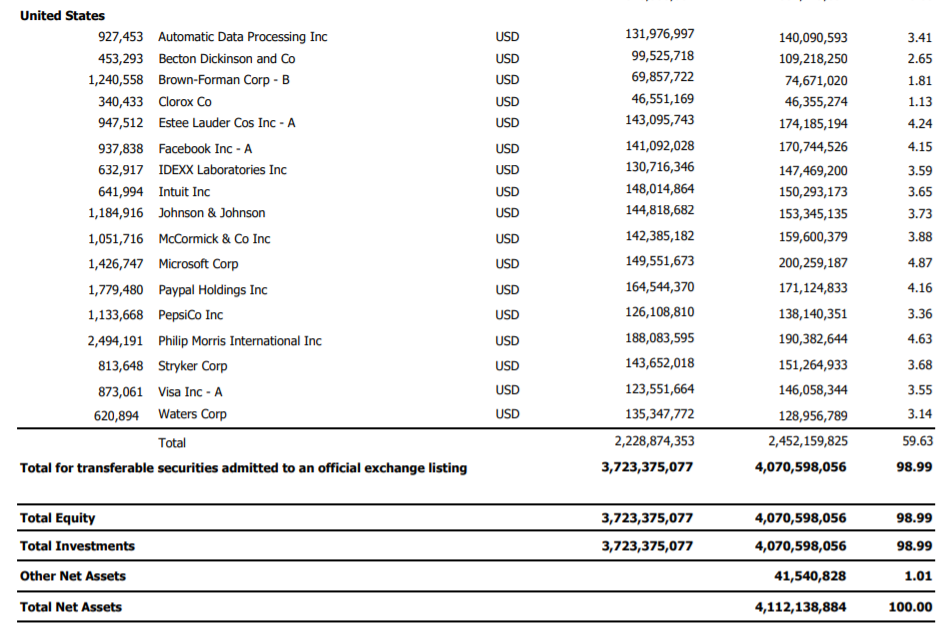

Includes detailed analysis of Fundsmith Equity Fund’s positions in Philip Morris, Facebook, Unilever and Sage Group.

The fund does not adopt short-term trading strategies and will not invest in derivatives, and will not hedge any currency exposure arising from within the operations of an investee business nor from the holding of an investment denominated in a currency other than sterling.

The Fund beat the benchmark MSCI World Index in 2018, and it remains the No. 1 performer since its inception in the Investment Association Global sector by a cumulative margin of 13 percentage points over the second best fund and 188 percentage points above the average for the sector, which has delivered +81.9% over the same time frame.

Curioso que Terry Smith no haya sido capaz de replicar el exito de Fundsmith en los mercados emergentes. En su presentacion a inversores siempre recalca que las empresas que tiene en su fondo emergente tienen mas calidad (mayor ROCE, mayor crecimiento, mejores perspectivas a LP) que las de Fundsmith.

Y es que es muy dificil ganar dinero si tu mercado no esta de moda, sea emergentes, tabaco, midstream, value, small caps UK o lo que sea incluso aunque seas Terry Smith

Buena toña se ha metido Terry Smith en Ambu en su fondo Smithson. Lo de comprar quality stocks a cualquier precio tiene sus riesgos. Pena que ninguno de mis brokers me deja operar en Dinamarca.

Que mejor forma de barrer para casa que repartiendo estopa al value investing y a Woodford. Se despacha a gusto Mr. Smith

Moreover, we have no desire to change our strategy. We are convinced that it can deliver superior returns over the long term. I would pose a different question which links the discussion of the Woodford affair with the earlier discussion of the ‘rotation’ from quality stocks into value stocks. If you expect such a ‘rotation’ to occur at some point and for value stocks to enjoy a period in the sun would you rather we tried to anticipate that and switched into a value investment approach of buying stocks based mainly or solely on the basis of their

valuation or would you rather we stuck to our existing approach of buying and holding high quality businesses? I would suggest the latter approach might be better, and it is what we are doing. There will be no style drift at Fundsmith.