Pues… Menos mal que no compré la semana pasada que estuve a punto  han caído hoy 6 y a seguir monitorizando

han caído hoy 6 y a seguir monitorizando

Eso mismo pensé yo, sin llegar a hacerlo, para entrar en Pfe a menor precio hace ya un tiempo. Deseché la idea y compré Pfe directamente.

Saca tus conclusiones…

3 Me gusta

Veo que ha entrado en vigor esta regla para ABBV hasta mañana por la noche. No termino de entender su significado y las implicaciones que pueda tener sobre la cotización. A ver si alguien que controle nos lo explica con lenguaje sencillo.

Adoption of Alternative Uptick Rule

In 2010, the SEC constructed an alternative uptick rule to restrict short selling from further driving down a stock price that has dropped more than 10% in one day. It’s designed to enable investors to exit long positions before short selling is triggered. The alternative uptick rule is triggered when a stock experiences a price decline of at least 10% in one day. At that point, short selling would be permitted if the price of the security is above the current best bid. This aims to preserve investor confidence and promote market stability during periods of stress and volatility.

The rule includes the following features: short sales related circuit breaker, duration of price test restriction, securities covered by price test restriction, and implementation. In other words, most securities are covered by the rule and in the event it is activated, the alternative uptick rule would apply to short sale orders for the remainder of the day as well as the following day.

2 Me gusta

Es una regla antigua que ha ido yendo y viniendo.

Esta prohibe ponerse corto si el ultimo tick no ha sido alcista.

Es un poco diferente a la prohibicion de ponerse cortos que lo han restringido a veces que implica no tener posiciones cortas “desnudas”, sin que las hayan pedido prestadas antes.

Es dificil de explicar, pero son 3 restricciones que se van incrementando.

a) no puedes ponerte corto si el ultimo precio cruzado no ha sido al alza

b) no puedes ponerte corto si no tienes las acciones de otro prestadas

c) prohibicion total de ponerse cortos

No se si lo he liado mas jjjjjjjjjjjjjjjjj

7 Me gusta

Las opciones negativas principales son que no se apruebe la compra por alguna parte, con lo que caería mucho.

Que les obliguen a vender productos a la competencia (no parece que afecte mucho) o que haya algún otro comprador o no afecta a AGN o es positivo.

Como en el caso reciente de BMY y CELG creo que lo más probable es que se lleve a cabo. Pero nunca se sabe, es importante ver quiénes son los que tienen las acciones de las diferentes compañías y en qué porcentajes. Estas cosas suelen estar bastante atadas antes de lanzarse…

4 Me gusta

Rick Gonzalez

Okay. On the dividend, look, again, this just assures that we can continue to drive a strong and growing dividend. We’re absolutely committed to a growing dividend, and nothing has changed. And this gives us a higher level of assurity to be able to continue to do that at a robust rate.

3 Me gusta

La conference call sobre la compra de Allergan:

Y un extracto en el que le preguntan al CEO por el tema del dividendo:

“Okay. On the dividend, look, again, this just assures that we can continue to drive a strong and growing dividend. We’re absolutely committed to a growing dividend, and nothing has changed. And this gives us a higher level of assurity to be able to continue to do that at a robust rate.”

Un saludo.

P.D.: Fuimos a lo mismo pero le diste más rápido al send. Es lo que tiene saber ser conciso ![]() .

.

2 Me gusta

Yo de los Richards me fío poquito

Teniendo razón, creo que a corto a pesar de haberse cargado con un volquete de deuda, el dividendo no debería correr peligro. Ya han dicho que van a repagar unos 20B hasta final de 2021 y luego más hasta 2023.

Que es lo que deberían hacer para aprovechar lo que quede de Humira, porque como no reduzcan deuda y bajen las ventas más de lo esperado, el problema es gordo.

