Continua la sangria… si cae hasta los 60$ me pensare entrar con algo. ?

1 me gusta

Espectaculares resultados de Walgreens Boots en el último trimestre…

Walgreens Boots (NASDAQ:WBA): Q4 EPS of $1.31 beats by $0.10.

Revenue of $30.15B (+5.3% Y/Y) beats by $220M.

1 me gusta

- GAAP diluted net earnings per share were $0.76, down 20.0 percent from the year-ago quarter due to Rite Aid related costs, mainly merger termination fees; Adjusted diluted net earnings per share were $1.31, an increase of 22.4 percent on both an actual and constant currency basis

- GAAP net earnings attributable to Walgreens Boots Alliance decrease 22.1 percent, to $802 million; Adjusted net earnings attributable toWalgreens Boots Alliance increase 18.8 percent to $1.4 billion, up 19.1 percent on a constant currency basis

- Sales increase 5.3 percent to $30.1 billion, an increase of 6.4 percent on a constant currency basis

- GAAP operating income decreases 2.3 percent to $1.1 billion; Adjusted operating income increases 21.2 percent to $1.9 billion, up 22.3 percent on a constant currency basis

1 me gusta

En USA también “el que no corre, vuela”.

Walgreens Boots Alliance recomienda a los accionistas rechazar la oferta de mini-oferta de TRC Capital Corporation.

DEERFIELD, Ill .-- ( BUSINESS WIRE)) - Walgreens Boots Alliance, Inc. (Nasdaq: WBA) anunció hoy que ha recibido un aviso de una mini oferta no solicitada por TRC Capital Corporation para comprar hasta 2 millones de acciones comunes de Walgreens Boots Alliance a un precio de $ 67.88 por compartir en efectivo El precio de oferta de TRC Capital es 4.38 por ciento inferior al precio de cierre de las acciones ordinarias de Walgreens Boots Alliance el 10 de noviembre de 2017, el último día de negociación anterior a la fecha de la oferta de compra y 4.73 por ciento inferior al precio de cierre de Walgreens Boots Alliance común stock el 17 de noviembre de 2017, el último día de negociación anterior a la fecha de este comunicado de prensa. La oferta es por aproximadamente 0.198 por ciento de las acciones ordinarias en circulación al 30 de septiembre de 2017.

Walgreens Boots Alliance no respalda la mini oferta no solicitada de TRC Capital y recomienda que los accionistas no ofrezcan sus acciones en respuesta a la oferta porque la oferta tiene un precio por debajo del precio actual de Walgreens Boots Alliance y está sujeta a numerosas condiciones . Walgreens Boots Alliance no está asociada de ninguna manera con TRC Capital, su mini oferta o la documentación de la oferta.

TRC Capital ha realizado muchas ofertas de mini ofertas similares para acciones de otras compañías. Las ofertas de compra mínima buscan adquirir menos del 5 por ciento de las acciones en circulación de una compañía, evitando así muchos requisitos de revelación y procedimientos de la Comisión de Bolsa y Valores de los Estados Unidos (SEC) que se aplican a ofertas por más del 5 por ciento de las acciones en circulación de una compañía. Como resultado, las ofertas de mini-oferta no brindan a los inversores el mismo nivel de protección que ofrecen las ofertas de oferta más grandes en virtud de las leyes de valores de los EE. UU.

La SEC advirtió a los inversionistas que algunos postores que hacen ofertas mini-tier a precios por debajo del mercado “esperan que tomen a los inversores por sorpresa si los inversores no comparan el precio de oferta con el precio actual del mercado”. Más sobre la guía de la SEC los inversionistas en ofertas de mini-oferta están disponibles en https://www.sec.gov/reportspubs/investor-publications/investorpubsminitendhtm.html

Y sigue:

https://www.businesswire.com/news/home/20171120005370/en/

Saludos.

1 me gusta

Hola compañeros,

Como la veis para hacer una primera entrada? Siempre pensando en el largo plazo

Un saludo

Hola compañeros,

Como la veis para hacer una primera entrada? Siempre pensando en el largo plazo

Un saludo

https://seekingalpha.com/article/4243312-walgreens-prescription-growth-dividends

Un saludo.

