Henkel tiene marcas muy buenas, que nada tienen que envidiar a P&G. En cuidado del hogar por ejemplo Wipp Express, Micolor, neutrex… en belleza magno, latoja… y en peluquería a nivel profesional, tienen schwarzkopf, que es una marca top. Además del negocio de adhesivos, que a nivel profesional también es muy bueno.

Si puedes tener tres o cuatro empresas punteras, ¿por que conformarte con una?

Ese es el mejor argumento. Quizás en una cartera con pocos valores no sea así, pero en una cartera amplia de 50 o 60 valores que razón hay para conformarse sólo con una si puedes tener las dos o tres empresas más importantes de un sector, si gustan todas claro.

Mixed performance in increasingly difficult market environment

Adhesive Technologies delivers robust performance

Beauty Care below expectations

Laundry & Home Care achieves good business development

Sales of 5,121 million euros, almost at prior-year level, organic: -0.4%

EBIT margin* at 16.5% (-1.5 pp), earnings per preferred share (EPS)* at 1.43 euros (-9.5%)

First successes from announced growth initiatives

Investments in growth and digitalization

Strong balance sheet with good cash management

Updated outlook for fiscal year 2019

Henkel does not anticipate industrial demand to increase in the second half of the year – in contrast to previous expectations. In addition, it is expected that the Beauty Care business unit will develop below our initial expectations in the course of the year. Against this background, Henkel has updated the guidance for the fiscal year .

Previously, Henkel had expected organic sales growth of between 2 and 4 percent for the Group and all three business units. Now, Henkel anticipates for the Group an organic sales growth of 0 to 2 percent. For Adhesive Technologies , Henkel expects an organic sales growth of -1 to 1 percent. For Beauty Care , Henkel anticipates an organic sales development of -2 to 0 percent. For Laundry&Home Care , Henkel continues to expect organic growth in the range of 2 to 4 percent.

Henkel continues to expect adjusted return on sales on Group level in the range of 16 to 17 percent.

For adjusted earnings per preferred share (EPS), Henkel now anticipates a development in the mid- to high single-digit percentage range below prior year at constant exchange rates (previously: mid-single-digit percentage range below prior year at constant exchange rates).

Por lo que yo se está retenido ya la espera de que se celebre la junta de accionistas, pero vaya, yo creo que este año no habrá.

Yo tengo activado los emails de comunicaciones y me va llegando información.

As a result of the cancellation of the Annual General Meeting, the resolution on the appropriation of profit for fiscal 2019 and the respective pay out of the dividend are postponed as well.

The management board of Henkel AG & Co. KGaA in accordance with the relevant governance bodies decided to conduct the company’s Annual General Meeting on 17 June 2020. The meeting’s agenda will be consistent with the agenda of the Annual General Meeting originally planned for 20 April

Henkel ha confirmado el pago del dividendo para el 22 de junio. Mantiene el importe del año pasado 1,83€ para las ordinarias y 1,85€ para las preferentes.

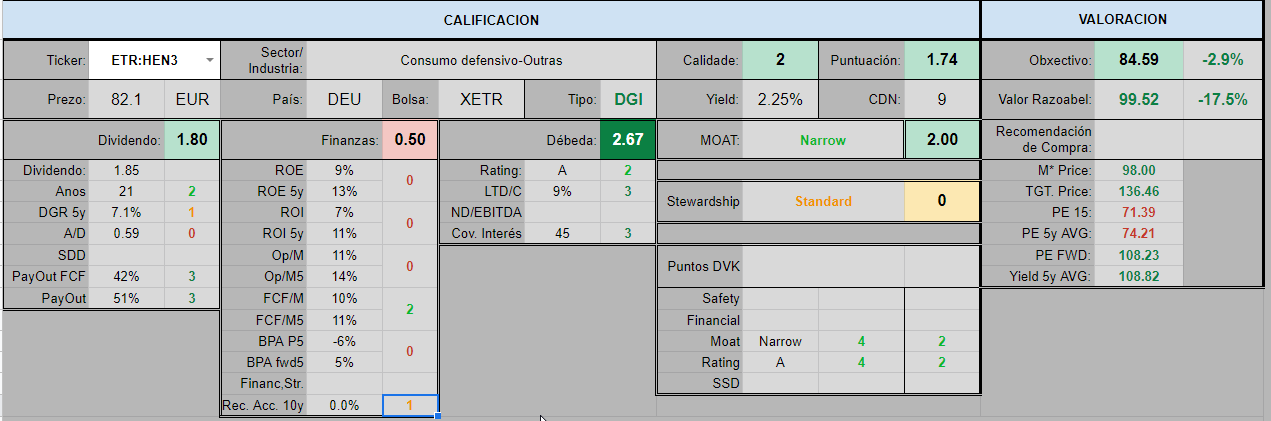

Revisando algunas empresas europeas, veo que Henkel, en un primer filtro, me devuelve un precio por debajo del precio de compra. El estado financiero parece un poco pobre, aunque las previsiones de las webs y M* les da un valor con bastante margen para el futuro.

Puede que los números actuales estén bastante dañados por el tema pandemia, y que se espere una mejora importante a futuro.

Alguno la lleva o la tiene controlada?