Habrá que seguir las ventas y la reducción de deuda…

3 Me gusta

Es una compra muy grande y la incertidumbre se refleja en el precio de la acción de forma considerable. Aunque debatamos horas sobre el tema, creo que al final sólo el tiempo aclarará las cosas.

Que el CEO hable en ese tono del dividendo en un principio parece bueno, pero ya sabemos que en muchas ocasiones mienten, como con VOD, y que los deseos o intenciones a veces chocan con la realidad: la deuda.

Yo conozco profesionalmente algunos productos de Allergan y siempre me han parecido muy buenos, o de los mejores en su grupo, aunque por lo que he leído la gestión de la empresas no ha sido muy ejemplar.

Pero a pesar de estar el río revuelto, yo he comprado al final de la sesión y he alcanzado media posición completa. Ahora paciencia y cruzar los dedos.

5 Me gusta

Tras el susto inicial, he acabado digiriendo la noticia y, además de todos los riesgos, veo el sentido de la adquisición. De la conferencia me gusta especialmente la frase del presidente de “el cash flow de Humira va a pagar por sus sustitutos”. Y la intención de mantener el dividendo creciente, claro.

He puesto una orden a 65 que se ha quedado a centavos. A ver si mañana entra.

2 Me gusta

As you may have heard, AbbVie (ABBV) announced this morning its intention to acquire Allergan (AGN) in a transformative move for both companies.

AbbVie is a past recommendation of both the Sure Dividend Newsletter and the Sure Retirement Newsletter.

This email serves to update our members on our view of Abbvie following the announcement of this transaction.

Terms of the Transaction

To understand the implications of the Allergan transaction on AbbVie’s business, investors must first understand the terms of the transaction. Accordingly, we’ll open this email by discussing the terms of the deal as outlined in AbbVie’s original earnings release:

“Under the terms of the Transaction Agreement, Allergan Shareholders will receive 0.8660 AbbVie Shares and $120.30 in cash for each Allergan Share that they hold, for a total consideration of $188.24 per Allergan Share. The transaction represents a 45% premium to the closing price of Allergan’s Shares on June 24, 2019.”

The per-share purchase price represents a transaction equity value of approximately $63 billion. For context, AbbVie has a current market capitalization of $97 billion (note that this market capitalization figure includes the impact of today’s tremendous price drop following the announcement of the Allergan acquisition).

The size of the acquisition means that the transaction will be deeply transformative for both companies. Here’s what AbbVie’s Chairman and Chief Executive Officer, Richard A. Gonzalez, said about the purchase in the press release:

“This is a transformational transaction for both companies and achieves unique and complementary strategic objectives. The combination of AbbVie and Allergan increases our ability to continue to deliver on our mission to patients and shareholders. With our enhanced growth platform to fuel industry-leading growth, this strategy allows us to diversify AbbVie’s business while sustaining our focus on innovative science and the advancement of our industry-leading pipeline well into the future."

And Allergan’s CEO Brent Saunders said the following:

