Based on the results of the first half of 2019, Covestro has confirmed its guidance for the current fiscal year. As expected, ongoing intense competitive pressure and uncertainties in major sales markets persisted into the second quarter.

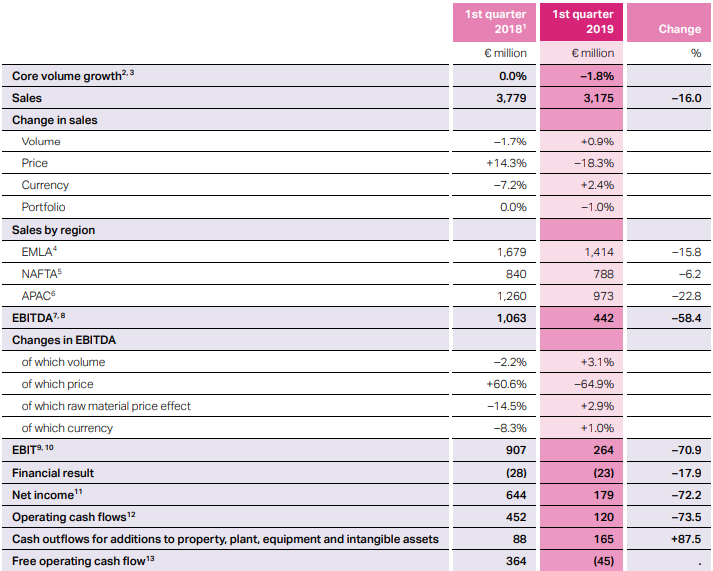

Whereas core volumes rose by 1.1%, Group sales fell to EUR 3.2 billion (–16.9%) due to lower selling prices. At EUR 459 million, EBITDA stabilized at the level of the first quarter of 2019 (EUR 442 million), but remained well under the outstanding result achieved in the prior-year quarter (–53.4%).

The decline in earnings resulted mainly from lower margins in the Polyurethanes and Polycarbonates segments. Net income declined to EUR 189 million, while free operating cash flow amounted to minus EUR 55 million on account of lower cash flows from operating activities and higher investments.

Yo la llevo en cartera desde finales de 2018.

Como ya dije en otros comentarios a menos de 40-42€ es muy buena compra para cualquiera a largo plazo( mas de 5 años ).

Empresa lider en su sector bién gestionada tanto en deuda como en payout por dividendo.

Las primeras compras las hice a 49-50€, a día de hoy tengo mi precio medio en 44€.

Para mi esta muy barata e injustamente infravalorada por Mister Market.

Empresa aburrida,sector aburrido,nombre feo y barata.

Pues hace un par de días me saltó en el screener hereje y me quedé un poco así, porque está en una zona que como se deje atrás los 30 con soltura igual se la llevan a probar la zona de mínimos, o por lo menos el intento.

