Solo comentar que he cobrado la segunda parte del dividendo. Así que Caixabank abona el último en 2 pagos distintos. Para toda la explicación de los distintos dividendos, se puede ver aquí:

Un saludo a todos.

Solo comentar que he cobrado la segunda parte del dividendo. Así que Caixabank abona el último en 2 pagos distintos. Para toda la explicación de los distintos dividendos, se puede ver aquí:

Un saludo a todos.

Yo también tengo Caixabanc como broker y me ha pasado lo mismo, el pago del segundo dividendo lo han dividido en dos partes. Creía que era un fallo del broker pero por lo que comentas es algo habitual de esta empresa.

Gracias por la aclaración

¿Y cómo se explica la caída de un 3% hoy?

Me respondo a mismo. ¿Mañana toca subidón, subidón?

Shares in Unibail, whose earnings statement came after trading had closed, were hurt on Wednesday by a downbeat earnings report from British peer Intu Properties. Intu shares sank more than 21% after reporting a fall in first-half net rental income. Unibail shares closed 3.4% lower on Wednesday. ($1 = 0.8991 euros)

La sesión de hoy ha sido previa a los resultados, los han sacado después del cierre del mercado. Mañana ya se verá que…

UNIBAIL-RODAMCO-WESTFIELD, THE PREMIER GLOBAL DEVELOPER AND OPERATOR OF FLAGSHIP

DESTINATIONS, REPORTS SOLID RESULTS FOR H1-2019

“Unibail-Rodamco-Westfield (URW) delivered solid results, despite the challenging retail environment.

With a unique transatlantic platform, connecting the best brands with over 1.2 billion customer visits each year in the wealthiest catchment areas, the URW portfolio is at the forefront of the changes in a rapidly evolving retail environment. We are making significant progress in executing on our strategic objectives of Concentration, Differentiation, and Innovation, with very strong tenant sales growth in Europe and the US, the disposal of €3.2 Bn of assets above book value over the past 12 months, and multiple openings of restaurants, leisure concepts and Digital Native Vertical Brands across our portfolio.

Our transatlantic reach made possible by the creation of URW is showing the first exciting results: the Group signed a first-of-its-kind agreement with The VOID, a leading immersive virtual reality experience operator, to roll out their concept in over 25 of URW’s Flagship destinations in both the US and Europe.

More cross-border deals are expected to follow.

Our €10 Bn pipeline is well positioned for a mixed-use future, now with 50% of the GLA in retail and the rest in dining & leisure, offices, residential, and hotels. With our unique skills this will continue to contribute to value creation.

Confident in URW’s performance, the outlook for the remainder of the year, and favourable financing conditions, we are increasing our 2019 AREPS guidance by +€0.30 to a range of between €12.10 and €12.30"

Christophe Cuvillier, Group Chief Executive Officer

No me gusta cuando las empresas empiezan a inventarse nombres contables nuevos; nunca había oído esa expresión. No tenemos EPS y AFFO que ahora salen con AREPS. Eso era muy de telefónica.

¿Pero te han gustado o sigues con la mosca tras la oreja?

Yo tuve que buscarlo, porque era la primera vez que veía esa “variable”. Y sinceramente, pienso un poco como tú … llegará el día que con tal de dar un dato bueno van a terminar midiendo la cantidad de papel higiénico que se gasta en los servicios de los centros comerciales … mientras en Europa no se trabaje con un criterio unificado DE VERDAD en materia económica y en cosas como retratarse a la hora de dar cuentas de como va el negocio de una empresa se siga un criterio unificado al estilo de lo que tienen en USA seguiremos siendo una banda.

Un saludo.

Te suena eso de cuando estás comiendo y muerdes demasiado, pegas un mordisco demasiado grande, y encima se junta que la carne estaba dura y termina yéndose un trocito por donde no debe … comienzas a toser y toser intentando reconducir la situación, y si no se te tuerce la cosa mucho entre tos y tos consigues coger un poco de aire y eso te ayuda a seguir intentando tragar … pues eso, que URW parece que ha conseguido coger un poco de aire y continua intentando tragar. A ver si le da para un vaso de agua y termina pasando el mal rato.

Así que no es que siga con la mosca detrás de la oreja, es que vive conmigo … pueden sacar todos los AREPS que quieran, que como no ganen pasta el dividendo se lo terminarán trillando, porque margen por el payout va ser que no tienen mucho. Si lo mantienen se podrán dar con un canto en los dientes.

Un saludo.