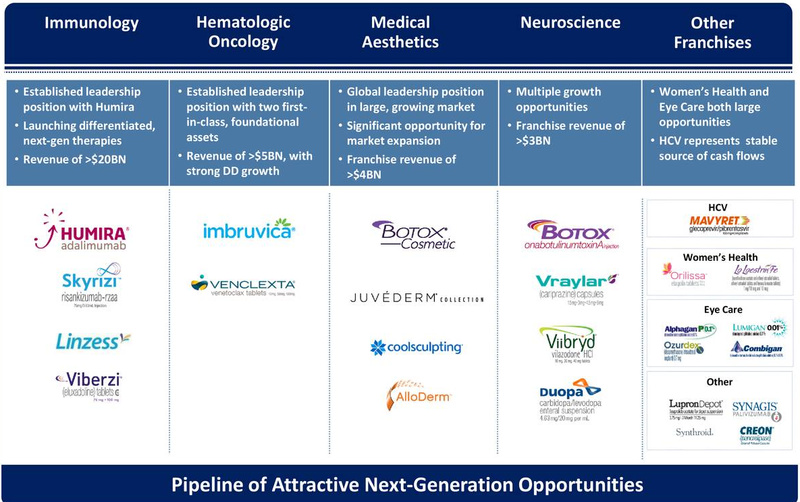

"This acquisition creates compelling value for Allergan’s stakeholders, including our customers, patients and shareholders. With 2019 annual combined revenue of approximately $48 billion, scale in more than 175 countries, an industry-leading R&D pipeline and robust cash flows, our combined company will have the opportunity to make even bigger contributions to global health than either can alone. Our fast-growing therapeutic areas, including our world class medical aesthetics, eye care, CNS and gastrointestinal businesses, will enhance AbbVie’s strong growth platform and create substantial value for shareholders of both companies.”

AbbVie expects the transaction to be 10% accretive to adjusted earnings-per-share over the first full year following the close of the transaction, with peak accretion of greater than 20%. Moreover, AbbVie expects the return on invested capital of the transaction to exceed AbbVie’s cost of capital within the first full year.

Upon the completion of the transaction, AbbVie will continue to be incorporated in Delaware as AbbVie Inc. and will continue to be led by Richard A. Gonzalez. Two members of Allergan’s board (including current Chairman and Chief Executive Officer Brent Saunders) will join AbbVie’s board upon the transaction’s close.

Synergies & Capital Structure

As with most corporate mergers, AbbVie expects to generate significant synergies from its acquisition of Allergan. The following passage from the press release details these synergies:

“AbbVie anticipates that the Acquisition will provide annual pre-tax synergies and other cost reductions of at least $2 billion in year three while leaving investments in key growth franchises untouched. The synergies and other cost reductions will be a result of optimizing the research and early stage portfolio, and reducing overlapping R&D resources (~50%), driving efficiencies in SG&A, including sales and marketing and central support function costs (~40%), and eliminating redundancies in manufacturing and supply chain, and leveraging procurement spend (~10%). The synergies estimate excludes any potential revenue synergies.”

AbbVie’s capital structure will be more leveraged following the transaction, as a portion of the cash component of the offer will be funded with new debt. AbbVie had $36.6 billion of total debt at the time of its most recent quarterly earnings release.

Fortunately, the company is committed to a Baa2/BBB or better credit rating. AbbVie also issued a new debt reduction target of $15 billion to $18 billion by 2021 with the publication of its Allergan acquisition press release.

Because of this, we do not believe that AbbVie’s debt will rise to troublesome levels following the acquisition of Allergan.

AbbVie’s Enhanced Growth Prospects

The most striking factor of this newly-announced acquisition is the positive impact that it has on AbbVie’s long-term growth prospects. AbbVie’s business can be divided into two main categories:

- Humira: $4.4 billion of revenue last quarter

- Non-Humira drugs: $3.4 billion of revenue last quarter

AbbVie’s flagship drug, Humira , contributes more than half of the company’s overall sales. Perhaps more importantly, Humira comes off patent in 2023, which means that it will face significant competition from biosimilars within the next four years. This means that it is extremely important for AbbVie to identify and pursue new growth opportunities.

The Allergan acquisition seems largely suited to fulfill this purpose. The following excerpts from today’s acquisition conference call elaborate on this (note that AbbVie’s “growth platform” refers to all of its non- Humira drugs):

“With today’s announcement AbbVie’s growth platform will be put on a course to achieve immediate standalone scale with sales of more than $30 billion in 2020 and best-in-industry growth prospects.”

“With revenue of more than $30 billion in 2020, we expect our growth platform to drive high-single-digit annual growth over the next decade. Given the scale and growth prospects, we will have increased capacity to pursue the most promising and innovative science, which remains the core focus for AbbVie, and what makes the difference for the many patients we serve.”

