Habrá que estar atento a ver si el precio consigue romper el canal bajista (que podría ser el toque de corneta que están esperando los que operan por técnico), o se le da por continuar el camino hacia abajo.

Muy buenas, ¿alguien sabe qué le pasa a este torpedo hoy? En vez de descontar el dividendo trimestral parece que esté descontando el de todo el año de golpe. Vaya cruz.

Reported diluted EPS of 249.0p down 5.4%, impacted by a number of adjusting items discussed below;

Adjusted diluted EPS of 323.8p up 9.1%, or 321.6p up 8.4% at constant rates;

Cigarette and THP volume share1 increased by 20bps, with value share2 up 30bps in key markets;

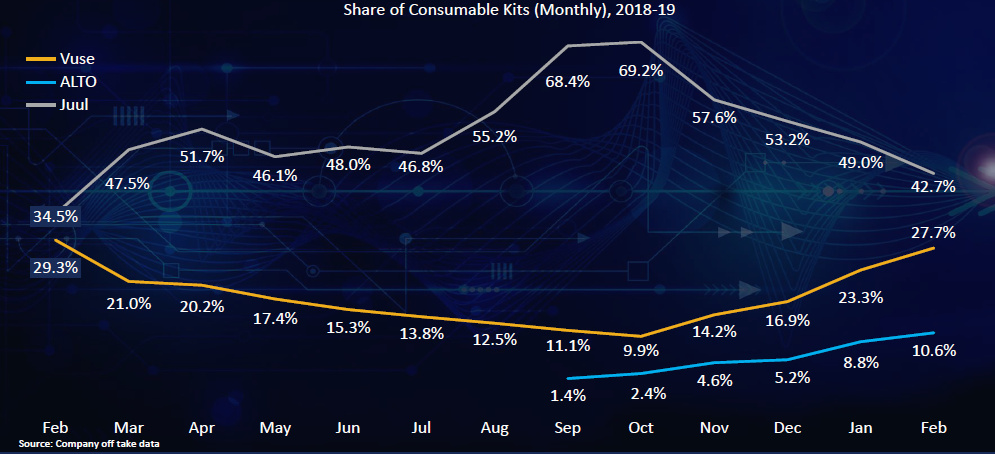

New Categories revenue grew 36.9% or 32.4% to £1,214m at constant rates with strong growth in all categories, despite the slowdown in US vapour. Excluding US vapour, New Categories revenue grew 39% at constant rates;

Reported revenue of £25,877m (up 5.7%);

Adjusted revenue of £25,827m (up 6.2%), or £25,683m on a constant currency basis (up 5.6%);

Reported profit from operations of £9,016m down 3.2% driven by adjusting items of £2,114m (2018: £1,034m) partly due to the charges incurred in respect of Canada (Quebec), Quantum (simplification programme), other smoking and health litigation including Engle in the US, Russia (excise dispute) and Indonesia (goodwill impairment), the majority of which are non-cash items;

Adjusted profit from operations of £11,130m (up 7.6%), an increase of 6.6% on a constant currency basis;

Reported operating margin declined 320 bps to 34.8%, largely due to the adjusting items;

Adjusted operating margin up 50 bps with significantly increased investment in New Categories;

At constant rates of exchange, the US delivered a strong year with adjusted revenue up 4.4%, value share up 30 bps and adjusted profit from operations up 6.4%;

Operating cash flow conversion was 97%, with adjusted cash generated from operations down 16.3% (on a constant currency basis). Normalising for the timing of the 2018 MSA payment, ACGFO increased 1.2%;

Free cash flow after dividends of £1,921m drove deleveraging of 0.5x to 3.5x (0.4x at constant rates); and

Dividend up 3.6% to 210.4p, in line with our commitment to a 65% pay-out ratio of adjusted diluted EPS.

A fecha de hoy estoy como tú y me quedo más tranquilo (ya se sabe, mal de muchos… )

Pensaba que era por haber acudido al drip. Siempre que lo hago tardan un poco más en aparecer las acciones nuevas, pero veo que esta vez hay más afectados y se lo están tomando con calma.

Saludos

La tesis es que si BATS crece al ritmo que se estima y vuelve al fair value histórico potencialmente se podría triplicar el valor de nuestra inversión en cinco años.

En el pasado ha pasado seis años sobrevalorada y luego otros seis años infravalorada. Actualmente lleva tres años bajista, lo que significa que, si las tendencias históricas se mantienen, debería volver al fair value en tres años.

Riesgo bajo de recorte de dividendo (en torno al 5% durante la crisis y menos del 1% en condiciones normales), principalmente por la deuda que todavía está un poco alta.

Si mantienen su política de payout ratio en torno al 65% daría para aumentar el dividendo 7% / año.

. Venga, apunta otra con otro 3% y entre las tres hacemos un 10

. Venga, apunta otra con otro 3% y entre las tres hacemos un 10

)

)