No me importaria si no fuera porque tengo las primeras entradas a muy buenos precios, por debajo de 40.

Ademas, tampoco veo ninguna empresa clara de las top para entrar ahora a estos precios.

Prefiero esperar, quietooorrrrrrr

No me importaria si no fuera porque tengo las primeras entradas a muy buenos precios, por debajo de 40.

Ademas, tampoco veo ninguna empresa clara de las top para entrar ahora a estos precios.

Prefiero esperar, quietooorrrrrrr

Cooj…ns, he estado echando un vistazo en la EUR_DGI y la única en verde es Unilever

Esto será aquello de como no soy capaz de defender mi marca haciendo más atractivo mi producto a través de innovación y desarrollo para mejorar oferta y calidad disponibles, para crecer, o a lo mejor simplemente mantenerme, tan solo me queda la opción de mejorar mis resultados por la vía del recorte en gasto.

Han empezado con lo más fácil y rápido, gente fuera, rebajar masa salarial.

Dado que por el lago del capex de crecimiento ha quedado demostrado que se les rien en la cara, se dedicarán seguidamente disminuir el de mantenimiento.

Y por último la gente se comerá los helados sujetos por un palito hecho de cartón reciclado muy barato que sorprendentemente se deshace cuando aún tienes medio helado por comer, el plástico del envase de algunos geles, champús y jabones será tan fino que para sacar el producto de su interior habrá que procurar un suave masaje a dicho envase por riesgo a que este se rompa si se pretende extraer del modo habitual por presión manual, etc, etc, etc y ya sabemos a donde lleva esto.

Mi insiste, la dirección huele a cadáver…

Un saludo.

Pero este plan de recorte de gastos es nuevo? Unilever ya tenía uno al menos en el que planeaban ahorrar mas de 1 bns€ anuales. Bueno es que también estas empresas tan grandes siempre están igual. En los resultados luego lo califican como extraordinarios, y los vas viendo todos los años esos “extraordinarios”

A este ritmo, mi cartera va a parecerse más a un fondo índice.

En Europa tenemos un deficit de buenos directivos alarmante

En Europa tenemos un déficit en general bastante alarmante

Vaya desastre de empresa. Debería ir como un tiro. Es evidente que el problema es el equipo directivo.

Pues no estaría mal que el equipo directivo siguiera metiendo la pata unos 2 ó 4 años.

Para comprar en rebajas. Es la única manera de acceder a buenos precios a este tipo de empresas

2-4 años mas?

Que yo llevo comprando desde el 2016

Jobar, es para hacerselo mirar. La madre de dios, tengo yo esos resultados en las finanzas de mi casa y nos embarga el banco

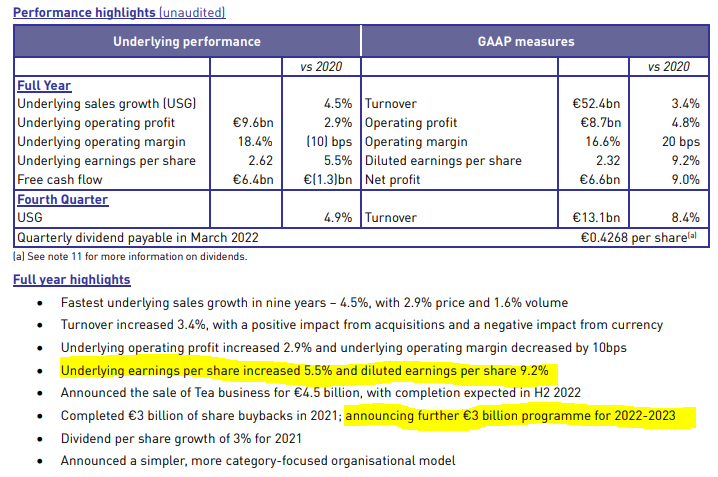

Unilever reported fourth-quarter and full-year results that were slightly better than we had expected on the top line, as it began raising prices to offset inflation. Management has warned, however, of further cost pressures to come, and we have increased our revenue estimate but lowered our margin estimates for 2022.

In aggregate, this has minimal valuation impact and we are retaining our EUR 50 fair value estimate for the Amsterdam-traded ordinary shares, and we think the recent sell-off presented a rare entry opportunity. However, we acknowledge the guidance that cost pressures will not ease until 2024 has increased the risk to our valuation.

We still believe a normalized EBIT margin of 20% is achievable in five years, but it now requires a sharp improvement in profitability once inflation abates, as well as ongoing price increases being somewhat sticky.

Fourth-quarter underlying sales growth of 4.9% year over year and full-year growth of 4.5% is the fastest growth Unilever has reported in almost a decade, but we believe 3.2% underlying sales growth on a two-year average basis is more reflective of our estimate of Unilever’s structural growth rate. We continue to estimate 3.4% steady state sales growth.

Sales would have been higher in 2021 were it not for continued weakness in Europe. The Asia/AMET/RUB and Americas segments grew by 5.8% and 5.5%, respectively, while lackluster pricing in Europe meant underlying sales grew by just 0.4%. The evidence of the fourth quarter, in which volume in Europe fell by 1.5% on price/mix of just 0.7% suggests that European consumers may have become conditioned to expect stable prices following a prolonged absence of inflation. By contrast, the emerging market consumer is accustomed to price increases, and Unilever’s exposure to emerging markets, which represented 58% of sales in 2021, and the ability to pass through cost inflation in these markets may help offset some of the challenges of the company’s categories.

Al loro con esta, hoy ex date, mañana es el record date.

Un saludo.

Entonces ¿El que haya comprado hoy cobra?

Saludos.

No, en el ex date no tienes ya derecho al cobro del dividendo que se descuenta en esa fecha. Siento si he generado esa confusión con el comentario. Mi comentario iba mas sobre lo que el descuento del ex date puede suponer en el precio, y más en un día como hoy.

Un saludo.