Ainsssss hace unos años a estas horas mirando gráficos … y ahora leyendo una conference call a deshoras … para lo que queda uno  . En fin, a lo que venía … buceando en la conference call posterior a la presentación de resultados, he encontrado este extracto que pego en el que hablan sobre el tema del dividendo en respuesta a una cuestión sobre la conveniencia de mantenerlo o no. Básicamente en la respuesta dicen que están plenamente comprometidos con el mantenimiento del dividendo, que está cubierto sin problemas y que no entienden los rendimientos que se están llegando a dar merced al palo que lleva el precio de la acción encima. Al final todo el problema es el precio de la acción, cuyo desplome ha disparado el rendimiento … se ha quedado calvo el tipo… En fin, ahora solo queda ir mirando de vez en cuando la nariz del amigo Christophe para ver si le va creciendo

. En fin, a lo que venía … buceando en la conference call posterior a la presentación de resultados, he encontrado este extracto que pego en el que hablan sobre el tema del dividendo en respuesta a una cuestión sobre la conveniencia de mantenerlo o no. Básicamente en la respuesta dicen que están plenamente comprometidos con el mantenimiento del dividendo, que está cubierto sin problemas y que no entienden los rendimientos que se están llegando a dar merced al palo que lleva el precio de la acción encima. Al final todo el problema es el precio de la acción, cuyo desplome ha disparado el rendimiento … se ha quedado calvo el tipo… En fin, ahora solo queda ir mirando de vez en cuando la nariz del amigo Christophe para ver si le va creciendo

.

.

Robert Woerdeman, Kempen & Co. N.V., Research Division - Research Analyst [47]

Apologies for that. I’m wondering what is the obsession to maintain the dividend at EUR 10.80. I reckon that the value of the business is not on the level of the DBS, but more on the total return that you generate.

And I think it would take away a lot of noise around your stock. And it would actually help you to step up the disposal base and on the long-term, increase the quality of the overall portfolio.

Christophe Cuvillier, Unibail-Rodamco-Westfield - Group CEO & Chairman of Management Board [48]

Not sure I agree. I mean I think it’s very important for investors to – first of all, it’s not the stock price that dictates the dividend. I’m awfully sorry. And some people might not have understood yet Jaap’s humor, but when he says we agree that the dividend yield is crazy, it’s because of the denominator obviously. Actually tonight, I think the dividend yield is 8.9%, which makes actually no sense because it’s the cash flows that generate the dividend. And the cash flows, as you can see, are fine.

Jaap went through an extensive demonstration at the investor days in London, which showed that even if all disposals, the EUR 4 billion disposals that we needed to make, in addition to the EUR 2 billion disposals already made in 2018 in the second half of 2018, if all of these EUR 4 billion disposals had occurred on the 1st of January, the EUR 10.80 dividend would still be covered.

So I honestly, on a personal basis, I don’t know why people don’t want to understand that or maybe we haven’t given the right explanation. And we’re going to be very happy during the road shows tomorrow and Friday and next week in the U.S. to explain again, the cash flows drive the dividend. And as far as we know, there again, based on our 5-year BP and based on our disposal plan, the EUR 10.80 is covered. Why is it important to us? Because it’s important to investors and because it reflects the quality of our company and the quality of the work of the teams.

As far as disposals are concerned to streamline portfolio, I mean I think we’ve done a pretty good job with a more than EUR 10 billion disposals in the last 10 years to streamline the portfolio. If there again, you go back to the presentations we did or I did at Westfield London – at London actually. It was at Westfield London, and you see the average value of the Unibail-Rodamco assets or shopping center, I think it’s above EUR 700 million, it’s EUR 719 million off the top of my head. And you compare with our peers, you will see that we have done a job that some people have not done or didn’t have the same strategy, which for us is fine. But I don’t think that we should cut the dividend to hasten the disposal at any price. This is not a strategy, and I don’t think this is what investors expect from us. I think the investors expect delivering the results, operating results, leasing results. And I think that’s what we have done in the first half and that’s what we will continue to do in the second half.

Robert Woerdeman, Kempen & Co. N.V., Research Division - Research Analyst [49]

Okay. That’s a fair point, but it’s just interesting to see that the entire world is questioning the dividend, whereas, I can imagine that you’d rather focus on increasing the total return and focus on that rather than on a certain dividend yield.

Jacob Lunsingh Tonckens, Unibail-Rodamco-Westfield - Group CFO & Member of Management Board [50]

Robert, let’s have this conversation offline because it just gets a little bit unhelpful because the concept is not about decreasing the dividend yield by disposing. It’s basically during the cash flows Christophe has laid out, which we’ve demonstrated. And if people buy the stock, yield comes down. It’s very simple.

Un saludo.

Empiezo a pensar en ampliar, parecía que se había estabilizado, pero vuelve a caer…

Yo, por debajo de 118 haré entrada y completaré posición, o quizás hago media entrada, por si cae más. ¿Cómo la veis? Por más que la analizo veo que puede parar crecimiento, pero no que el dividendo esté en peligro.

Tenéis razón que se echa de menos que haya el mismo nivel de análisis de las europeas que de las americanas.

Resultados after market.

Me da que mañana se nos va para arriba.

… que buena falta hace,

p.s. y el viernes es el día que XOM llega al 6% de yield, ¿no?

Es curioso que el año en que todo está en máximos históricos mejores yields en general se han podido encontrar.