Walgreens Boots Alliance, Inc. (WBA) operates as a pharmacy-led health and wellbeing company. It operates through three segments: Retail Pharmacy USA, Retail Pharmacy International, and Pharmaceutical Wholesale.

Walgreens is a dividend champion, with 43 consecutive years of annual dividend increases under its belt.

Over the past decade, Walgreens managed to double earnings per share from $2.03 in 2007 to $5.05 in 2018. The company is expected to earn $6.52/share in 2019.

Earnings Per Share for Walgreens Boots Alliance

Growth in earnings per share should come from acquisitions, such as the recent purchase of close to 2,000 Rite Aid stores. This will increase Walgreen’s scale, which could result in a competitive position that results in lower costs for drugs from manufacturers for example. In addition, those acquisitions could result in synergies that add to Walgreen’s bottom line. As a growing portion of population is aging, the amount of prescriptions is only going to increase, offset by the increased penetration of cheaper generic drugs. One of the reasons why I like Walgreen’s and CVS today is the fact that everyone seems to be worried about the potential impact of Amazon disrupting their business model. Based on my research, it would be very difficult for Amazon to replicate the scale of operations in purchasing and efficiently serving clients, the relationships with Pharmacy Benefits Managers, the specialty drug business, and the regulatory hurdles to operate the business in this sector. This is why I believe that the recent weakness is a buying opportunity, since it provides an attractive entry point for long-term investors. This weakness in the share price could also bode well for share buybacks.

Over the past decade, the number of shares outstanding has increased slightly. The company repurchased shares between 2007 and 2012, bringing the total number of shares outstanding from a little over 1 billion shares to 880 million. The subsequent purchase of a 45% stake Alliance Boots in 2012 and the acquisition in 2015 led to an increase in the number of shares to 1.09 billion in 2015. After a few years of buybacks, the number of shares outstanding is down to 995 million.

Shares Outstanding in Mil for Walgreens Boots Alliance

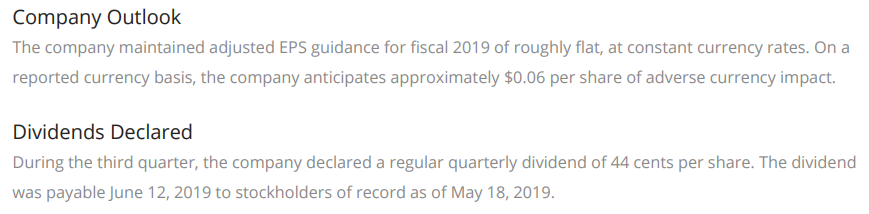

Over the past decade, the company has managed to increase the amount of its dividends by a factor of five. Walgreen’s paid an annual dividend of 33 cents/share in 2007, which has increased to $1.64/share by 2018. Just a few months ago, the company raised its quarterly dividend by 10% to 44 cents/share.

Dividends Per Share for Walgreens Boots Alliance

Walgreen’s was able to increase its dividends at a rate that was higher than earnings growth due to the expansion of its dividend payout ratio. Between 2007 and 2018, the dividend payout ratio increased from 16% to 40%. Going forward, I expect a much smaller room for expansion in the dividend payout ratio than before. However, I would still expect dividend growth to slightly exceed earnings growth over the next decade. But do not expect dividends per share to grow by a factor of five – I would be satisfied with a doubling of the amount of earnings and dividends over the next decade.

Valuation for Walgreens Boots Alliance

I find Walgreen’s to be cheap at 10.40 times forward earnings. The stock yields 2.60% and has a forward payout ratio of 27%. The dividend has a high safety score, and I believe that the stock price reflects the uncertainty that we all hear about in the news. I believe that the low valuation is unwarranted, and would be corrected at some point. If this comes out through a valuation expansion and an increase in earnings power, this could lead to great returns. For long-term accumulators of assets like me however, I am fine if I can continue buying regularly why the stock price is down. This means to me that I am able to purchase future dividend income at a discount.

Gracias a todos por vuestras aportaciones. Cuanto más indago en esta empresa, más me gusta

Y ahora viene la duda, ¿a precios actuales WBA o CVS?

Y ahora viene la duda, ¿a precios actuales WBA o CVS?

