¿Cuando MMM cotizaba a 250$ el mercado se equivocaba o no?

Aunque estos tiempos han quedado atras

Ahora toca TSLA, ARKK y BTC

¿Cuando MMM cotizaba a 250$ el mercado se equivocaba o no?

Aunque estos tiempos han quedado atras

Ahora toca TSLA, ARKK y BTC

BATS y MO. No creo que nadie se sorprenda.

“Tobacco is continuing to consume an ever-greater portion of my portfolio. If the valuations of British American, Altria, Imperial Brands, and/or Japan Tobacco stay at these levels, I could very well reach a point this year where almost half of my wealth is in the tobacco sector.”

My lost brother

Yo no llego al 50% pero este año mis dos grandes compras han sido BATS y MO. Estoy esperando a poder ampliar en PM pero no la quiero comprar a más de 80.

Imperial Brands también la quiero ampliar a estos precios pero no tengo para más hasta que lleguen más dividendos.

I remain enthralled with the super low P/E ratios and super-high dividends that characterize the tobacco sector specifically. I add to British American, Japan Tobacco, Imperial Brands, and Altria (in that order). If these prices remain in effect long enough, they will be self-funding.

I am dead serious when I say that it is my intention to load up big tobacco for as long as these prices remain and then use those dividends to build out an entire portfolio of stocks over a multi-decade period.

Nuevo artículo (“gratuito”)

https://theconservativeincomeinvestor.com/learning-from-the-nikkei-indexs-all-time-high/

With low interest rates and a hope for a better economy, there are many American stocks and investments trading at ridiculous prices.Look for and purchase assets trading at valuations that you could justify to an early 1990s or early 2010s audience. That is where the future outperformance resides.

Otro gratis… the old Tim is back!!!

https://theconservativeincomeinvestor.com/those-profitless-high-flying-stocks/

I’m not saying there is no role for someone to own nosebleed P/E ratio stocks. I own three, and two of them looked excessively valued when I made the purchase (the third was the Visa shares purchased in 2015 I have mentioned from time to time, which have grown into a lofty P/E ratio).

But these types of stocks, on the whole, exhibit characteristics that lead to long-term underperformance. Generic businesses at fair prices will outperform enticing businesses trading at generational highs.

Por cierto, creo que las otros dos compañías a las que hace referencia en el comentario de arriba son Alphabet (GOOG) y Fair Isaac (FICO).

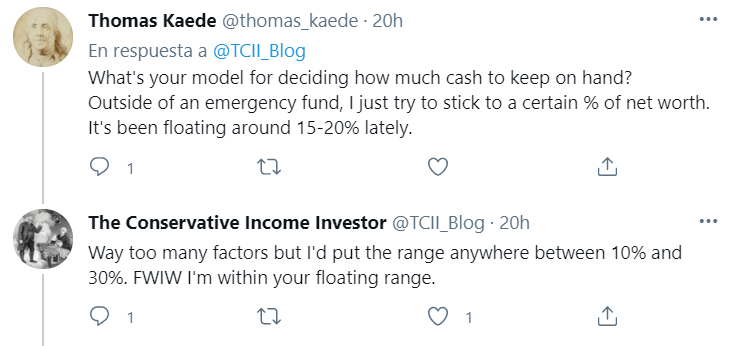

Madre mía! un 30% en liquidez!!

Es el eterno debate, pero yo cuando paso del 5% no puedo más, jajaja, ahora estoy en un 7% y estoy pensando dónde disparar. Claro, luego pasa que cuando vienen las rebajas no hay guita, ainsss.

Estoy de acuerdo, pero es lo de siempre. Cuanta subida o dividendos llevará perdidos por no haberlo invertido?

(él o cualquiera jajaja que no es nada personal  )

)

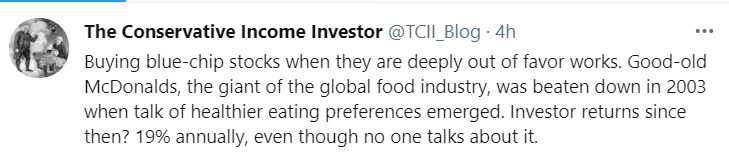

En general estoy de acuerdo con esa afirmación, pero lanzarse a comprar blue chips cuando caen por el mero hecho de que son blue chips sin analizar nada nos puede llevar a comprar Kodaks o Nokias…

O telefónicas

Y el otro punto es que hay que saber entrar en las bajadas. Cuando entras, cuando ha caido un 10%? Un 20%? Un 40%?

En las grandes caidas es cuando tiembla el pulso, porque nadie sabe cuánto va a caer… Y hay que tenerlos bien puestos para ejecutar la compra.

MCD, puede considerarse la empresa de más calidad de la comida rápida y tal como ha estructurado su modelo de negocio de franquicias, también tiene parte de Reit y gran poder de marca, por lo menos a mi me lo parece, no creo que se pueda comparar con Kodak y menos aún con TELF.

y con la Telefónica de 2006?

Comparar una blue chip USA con una blue chip española es cuando menos temerario. Y te lo dice uno que lleva TEF. Pero eso lo he aprendido.

En esencia, en España no hay blue chips.

Algunos nos lo creímos. Alierta decía que iba a repartir 1,10 € de dividendo, algo así como un 10% creo que suponía. Y nos lo creíamos…

Eso no lo he visto yo en ninguna blue chip USA.

British American Tobacco is “stupid cheap”.