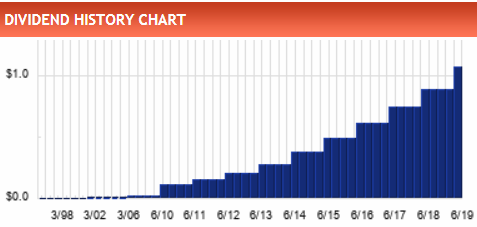

Abro hilo para esta empresa, aprovechando que hace unos días se comentó en el foro.Es la empresa de seguros de salud más grande de Estados Unidos. Respecto al historial de dividendos, aunque tiene una RPD baja, de un 1.5%, su crecimiento de los últimos años es muy elevado. Según la lista CCC lleva 9 años incrementando dividendos a este ritmo:

Esta es la evolución del dividendo según Dividend Channel:

Parece una empresa espectacular. Mirando en seeking alpha el yield medio de los últimos 4 años es 1,46% con lo que por ese lado no estaría cara ya que el forward yield es 1,75%.

A pesar del aumento de dividendo tan alto el payout lo han reducido un poco en los últimos años.

Yo no miro empresas con un yield tan bajo pero alguna empresa así puede tener cabida en mi cartera

Wide-moat-rated UnitedHealth Group reported third-quarter results that beat consensus on the top and bottom lines. Positive trends continued in all major business lines, and the firm increased its adjusted earnings outlook for 2019 based on those trends. While we appreciate UnitedHealth’s momentum, we do not expect to change our fair value estimate on the basis of these announcements.

During the quarter, revenue grew 7% year over year to $60.4 billion, operating profits grew 9% to $5.0 billion, and adjusted earnings per share grew 13% to $3.88. UnitedHealthcare, the leading U.S. health insurer, grew 5% year over year to $48.1 billion in revenue while operating profits grew 4% during the same period to $2.7 billion. This business continues to benefit from the expansion of Medicare Advantage plans, and the recent executive order bolstering that program may reinforce those positive trends.

The Optum businesses delivered 13% consolidated revenue growth to $28.8 billion and operating profit growth of 16% to $2.4 billion. By business line, OptumHealth, which recently closed on the acquisition of DaVita Medical Group, increased revenue 34% to $8.1 billion. OptumInsight, the company’s healthcare-focused information technology group, grew 16% year over year to $2.6 billion while its backlog grew 21% to $19.0 billion, which bodes well for future growth. OptumRx grew 6% to $18.5 billion, despite the ongoing transition of Cigna’s business after the latter’s acquisition of top-tier pharmacy benefit manager Express Scripts.

With these strong trends, the firm now expects to generate adjusted EPS of $14.90-$15.00 in 2019, up about 16% year over year and up from its $14.40-$14.70 original guidance. The company plans to give 2020 expectations at its Dec. 3 analyst day. However, management expects its core earnings outlook to be on the low end of its typical 13%-16% growth goal and may be further influenced negatively by the reinstatement of the health insurance tax.

Specifically, we no longer feel confident enough to endorse a wide moat rating, which implies excess returns for at least the next 20 years, for UnitedHealth despite its unrivaled scale advantages in the U.S. health insurance industry

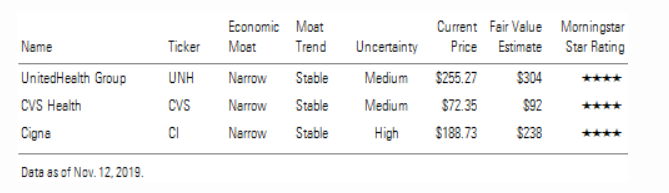

Admittedly, in a pure Medicare for All scenario where U.S. insurers have no place in the U.S. insurance market, these companies’ U.S. medical and pharmacy benefit management operations could be in jeopardy. These businesses represent about 60% of CVS’ operating profits, about two thirds of UnitedHealth’s operating profits, and about 85% of Cigna’s operating profits.

However, we believe this scenario represents a very low-probability (5% or less) risk within our 10-year forecast period, as it would require significant shifts in control of the current federal government bodies, including a filibuster-proof Democratic majority position in the Senate and a new president from the far-left wing of the Democratic Party.

Tengo la certeza de que hay una caza de brujas en marcha hacia ciertos sectores. De lo contrario no se explica que la dieta alimenticia mate mucha más gente al año que el tabaco y que no se le meta mano a MCD, QSR, GIS, SJM, K…

Ni una cosa ni la otra. Esto va de “Artificialmente demonizar” y luego “artificialmente olvidar lo demonizado”. A través de esas dinámicas se mueven los precios. Primero Nadie iba a comprar IPhones porque eran caros y tal, luego nadie va a comprar tabaco porque no seque del vaping, luego nadie va a comprar Victoria Secret porque su modelo es caduco etc…a veces son problemas puntuales que se SOBREDIMENSIONAN para crear tendencias…va por sectores…de hecho cuando empiecen a bajar las que han estado subiendo en los últimos años bastante (qué cálculo sobre la reelección de Trump) veréis a Altria volver a 80.

No es de UNH en particular, igual hay otro hilo más adequado.

Defensive Nature of Healthcare Firms Should Offer More Protection From Coronavirus Concerns

M* 19-Mar-2020

The concerns around a global recession due to coronavirus disruptions are weighing on global markets, but the defensive nature of healthcare should hold up on a relative basis, and we don’t expect any significant changes to our healthcare moat ratings. While we may make downward adjustments to our valuations in healthcare to account for near-term challenges, we expect more modest changes relative to recent stock price movements. Our base case calls for a strong economic rebound in 2021 following a recession in 2020, which should only have modest impacts to healthcare valuations, given the defensive nature of those companies. However, if the coronavirus pandemic exerts a sustained impact on the economy, with significantly higher numbers of patients unemployed and uninsured or underinsured, this could reduce healthcare demand to a greater extent. We expect government efforts to reduce the near-term hit can keep most of the harder-hit industries in business while effective treatments emerge.

On the near-term effects of coronavirus, we expect critically ill coronavirus patients needing essential medical services and therapies will crowd out more elective procedures, new products, and non-critical-care products. Fewer elective procedures will weigh on the device makers and service providers. Also, higher-than-expected medical costs focused on the COVID-specific cases could reduce profitability for health insurers. With branded drug firms already focused on specialty drugs, we expect less impact to this industry, but drugs administered in the hospital could still feel some crowding out by coronavirus patients. Also, clinical development timelines will probably face some delays due to coronavirus disruptions, which will likely slow some new product launches. Additionally, the coronavirus impact on the credit markets could weigh on more heavily indebted companies, such as some hospital firms and companies that have recently completed major acquisitions.