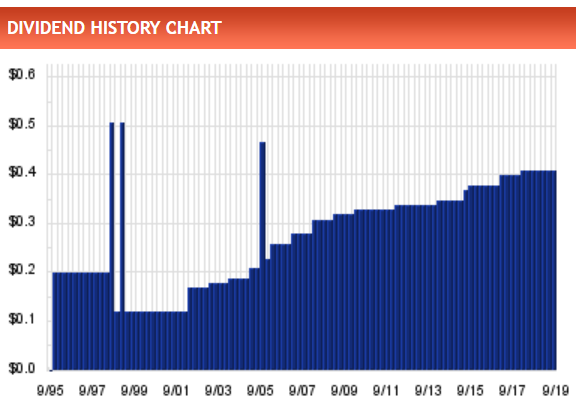

18 años incrementando dividendo

RPD actual=4,89%

DGR1=3,8%, DGR3=2,8%, DGR5=3,5% y DGR10=2,7%

PPL (PPL) is in discussions to merge with Avangrid (AGR), according to The Financial Times . Neither company has publicly confirmed the rumors, and it’s possible no deal is reached. However, a marriage of these two utilities could unlock some benefits for PPL shareholders.

Avangrid is a U.S. utility with a mix of regulated operations and renewables businesses focused primarily on wind. Regulated utilities generate about 70% of Avangrid’s adjusted net income, with renewables contributing the remaining 30%.

The firm’s regulated utilities deliver natural gas and electricity to customers in New York, Maine, Connecticut, and Massachusetts.

Importantly, Iberdrola (IBDRY), a major utility based in Spain with a market cap nearly three times larger than PPL’s, owns 81.5% of Avangrid.

Iberdrola generates close to 20% of its cash flow (EBITDA) from the U.K. and might be interested in combining PPL’s U.K. operations with its own, perhaps in the form of a new spin-off. Of course, such a plan would require regulators to give their blessing, which may be unlikely.

However, if successful, this would leave the PPL-Avangrid entity as an all-U.S. business with healthy exposure to renewables and predictable growth. In fact, Avangrid targets 8-10% adjusted EPS growth from 2018-22, and PPL’s earnings are expected to grow at a mid-single digit pace, according to management.

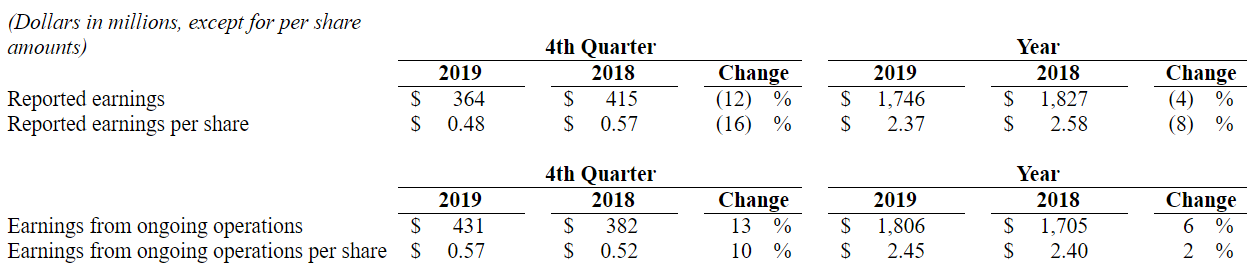

Third-Quarter 2019 Earnings (05/11/2019)

Cayendo un 16% hoy.

Esta empresa exáctamente a qué se dedica? Sería una especie de REE?

He estado mirando las cuentas y no acabo de entender qué pasa con sus flujos de caja. Todos los años tienen FCF negativos.Alguien me puede iluminar?

Acaba de presentar resultados. Por lo que veo el año pasado vendió a National Grid su negocio en Reino Unido y le compró la parte que National Grid tenía en EEUU. El resultado es una empresa más enfocada a EEUU y que ha rebajado su deuda neta/ebitda a 3,3 veces que es un rango muy manejable. Además tienen una nueva política de dividendos según la cual reparten un 60-65% de payout y como consecuencia acaban de recortar el dividendo a 0,2€ trimestrales. Es un recorte de más de la mitad de lo que venían repartiendo. Imagino que se vienen caídas gordas en bolsa. Pero ahora me parece una empresa mucho más interesante por fundamentales.

Sin embargo sigo sin acabar de entender todos sus negocios. No se si es una especie de REE pura o si tiene más cosas.

Ya se sabía desde el año pasado que iba a recortar. La roté a principios de año por ENB y WPC para tener mas o menos el mismo PADI.

Esto ponÍa en SSD en marzo: Applying a 60% to 65% payout ratio suggests an annual dividend per share between 84 cents and $1.04, or a reduction of 37% to 49% compared to the current payout of $1.66.

Ha sido incluso mayor el recorte.

Saludos.