¿Un poco de cada ponderando más la que más te guste?

Saludos.

Por si puede ayudar:

Y ahora viene la duda, ¿a precios actuales WBA o CVS?¿Un poco de cada ponderando más la que más te guste?Saludos.

Depende lo que busques:

a) WBA es un retailer, parecido a WMT o TGT, solo que vende medicamentos. Menos complicación pero también menos barreras de entrada

b) CVS es otra cosa, un experimento que pocas veces se ha hecho. Farmacia + aseguradora + clinicas “one minute” con diagnosticos rapidos tipo gripe anginas etc. entre otras cosas. Ahora hablan de partnership con Apple para monetizar las app de salud de los apple watch por ejemplo.

CVS es algo mucho más ambicioso, y de las dos yo me quedo con ella ya que me parece una visión a largo plazo cojonuda, pero es algo personal. Muchas de mis inversiones se basan en “admiración” por el management. Me explico: cuando escucho y leo cosas del board de CVS tengo la sensación de que realmente ven mucho más lejos que yo, la impresión es que mientras yo veo a 100km ellos ven a 500. Otra cosa es que salga bien, todos sabemos de macroempresas y adquisiciones que no se han llevado bien y han acabado penalizando al accionista.

Should I be adding to CVS and Walgreen’s Later This Month?

Last week, I received questions from a few readers about CVS and Walgreen’s. The share prices behind both companies are taking a beating recently.

If share prices are low when the next newsletter comes out on Sunday, March 24th, there is a high chance that I will add at least a share of Walgreen’s to the Dividend Growth Investor Portfolio. There is a low chance that I will add to CVS however.

I like the valuation and earnings trends for CVS. However, I do not like the dividend freeze that was enacted in 2018, following the acquisition of Aetna. As a dividend investor, I look for companies that have managed to grow dividends for a certain number of consecutive years. This shows to me a commitment to raising dividends. This commitment means something when it is backed by rising earnings per share. Under an ideal scenario, a company will grow earnings and distribute a rising annual dividend per share. I want to buy a share in such a company, and enjoy rising earnings, dividends and share prices over time. Once this virtuous loop ends however, I start asking myself if something is wrong with the business.

As a result, when I see that management is no longer committed to growing dividends, it shows that they do not have a lot of conviction behind their earnings per share growth in the near term. By keeping dividends unchanged, management is really telling me that things are cloudy on the horizon, so that they do not believe that future earnings will justify growing the dividend. Without annual dividend increases, I am essentially stuck wondering whether something is wrong with the business, or this is just a temporary situation.

It is very likely that this is just a temporary measure, in order to get the balance sheet under control, reduce debt, integrate acquisitions etc. Once CVS starts raising dividends again, I will consider adding to the stock again. For my investment model to work, I need companies at an attractive valuation, growing earnings and growing dividends. That way I can keep investing $1,000/month, reinvesting dividends, and enjoying the organic dividend growth that will propel me to $1,000 in monthly dividend income within 10 – 15 years. If I invest in companies that never raise their dividends, it will take longer to reach my stated newsletter goal of generating $1,000 in monthly dividend income.

It is very likely that I am missing out on an incredible bargain today, by not adding to CVS. However, I also see risks of a dividend cut being increased as well. A lot of dividends cuts in the past have occurred in situations with a lot of debt, high payout ratios and major acquisitions.

My basic thought process is that if CVS prospers, I already have exposure to the stock, so I should do ok. If CVS fails, I will likely lose what amount I own there, but would have protected my new capital from going into a sinkhole. Plus, I would have allocated dividends elsewhere, and increased the diversification of my portfolio.

That being said, I am still considering Walgreen’s as an addition to my portfolio. I may even consider adding further after that. I have a high allocation to Walgreen’s, and want to avoid overly concentrating my efforts in once company. I like diversification, which is why I want to own as many companies as I can find, and also to limit their weight in my portfolio to a reasonable amount. I also like spreading my purchases over several months, in order to take advantage of potentially lower prices. The downside to this strategy is when share prices start going up in a linear fashion, and I haven’t build out my full position in a security. However, I believe that there are always good securities to be selected at the right valuation. My goal as a portfolio manager is to manage my risk properly.

