AstraZeneca redacta un plan para escindir su negocio en China en medio de tensiones

El fabricante de medicamentos anglo-sueco considera incluir una unidad separada en Hong Kong como refugio potencial de la lucha global

Según los planes, AstraZeneca , que es la compañía cotizada más grande del Reino Unido por valor de mercado en £ 183 mil millones, dividiría sus operaciones en China en una entidad legal separada pero mantendría el control del negocio…

Una persona informada sobre los planes de AstraZeneca dijo que incluir una unidad separada en Hong Kong o Shanghái podría aislarla políticamente de cualquier movimiento de China para tomar medidas enérgicas contra las empresas extranjeras al convertirla en una empresa china más plausiblemente nacional. También ofrecería una fuente separada de capital.

Dijeron que la cotización separada también podría ayudar a los inversores en la compañía restante a asegurarse de que tenían menos exposición al riesgo relacionado con China…

Un detalle de Clicktrader

Analyzing AstraZeneca In Comparison To Competitors In Pharmaceuticals Industry

Amidst today’s fast-paced and highly competitive business environment, it is crucial for investors and industry enthusiasts to conduct comprehensive company evaluations. In this article, we will delve into an extensive industry comparison, evaluating AstraZeneca (NASDAQ:AZN) in comparison to its major competitors within the Pharmaceuticals industry. By analyzing critical financial metrics, market position, and growth potential, our objective is to provide valuable insights for investors and offer a deeper understanding of company’s performance in the industry.

AstraZeneca Background

A merger between Astra of Sweden and Zeneca Group of the United Kingdom formed AstraZeneca in 1999. The firm sells branded drugs across several major therapeutic classes, including gastrointestinal, diabetes, cardiovascular, respiratory, cancer, immunology and rare diseases. The majority of sales come from international markets with the United States representing close to one third of its revenue.

| Company | P/E | P/B | P/S | ROE | EBITDA (in billions) | Gross Profit (in billions) | Revenue Growth |

|---|---|---|---|---|---|---|---|

| AstraZeneca PLC | 33.60 | 5.29 | 4.40 | 3.68% | $3.33 | $9.4 | 4.64% |

| Eli Lilly and Co | 105.80 | 49.41 | 16.45 | -0.52% | $0.96 | $7.64 | 36.84% |

| Novo Nordisk A/S | 40.04 | 32.11 | 14.07 | 24.5% | $32.76 | $49.02 | 28.89% |

| Johnson & Johnson | 29.09 | 5.24 | 4.11 | 35.56% | $7.24 | $14.74 | 6.78% |

| Merck & Co Inc | 57.98 | 6.41 | 4.48 | 11.87% | $6.95 | $11.7 | 6.71% |

| Novartis AG | 25.20 | 5.24 | 3.79 | 3.91% | $4.88 | $8.97 | 12.14% |

| Pfizer Inc | 15.65 | 1.67 | 2.39 | -2.43% | $-1.1 | $3.96 | -41.55% |

| Bristol-Myers Squibb Co | 12.97 | 3.58 | 2.39 | 6.32% | $4.85 | $8.46 | -2.25% |

| Zoetis Inc | 38.59 | 17.13 | 10.50 | 12.28% | $0.9 | $1.51 | 7.44% |

| GSK PLC | 9.78 | 4.54 | 2 | 11.34% | $2.55 | $5.88 | 4.06% |

| Takeda Pharmaceutical Co Ltd | 33.55 | 0.90 | 1.55 | -0.69% | $202.28 | $699.51 | 4.07% |

| Viatris Inc | 6.51 | 0.57 | 0.77 | 1.59% | $1.22 | $1.69 | -3.34% |

| Dr Reddy’s Laboratories Ltd | 17.71 | 3.56 | 3.38 | 5.94% | $23.28 | $40.37 | 9.11% |

| Jazz Pharmaceuticals PLC | 146.12 | 2.19 | 2.23 | 4.19% | $0.33 | $0.87 | 3.35% |

| Corcept Therapeutics Inc | 33.99 | 6.07 | 6.84 | 7.06% | $0.03 | $0.12 | 21.5% |

| Amphastar Pharmaceuticals Inc | 22.28 | 4.59 | 5 | 8.31% | $0.09 | $0.11 | 50.3% |

| Average | 39.68 | 9.55 | 5.33 | 8.62% | $19.15 | $56.97 | 9.6% |

By thoroughly analyzing AstraZeneca, we can discern the following trends:

- With a Price to Earnings ratio of 33.6, which is 0.85x less than the industry average, the stock shows potential for growth at a reasonable price, making it an interesting consideration for market participants.

