@elninioarriba También deberías de comentar que en el articulo que citas el autor recomienda comprar o vender puts para comprar a un precio más bajo o embolsarse dinero.

Es decir, que cree que la cotización va a caer pero que aún así es una empresa para tener en cartera.

Está escrito abatidor, lo había comentado, aunque sin darle mucha importancia jejejejeje. Está claro que empresas como esta te pueden cambiar de la noche a la mañana, empiezan a vender de la ostia y cambia el panorama completamente.

Revenue was up 1 percent to $1.2 billion (up 3 percent currency neutral).

Wholesale revenue decreased 1 percent to $707 million and direct-to-consumer revenue was up 2 percent to $423 million, representing 35 percent of total revenue.

North America revenue decreased 3 percent to $816 million and the international business increased 12 percent to $339 million (up 17 percent currency neutral), representing 28 percent of total revenue. Within the international business, revenue was up 6 percent in EMEA (up 11 percent currency neutral), up 23 percent in Asia-Pacific (up 29 percent currency neutral) and down 3 percent in Latin America (up 2 percent currency neutral).

Apparel revenue decreased 1 percent to $740 million; footwear revenue increased 5 percent to $284 million; and accessories revenue was unchanged at $106 million.

Gross margin increased 170 basis points to 46.5 percent compared to the prior year driven by supply chain initiatives, regional mix and restructuring charges in the prior period offset by foreign currency impacts.

Selling, general & administrative expenses increased 2 percent to $566 million, or 47.5 percent of revenue.

Operating loss was $11 million.

Net loss was $17 million or $0.04 loss per share, inclusive of a negative $0.01 impact from the company’s minority interest in its Japanese licensee.

Inventory decreased 26 percent to $966 million.

Total debt was down 24 percent to $591 million.

Cash and cash equivalents increased 131 percent to $456 million.

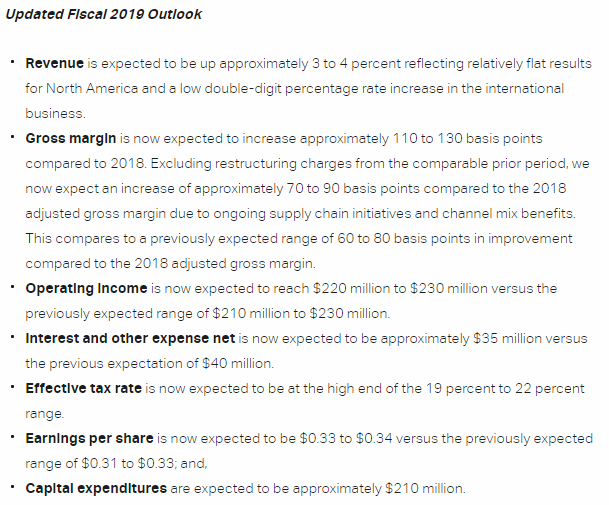

Fiscal 2019 Outlook

Revenue is expected to be up approximately 3 to 4 percent reflecting a slight decline in North America and a low to mid-teen percentage rate increase in the international business.

Gross margin is expected to increase approximately 110 to 130 basis points compared to 2018. Excluding restructuring charges from the comparable prior period, we expect an increase of approximately 70 to 90 basis points compared to 2018 adjusted gross margin due to ongoing supply chain initiatives and channel mix benefits.

Operating income is now expected to reach approximately $230 million to $235 million versus the previously expected range of $220 million to $230 million.

Interest and other expense, net is now expected to be approximately $30 million versus the previous expectation of approximately $35 million.

Effective tax rate is now expected to be approximately 22 percent versus the previous expectation at the high end of a 19 percent to 22 percent range.

Earnings per share is expected to be $0.33 to $0.34 inclusive of a negative impact from the company’s minority interest in its Japanese licensee.

Capital expenditures are expected to be approximately $210 million.

Revenue was down 1 percent to $1.4 billion (flat on a currency neutral basis).

Gross margin increased 220 basis points to 48.3 percent compared to the prior year driven by channel mix, supply chain initiatives and restructuring charges in the prior period.

Total debt was down 26 percent to $592 million.

Updated Fiscal 2019 Outlook

Revenue is now expected to be up about 2 percent versus the previously expected range of 3 to 4 percent.

Gross margin is now expected to increase approximately 130 to 150 basis points versus the previously expected range of 110 to 130 basis points compared to 2018. * Operating income is now expected to reach the high end of the previously given range of approximately of $230 million to $235 million.

Earnings per share is now expected to reach the high end of the previously given range of approximately of $0.33 to $0.34.

Capital expenditures are now expected to be approximately $180 million versus the previously expected $210 million.

Revenue was up 4 percent to $1.4 billion (up 4 percent currency neutral).

Gross margin increased 230 basis points to 47.3 percent compared to the prior year driven primarily by pricing including lower discounts to our wholesale partners, channel mix and supply chain initiatives.

Selling, general & administrative expenses increased 3 percent to $607 million, or 42.1 percent of revenue.

Operating income was $74 million.

Net loss was $15 million or $0.03 diluted loss per share

Cash and cash equivalents increased 41 percent to $788 million.

Inventory decreased 12 percent to $892 million.

Total long-term debt decreased 19 percent to $593 million.

Full Year 2019 Review

Revenue was up 1 percent to $5.3 billion (up 3 percent currency neutral).

Gross margin was 46.9 percent, a 180-basis point improvement from 45.1 percent in the prior year driven predominantly by supply chain initiatives, channel mix and prior period restructuring charges.

Selling, general & administrative expenses increased 2 percent to $2.2 billion, or 42.4 percent of revenue.

Operating income was $237 million.

Net income was $92 million or $0.20 diluted earnings per share

Initial 2020 Outlook

The company’s initial 2020 outlook currently includes an estimated negative impact of the coronavirus outbreak in China of approximately $50 million to $60 million in sales related to the first quarter of 2020. This outlook does not contemplate additional financial or operational impacts past the first quarter of 2020. Given the significant level of uncertainty with this dynamic and evolving situation, full year results could be further materially impacted. The following outlook also does not include any possible benefits or costs from a potential restructuring initiative. Key points related to Under Armour’s full year 2020 outlook include:

Revenue is expected to be down at a low single-digit percent compared to 2019 results.

Gross margin** is expected to be up approximately 30 to 50 basis points versus the prior year due to ongoing supply chain initiatives and regional mix benefits.

Operating income is expected to reach $105 million to $125 million.

Interest and other expense net is planned at approximately $30 million.

Diluted earnings per share is expected to be in the range of $0.10 to $0.13.

Capital expenditures are planned at approximately $160 million compared with $144 million in 2019.