Indeed, it’s hard to overstate how important this diversification benefit could be for AbbVie moving forward. For years, AbbVie has traded at a pessimistically cheap valuation very likely due to the Humira patent cliff. The reduction of this risk has the potential to meaningfully increase AbbVie’s valuation multiple moving forward.

Valuation of the Transaction

A key component of any acquisition is the price paid by the acquiring company. In transactions where the acquiring company is paying with stock (such as this one), the valuation of the purchasing company’s shares must also be considered. We explore both elements of the acquisition below.

First off, let’s discuss Allergan’s valuation. AbbVie’s management team clearly believes it is capturing an appealing value. On this afternoon’s conference call, the company made the following statement:

“Assets of the quality of Allergan are not always available, and certainly not at this value. The opportunity to access these attractive durable franchises and immediately rescale on our growth platform, and at the same time, have ample HUMIRA cash flow to deleverage before the U.S. LOE, is an incredibly compelling opportunity, and one that we did not want to pass up.”

Note: LOE stands for “loss of exclusivity”.

Let’s ignore what AbbVie’s management team says about the transaction (after all, they have a vested interest in the transaction closing successfully) and examine the numbers.

The total consideration for AbbVie’s purchase of Allergan is $188.24 per share, comprised of $120.30 in cash and 0.8660 units of AbbVie stock. In Allergan’s first quarter earnings release, the company stated that it expects to generate adjusted earnings-per-share of $16.55 in fiscal 2019.

Using this guidance and the transaction’s total consideration price, the acquisition implies a price-to-earnings ratio of 11.4. For context, Allergan has traded at an average price-to-earnings ratio of 14.1 over the last decade. AbbVie investors should be pleased to see that the company is acquiring Allergan at a noticeable discount to its long-term average valuation multiple.

On the other hand, the shares being issued by AbbVie to fund the transaction are also undervalued, which troubles us and makes the dilution associated with the transaction even worse.

Using yesterday’s closing price of $78.45 and the company’s fiscal 2019 adjusted earnings-per-share guidance of $8.78, AbbVie’s stock was trading at a price-to-earnings ratio of 8.9 before the transaction was announced. Issuing stock at 8.9 times earnings to acquire another company at 11.4 times earnings does not seem like a winning strategy in our view.

Moreover, AbbVie’s management team unquestionably recognizes that the stock is trading below intrinsic value. AbbVie completed a tender offer for $7.5 billion of its common stock in June of 2018 at a price of $103 per share. To put it bluntly, it makes no sense for AbbVie to repurchase shares at $103 only to issue them at $78 (or even lower after today’s price action) a year later to fund the purchase of Allergan.

To conclude this section, we believe that the valuation being paid for Allergan’s stock is quite attractive, but AbbVie’s common shares are even more undervalued. We would be more supportive of this transaction if it were capable of being funded entirely by cash. With that said, we are glad that the majority of the purchase price (64%, or more if AbbVie’s stock continues to fall) is being funded by cash.

Accretion of the Transaction

AbbVie stated in today’s press release that it expects “immediate” 10% accretion to earnings-per-share. To close out today’s email update, we thought we would perform some back-of-the-envelope calculations to see what is likely to happen to AbbVie’s earnings-per-share following the acquisition’s close.

First, let’s determine the base case for AbbVie’s adjusted earnings-per-share in 2019 assuming the Allergan acquisition was not announced. The easiest way to do this is by looking at the company’s financial guidance.

When AbbVie reported first quarter earnings on April 25th, the company updated its 2019 financial guidance to adjusted earnings-per-share of $8.73 to $8.83. We’ll use the midpoint of this guidance band ($8.78) for AbbVie’s base case earnings.

Next, let’s determine a ‘bear case’ for AbbVie post-acquisition that assumes no synergies. In other words, let’s see how much the combined company would earn on a per-share basis by including Allergan’s earnings and accounting for the dilution associated with the transaction.

First, let’s determine AbbVie’s contribution to earnings. The company is guiding for adjusted earnings-per-share of $8.78 and currently has 1,483 million diluted shares outstanding, which implies company-wide net income of $13.0 billion in the full fiscal year.