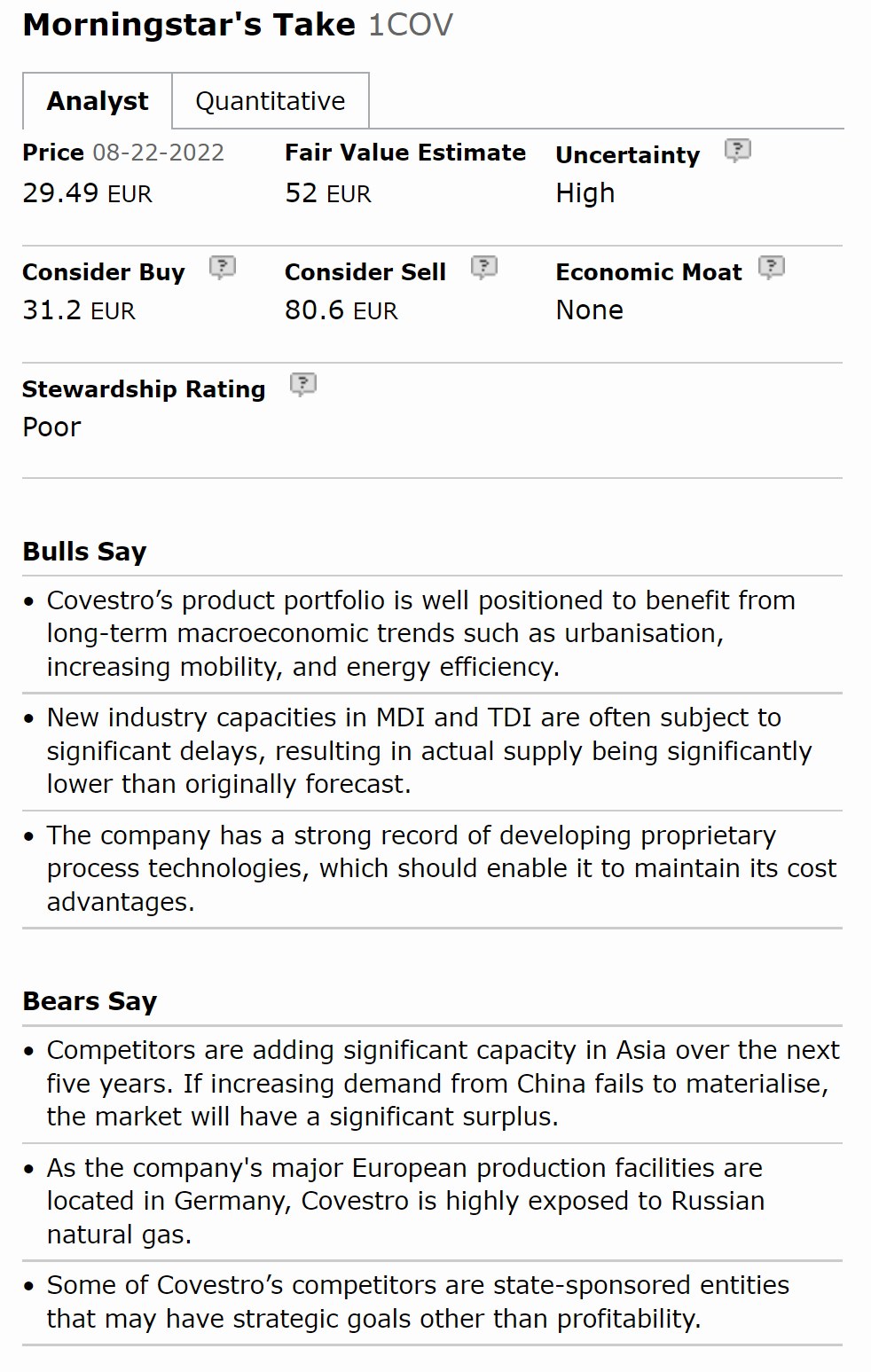

We don’t think Covestro has a moat, given that the majority of its business is in commodified products, with demand driven by highly cyclical end markets. The company is the cost leader in certain product markets. However, cost curves are relatively flat, which largely neutralises the benefits of leadership. Return on invested capital has been volatile historically and has often been below the company’s cost of capital.

Covestro has a Poor capital allocation rating. The company has allocated capital in a classic, procyclical manner historically, which we think has destroyed shareholder value. While new guidance and strategic targets assert the company has changed its ways, we will need to see some concrete evidence of the same before moving back to a standard rating.

The company’s balance sheet is sound. The company’s high cyclicality and operating leverage mean business risk is high. However, this is offset by low balance sheet risk given leverage is moderate and maturities are fairly balanced.

Vendo toda posición de Covestro. Con perdidas las cuales compenso al 100% con dividendos que cobro este año.

Pienso que no esta cara, esta a buenos precios de entrada. Igual si baja mas vuelvo a entrar con pequeñas compras en el rango de (30-35€).

La razón principal de la venta es la supresión del dividendo de este año y posiblemente del próximo.

Tenía una posición importante y me parecían demasiados activos parados sin cobrar dividendo.