I believe that my upside will take care of itself. I do want to place some fail-safe mechanisms in portfolio construction process, in order to reduce the magnitude of my errors when they occur. I also believe in maintaining a disciplined approach when investing my hard earned money. This is why the odds of me adding to CVS Corp are low.

Si alguien estaba esperando mejores precios para entrar, ahora mismo bajando 12% a 55,7 $

3 Me gusta

No han gustado los resultados del 2º trimestre. Baja el EPS un 8,8% y el guidance del 2019 pasa de un crecimiento del 7-12% a quedarse plano.

2 Me gusta

Hmmm, momento para recargar ? Como lo veis?

Yo tenía precio para empezar a mirarla sobre $52. Igual lo hago aunque no me llama mucho la empresa la verdad…

Por lo que leo, no están muy contentos con su directiva. Hay recorte de comisiones a los empleados y cierto descontrol en los puntos de ventas. Quizás la amenaza no sea únicamente Amazon. Dicho esto, compradas ayer a 55,68. Ahora la espero en los 50…que sin duda tocará. Junto con CVS, no sobrepasan el 3% de mi cartera americana.

1 me gusta

Walgreens’ (WBA) stock price fell 12.8% yesterday after releasing weak 2nd quarter 2019 results.

Key points from the earnings release are below:

-

Revenue grew 4.6% for the second quarter year-over-year

-

Adjusted earnings-per-share declined 5.4% year-over-year

-

Fiscal 2019 adjusted earnings-per-share guidance was reduced from growth of 9.5% at the median to "roughly flat".

CEO Stefano Pessina had the following to say:

“The market challenges and macro trends we have been discussing for some time accelerated, resulting in the most difficult quarter we have had since the formation of Walgreens Boots Alliance. During the quarter, we saw significant reimbursement pressure, compounded by lower generic deflation, as well as continued consumer market challenges in the U.S. and UK. While we had begun initiatives to address these trends, our response was not rapid enough given market conditions, resulting in a disappointing quarter that did not meet our expectations. As a result, we are now expecting roughly flat adjusted EPS growth for fiscal 2019.

We are going to be more aggressive in our response to these rapidly shifting trends. We are focusing on our operational strengths and addressing weaknesses, making a number of senior appointments to bring change and accelerating the digitalization and transformation of our business. This will include expediting the execution of our partnership initiatives, fully developing our in-store neighborhood health destinations, re-imagining our front end retail offering, optimizing our store footprint and increasing the annual savings goal of our transformational cost management program from in excess of $1 billion to more than $1.5 billion. As a result of these actions, our business model will deliver improved performance in fiscal 2020, positioning us for mid-to-high single-digit growth in adjusted EPS in the following year."

2nd quarter 2019 results were very clearly not good at Walgreens. All companies go through weak periods, and Walgreens is no exception.

But investors need to keep in mind that Walgreens stock was already heavily discounted before yesterday’s price decline. Walgreens shares are now trading for a price-to-earnings ratio of less than 10 using expected 2019 adjusted earnings-per-share of ~$6.00. For comparison, the security has traded for an average price-to-earnings ratio of 15.6 from 2009 through 2018.

And this is not the first time in Walgreens history that it has experienced an earnings contraction. In fiscal 2012, earnings-per-share fell to $2.53 from $2.64 the prior year. Earnings-per-share are expected to be around flat this year.

Walgreens has a long history of success as evidenced by its 43 consecutive years of dividend increases . The company’s management is especially shareholder friendly. In addition to its long dividend streak and current 3.2% dividend yield, Walgreens consistently repurchases its shares. The company’s share count is down 6.5% over the last 4 fiscal quarters alone.

CEO Stefano Pessina has an especially good track record at Walgreens since becoming CEO in 2015. In 2015, adjusted earnings-per-share were $3.88. They were $6.02 in fiscal 2018 for a compound rate of 15.8% annually. And Walgreens is being proactive and has a plan to return to growth after fiscal 2019.

We will be following Walgreens results closely. In our view, Walgreens remains a strong buy at current prices. We hope our readers will take a long-term view with the company and not sell based on yesterday’s price decline. We reiterate that Walgreens remains a buy today.

3 Me gusta