Presenta resultados este viernes XOM? Buf, las perspectivas no son halagüeñas pero creo que algo descontado está. Para que diera un 6% tendría que caer un 15%. Pues viendo lo exagerado que es el mercado a corto plazo, a saber.

Eterno dilema…¿Cargo ahora y me garantizo los 68$ o espero y, casualidades del destino, se marca un viscofan?

Parece que continúan cogiendo aire. En el PDF confirman el rango de lo que en Julio llamaron “AREPS” y que ahora, muy cabalmente, han vuelto a mencionar con todas las letras, el ajusted recurring earnings per share. Daban rango entre 12.10-12.30 en Julio pasado y se reafirman ahora. Entonces defendían la sostenibilidad del dividendo y su compromiso con el mismo, esperemos que la mejora en los resultados refuerce ese compromiso.

Supongo que aun les quedará morralla que ir eliminando. Si poco a poco van quitándose de encima aquello que no les es rentable como comentan hicieron en España en 2018 y han hecho en los países nórdicos en 2019 y se centran en potenciar aquello que sí les produce beneficio, al mismo tiempo que continúan integrándose las cifras de WFD deberían de ir mejorando los resultados poco a poco. Todo ello con los dedos cruzados para que de verdad no venga el lobo de la recesión que tantas veces se menciona y lo pare todo en seco, en cuyo caso mari… el último.

Un saludo.

Pues yo me voy a mojar … el dividendo ya veremos como sale la cosa al final. Esperemos que sean de palabra, que los números que hicieron fueran buenos y esté cubierto sin problema y como mínimo mantengan. En cuestión de precio creo que se tiene que ir arriba. En corto plazo (TF’s diarios) puede corregir como parece que está haciendo tras la presentación de resultados. Se puede dar un paseo si la llevan hasta la zona de los 135 de nuevo tranquilamente y no se rompería nada, incluso algo más abajo para filtrar (130 zonales). Fijando la referencia en el TF alto se podría apoyar incluso bastante mas abajo. Pero esto ya obligaría a replantear todo y ver los porcentajes de corrección. No obstante, en TF’s mas altos las divergencias son alcistas. Así que salvo sorpresa, para mí, yo creo que con el paso de las semanas tiene que tirar arriba. Cuando hablo TF’s mas altos me estoy refiriendo a compresiones semanales y mensual. Luego ya cada uno tiene su forma de ver las cosas, pero yo es lo que creo puede pasar. Después de todo no está sino corrigiendo un segundo impulso. Si se toma el mensual, hizo un primer impulso con el techo en los 117 y pico, corrigió al 61.8% del fibo y desde ahí arrancó con un segundo impulso. En corregir ese 61.8% del fibo consumió dos años aproximadamente. Con el segundo marco el techo en los 200 zonales, sobre 208 aproximadamente. Se ha hecho ya la vuelta entre el 50 y el 61.8% del fibo de este segundo, consumiendo entre dos y tres años (depende de si contamos la formación del doble (¿triple?) techo o no). Y no me da la sensación de que se vaya a ir a buscar el 61.8%. No lo creo por la estructura del precio, que se ha ido a apoyar en la zona de techo del primero, y por las divergencias que creo marcan algunos indicadores. Así que ¿por qué no poner la mira en el techo del segundo impulso de momento? Pero, recuerdo, estamos hablando en TF’s mensuales, con lo que ello conlleva. Los movimientos en TF’s medios y altos no son de hoy para mañana, detalle este que a veces cuesta entender si no está con estas cosas.

En fin, que me ha dado el aire y he profanado este santo lugar consagrado a los dividendos hablando de herejías como rayas, gráficos e indicadores. Prometo flagelarme sin descanso al menos durante cinco minutos como penitencia.

Un saludo.

Estáis demasiado pendientes del precio y la digestión de la compra va a llevar su tiempo. Largo plazo y tal. Pero hasta la fecha el plan va siguiendo su curso y la empresa esta entregando trimestre a trimestre los resultados prometidos. Simplemente hay que dejarles trabajar y que sigan entregando resultados. Ya lo hicieron en su momento con la fusión de Unibail y Rodamco. El precio quien sabe cual será el catalizador, que acabe entrando algún fondo importante, que pase el tiempo y sigan entregando resultados…

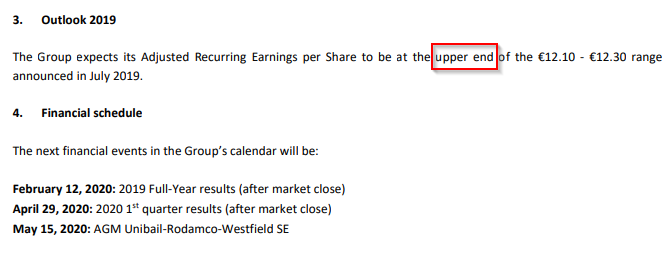

Por lo pronto, esperan rango alto del guidance que se habían puesto:

Y en M*:

cuando he visto TF por primera vez he pensado… será Telefónica?

No hace falta flagelarse, castígate con unas flexiones que al menos se supone que son buenas