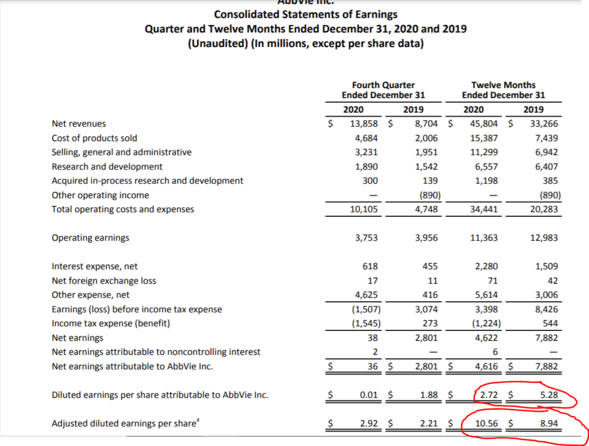

Si os fijáis en todas las webs usan los atribuibles a AbbVie pero luego incluyen los otros abajo. Claro cambia mucho el cuento de ganar la mitad a ganar bastante más que el año anterior. ¿En cuál os fijáis? ¿Sabéis cómo calculan los “Adjusted diluted earnings per share”?

Tendremos que empezar a consumir Botox jejejej

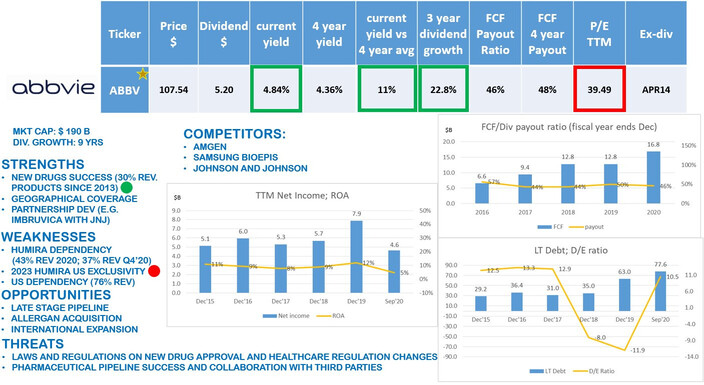

Si no entendí mal el problema viene con el medicamento Rinvoq (en USA, porque en Europa creo que ya se comercializa) que lo venden como el sucesor de Humira.

AbbVie Posts Strong Q2 Results, Driven by New Immunology Drugs and Accelerating Allergan Products

AbbVie reported second-quarter results that were ahead of our projections, and we are raising our fair value estimate to $108 from $103. With this minor increase, we view the stock as slightly overvalued, with some concern that the market is overly focused on recent and likely near-term strong growth rather than the major U.S. biosimilar pressure against Humira starting in 2023. The biosimilar pressure on such a key drug (over a third of total sales) is a key reason for our narrow rather than wide moat rating on the stock despite a remaining portfolio that is executing well.

In the quarter, total sales increased 19% on a comparable operational basis after adjusting for the Allergan acquisition, but we expect decelerating growth by 2023 due to the biosimilar pressure. Despite the approaching pressures, we expect AbbVie’s resilient next-generation immunology drugs Skyrizi and Rinvoq to help mitigate Humira biosimilars as the new drugs already represent close to 20% of Humira sales, and we expect further entrenchment in current and new indications to propel growth to represent a third of Humira sales in 2022, the last year of exclusivity for Humira in the U.S. While the Food and Drug Administration is delaying approvals in important new indications for Rinvoq, we believe the drug will gain several important new indications (including atopic dermatitis and ulcerative colitis) with the FDA’s safety concerns largely addressed within the label of the drug.

Also helping long-term growth, the recently acquired Allergan products are performing well. We believe AbbVie’s increased marketing spending on the products are helping to propel growth. In particular, Botox (both cosmetic and therapeutic) is posting excellent growth even after adjusting for an easy year-over-year comparison. Also, the strong launch of acute migraine drug Ubrelvy sets up a good pathway for the likely 2021 approval of atogepant in migraine prevention.

)

)