Comparable store restaurant sales growth of 2.1% and traffic of -1.5% outperformed the casual dining industry.

As previously announced, the Company acquired Maple Street Biscuit Company in an all-cash transaction for $36 million.

The Company repurchased $14.2 million in shares in the first quarter.

GAAP earnings per diluted share were $1.79 compared to prior year first quarter earnings per diluted share of $1.96. This figure includes unfavorable impacts to earnings per diluted share for the quarter of ($0.11) related to transactional and integration expenses associated with the acquisition of Maple Street Biscuit Company and ($0.25) from the Company’s equity method investment in its unconsolidated subsidiary Punch Bowl Social.

Fiscal 2020 Outlook

GAAP earnings per diluted share between $8.50 and $8.65

Total revenue of $3.15 billion to $3.20 billion

Cracker Barrel comparable store restaurant sales growth of approximately 2.0%

Cracker Barrel comparable store retail sales growth of approximately 1.0%

Operating income margin of approximately 9.0% as a percent of total revenue

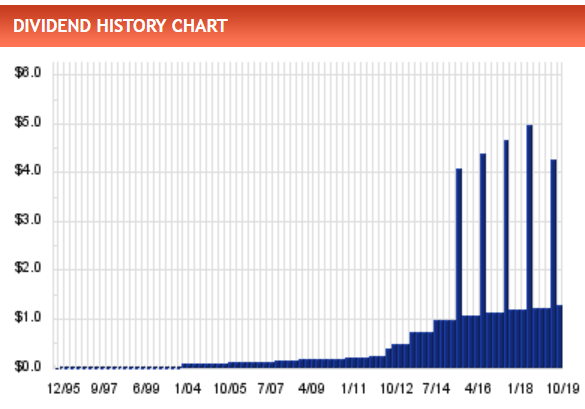

Gracias Cuke por darnos a conocer esta empresa. Tiene muy buena pinta como negocio (he leido opiniones en la red y hablan muy bien de sus restaurantes) e incluso los últimos años han pagado dividendos extraordinarios que han llevado el yield por encima del 5%, pero creo que esos pagos no los tenemos que tener en cuenta. Visto el tamaño de la empresa, 3-4B y lo desconocido que se me hace creo que esperaré a un yield mínimo del 4% (130 $).

¿Sabes algo de su balance, deuda…?

No, mis análisis no van más allá de mirar el histórico de dividendos y leer un poco sobre la empresa. El resto se lo confío a la diversificación y a ver que en los resultados trimestrales no hay nada raro.

Estuve en uno de estos restaurantes hace 10 años en un viaje por USA y me gustó. No deja de ser comida estilo Foster o algo así, con grandes ensaladas y un trato bueno por parte de los camareros hasta que recogen la propina y te giran la cara…

Varias veces me he acordado de ella para invertir, pero no se que tipo de recorrido tendrá en USA y que poder de expansión fuera, ya que hay muchos restaurantes de ese estilo ya y no paran de salir franquicias nuevas todos los años.

Estaría bien poder pillar un análisis detallado de las cuentas (por desgracia yo soy muy limitado para profundizar mucho en la contabilidad de una empresa) y la opinión de alguien que se mueva mucho por USA para que de una visión más realista de hacia donde pudiera ir.

Siempre nos quejamos de no haber podido pillar un McDonalds o un Starbucks en sus inicios, pero hay muchas cadenas de comida y gran parte de ellas no se caracterizan por ser una maravilla precisamente.

Salu2 y felices fiestas.

Total revenue of $846.1 million for the second quarter of fiscal 2020, representing an increase of 4.2% over the second quarter of the prior year.

Operating income in the second quarter was $79.1 million, or 9.4% of total revenue, an increase from the prior year quarter of $76.7 million, or 9.5% of total revenue.

GAAP earnings per diluted share were $2.55, compared to prior year second quarter earnings per diluted share of $2.52.

The Company repurchased $5.8 million in shares during the second quarter.

Fiscal 2020 Outlook

GAAP earnings per diluted share between $8.55 and $8.65.

Comparable store restaurant sales growth of 2.0% to 2.5%

For the third quarter of fiscal 2020, when compared to the comparable period in 2019, comparable restaurant sales declined 41.7% and comparable store retail sales declined 45.5%.

Total revenue of $432.5 million for the third quarter of fiscal 2020, representing a decrease of 41.5% over the third quarter of the prior year.

Cracker Barrel comparable store restaurant sales decreased 41.7% in the third quarter over the prior year quarter, as a 43.6% decrease in comparable store restaurant traffic was marginally offset by a 1.9% increase in average check.

Comparable store retail sales decreased 45.5% from the prior year quarter.

GAAP operating income (loss) in the third quarter was ($79.0) million, or (18.3%) of total revenue, a decrease from the prior year quarter GAAP operating income of $65.1 million, or 8.8% of total revenue.

Se esta poniendo interesante, esta a precios de covid con dividendo del 6,78%, en SSD le dan una puntuación de 70 (safe).

Antes del covid, llevaba 30 años consecutivos subiendo el dividendo, lo cancelo en dichos años por razones obvias y ya ha vuelto a los niveles pre-covid.