Strong First-Quarter Outperformance Prompts Us to Raise 3M’s Fair Value Estimate

Wide-moat rated 3M outperformed analyst expectations embedded in our full-year projections. On the heels of this outperformance, we raise our fair value estimate by 3% to $199 from $193. About $1 of the raise is due to some additional revenue credit in business divisions like oral care, advanced materials, and automotive and aerospace OEM. Another $1 of the raise is due to time value of money. The remaining $4 of the raise is due to some additional stage II EBI growth credit to rectify some conservatism in our numbers.

We also bumped up our full-year diluted EPS estimate to $9.70 from $9.67 as 3M delivered its biggest quarterly outperformance since this analyst has covered the stock (even as the stock sold down during trading). We think the sell-off was largely predicated on management maintaining its guide given some of the litigation risks it highlighted on the call, as well as some conservatism given that we’re only one quarter through the year. We encourage investors to take a closer look at the firm’s underlying fundamentals. Even when accounting for some normal seasonal drop-offs in some of its businesses, many appear to be outperforming some early market expectations; that’s why we model at the top of management’s earnings guide.

Turning to the quarter, overall top line grew 9.6% year on year to $8.9 billion, or 8% on an organic basis. Organic growth was fairly broad-based across all of 3M’s business segments, which was nice to see. Of course, what previously hurt 3M some quarters ago and was a strong positive contributor to its sales growth this time around was its exposure to the Asia-Pacific region (about 31% of mix during the quarter), and specifically China. Asia-Pacific grew just under 13% year on year on an organic basis (or just over 18% on a reported basis) and China grew 32% year over year. While this was no surprise given the path to recovery from the global pandemic, we were surprised by strength from EMEA, which grew 10.4% year on year.

Despite Solid Second-Quarter Print, We Lower 3M’s FVE as a Result of Expected U.S. Tax Reform

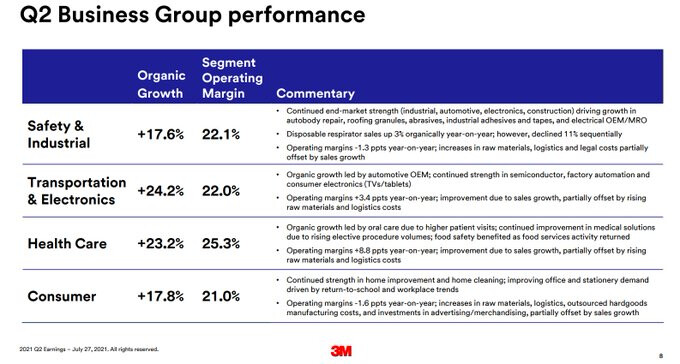

Wide-moat-rated 3M had solid second-quarter results. However, we lower our fair value estimate to $195 per share from $199 previously due entirely to our probability-adjusted U.S corporate tax rate of 26% beginning in 2022. Nonetheless, 3M turned in better-than-expected organic top-line growth, as our earnings and free cash flow projections moved higher, though our overall operating margin assumptions remained untouched. On the heels of this outperformance, management raised its EPS guidance range by 45 cents at the midpoint to $9.90, or good for just shy of a 5% raise. Management also tightened the EPS guide by a dime per share. Finally, management raised its full-year organic top-line guide by 3% to 7.5% at the midpoint.

We model just below that at 7.2%, of which only 40 basis points is thanks to price, in line with 3M’s historical experience, excluding electronics. We have a hard time believing 3M will manage to take price materially greater than this figure, particularly given the 10 basis point price-take observed during the second quarter. Nonetheless, there’s generally a couple quarter lag to take price, particularly since portions of 3M’s business is contractual, and it takes time for the firm to offset its raw material headwinds. For the second half, management is expecting that raw material and logistic-related headwinds persist and even exacerbate. The firm now expects between a 65 cent and 80 cent per share price-cost headwind versus the 40 cents or so prior. Nonetheless, we still see conservatism baked into the raised EPS guide due to management baking in a cushion on account of these headwinds. 3M should disproportionately benefit relative to the multi-industry category during this part of the cycle. More importantly, we see its long-term trends intact.

3M recibe un veredicto en contra de 22,5 millones de dólares en la última prueba de tapones para los oídos del ejército de EE. UU.

El juicio fue el octavo hasta ahora en llegar a un veredicto, y los demandantes en otros cuatro casos ganaron más de $ 29 millones combinados. Los jurados se pusieron del lado de 3M en otros tres, y se están llevando a cabo dos juicios más, y más por venir…

Tengo 4 spin-offs en mi cartera más 3 como mínimo que se prevén para el 2022, 3M, JMJ y AT&T, serán 7. A este ritmo mi cartera se dobla en número de posiciones sola.

Dentro de cada empresa suele haber algún garbanzo negro que puede estropear “el cocido” y que conviene soltar ahora que la gente traga ( ó tragamos) con cualquier cosa.

Supongo que es lo mismo que cuando las empresas que tienen renovables, venden una parte (ó todas las que tiene) para aprovechar que están “de moda” y tienen un precio que no se merecen.

No es que las empresas procedentes de spin offs sean malas, en la mayoria de casos es cuestion de negocios mas o menos estancados, que no encajan con las lineas de negocio a potenciar por la empresa, habitualmente de mas crecimiento esperado.

En estos casos yo sigo lo que dice @Juanmanuel si la empresa la vende, por algo sera, si fuera un negocio espectacular, la empresa se desharia de el? Seguro que no

Yo no he tenido de momento mas que la de Organon, y de momento ahi permanece, tal cual me la adjudicaron

Yo con esa parte de la empresa que van a desgajar seguramente haga como con OGN, la venderé. En cambio, los spin-offs de JNJ y GSK me los quedaré porque conozco de primera mano sus productos y son muy potentes.

Todo esto, claro, si antes no he liquidado toda la cartera y lo he metido en el World porque ya me empiezan a cansar los spin-offs esos.