- With a Price to Book ratio of 5.29, significantly falling below the industry average by 0.55x, it suggests undervaluation and the possibility of untapped growth prospects.

- With a relatively low Price to Sales ratio of 4.4, which is 0.83x the industry average, the stock might be considered undervalued based on sales performance.

- With a Return on Equity (ROE) of 3.68% that is 4.94% below the industry average, it appears that the company exhibits potential inefficiency in utilizing equity to generate profits.

- The Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) of $3.33 Billion is 0.17x below the industry average, suggesting potential lower profitability or financial challenges.

- With lower gross profit of $9.4 Billion, which indicates 0.16x below the industry average, the company may experience lower revenue after accounting for production costs.

- With a revenue growth of 4.64%, which is much lower than the industry average of 9.6%, the company is experiencing a notable slowdown in sales expansion.

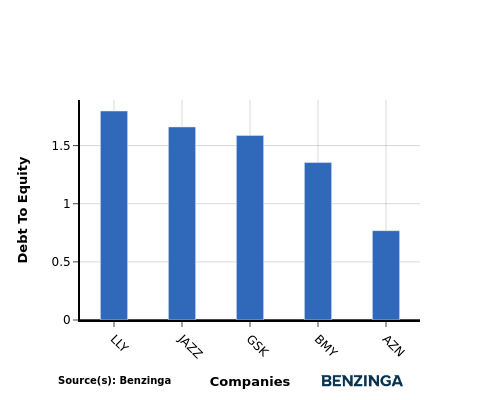

Debt To Equity Ratio

The debt-to-equity (D/E) ratio helps evaluate the capital structure and financial leverage of a company.

Considering the debt-to-equity ratio in industry comparisons allows for a concise evaluation of a company’s financial health and risk profile, aiding in informed decision-making.

When examining AstraZeneca in comparison to its top 4 peers with respect to the Debt-to-Equity ratio, the following information becomes apparent:

- AstraZeneca has a stronger financial position compared to its top 4 peers, as evidenced by its lower debt-to-equity ratio of 0.77.

- This suggests that the company has a more favorable balance between debt and equity, which can be perceived as a positive indicator by investors.

Key Takeaways

AstraZeneca has a low PE ratio, indicating that its stock price is relatively low compared to its earnings. The low PB ratio suggests that the stock is undervalued based on its book value. The low PS ratio indicates that the stock is trading at a low price relative to its sales.

On the other hand, AstraZeneca’s low ROE suggests that it is not generating high returns on its shareholders’ equity. The low EBITDA indicates that the company’s operating profitability is relatively low. The low gross profit suggests that AstraZeneca’s cost of goods sold is high compared to its revenue. Lastly, the low revenue growth indicates that the company’s sales are not growing at a significant rate.

Overall, AstraZeneca’s valuation ratios suggest that the stock may be undervalued based on its earnings, book value, and sales. However, the company’s profitability and revenue growth are relatively low compared to its peers in the pharmaceuticals industry.

This article was generated by Benzinga’s automated content engine and reviewed by an editor.

Copyright © Benzinga. All rights reserved. Write to editorial@benzinga.com with any questions about this content. Benzinga does not provide investment advice.

© 2023 Benzinga Newswires. Benzinga does not provide investment advice. All rights reserved.

Alto ejecutivo de AstraZeneca en China detenido por autoridades

Grupo farmacéutico confirma otros cuatro directivos actuales y anteriores investigados, además de Leon Wang

…

La investigación está relacionada con la supuesta importación y venta ilegal del medicamento contra el cáncer Imjudo y Wang se encuentra entre las personas detenidas en relación con la investigación, según una persona familiarizada con el asunto…

…

AstraZeneca mantuvo una conferencia telefónica con inversores el miércoles con su directora financiera, Aradhana Sarin, después de perder 15.000 millones de libras de su capitalización de mercado el martes en reacción a un informe de los medios chinos de que docenas de ejecutivos habían sido implicados en una investigación de fraude de seguros médicos.

La compañía dijo a los inversores que el informe de los medios confundió la investigación actual con sentencias anteriores a vendedores de la compañía por fraude de seguros en relación con la venta de su medicamento contra el cáncer de pulmón, Tagrisso…