Next, let’s determine Allergan’s contribution to net income. In Allergan’s first quarter earnings release, the company revised its 2019 financial guidance, which now calls for adjusted earnings-per-share of $16.55 and an average 2019 share count of 332.0 million. This implies company-wide adjusted net income of $5.5 billion.

So together, the combined company should be capable of generated $18.5 billion of adjusted net income (AbbVie’s $13.0 billion plus Allergan’s $5.5 billion) in the current fiscal year.

Lastly, let’s determine how many outstanding shares the pro-forma company will have following the merger and use this figure to determine an estimate for 2019 earnings-per-share for the new company.

AbbVie is issuing 0.8660 AbbVie shares per Allergan share and there are approximately 332 million Allergan shares outstanding, so the merger will create 294 million new AbbVie shares. AbbVie had 1,483 million diluted shares outstanding at the time of its latest earnings release, so the new share count would be 1,777 million.

We are now equipped with all of the information required to compute a 2019 earnings-per-share estimate. Dividing the pro-forma company’s adjusted net income of $18.5 billion by its estimated share count of 1,777 million, we get adjusted earnings-per-share of $10.41.

Since this is significantly higher than AbbVie’s 2019 financial guidance of $8.78 in adjusted earnings-per-share and does not account for any synergies , we believe that the merger will indeed be accretive for AbbVie, especially if the company can achieve its target $2 billion in synergies post-merger.

Final Thoughts

When we first read about AbbVie’s acquisition of Allergan, our first thought was that the acquisition has the potential to nicely diversify the company’s revenue away from its flagship drug Humira . However, we were alarmed to see the stock drop 16% in today’s trading and wondered if there were valid reasons for this price movement.

Fortunately, the analysis that we have performed and shared with you in this email shows that the Allergan acquisition seems to be a positive event for AbbVie’s long-term investors. Even without accounting for any cost synergies, some back-of-the-envelope math shows that it could be powerfully accretive for existing shareholders. Because of this, we are reiterating our buy recommendation on AbbVie today.

7 Me gusta

You may have heard the news that Abbvie (ABBV) is in talks to acquire biotech Allergan (AGN) in a transaction valued at $60 billion. Abbvie will offer $120.30 in cash plus 0.8660 in Abbvie shares for each Allergan share.

When I analyzed Abbvie in September of last year, I did mention the following:

Perhaps Abbvie could similarly acquire growth through acquisitions as well. Hopefully they do not overpay for those acquisitions, and do not decide to cut the dividend in the meantime.

This deal will allow Abbvie to diversify its revenue stream away from blockbuster drug Humira, which accounts for a very large portion of revenues and earnings. Humira is losing its exclusivity in the US after 2023. This deal will also bring in synergies, and bring in new drugs in various stages of development. The synergies will be mainly from a reducing duplication in SG&A, R&D, and consolidating manufacturing operations. The acquisition price is roughly half what Allergan was going for, when Pfizer walked out of its deal to acquire it a few short years ago.

After the announcement, Allergan shares went up, while Abbvie’s share price nosedived by over 16%. This decline pushed the dividend yield to 6.50%.

It looks like the market participants did not like the deal. Perhaps it is because this deal will increase Abbvie’s debt significantly, and reduce financial flexibility. My research has identified increased debt following an acquisition spree as one of the predictors of a future dividend cut. I am not predicting that Abbvie will cut dividends, but I do believe that the market considers the risk of a dividend cut to be elevated today, versus last week.

It is also possible that the deal strikes as desperation, because Abbvie does not have the drugs to offset the effects of declining sales and profits from Humira after 2023. Allergan has not grown revenues for a couple of years.

The real question for dividend investors today is, “how safe is the dividend”?. My answer is that it depends on how each individual investor decides to evaluate sustainability. At current rates, the annual dividend is at $4.28/share.

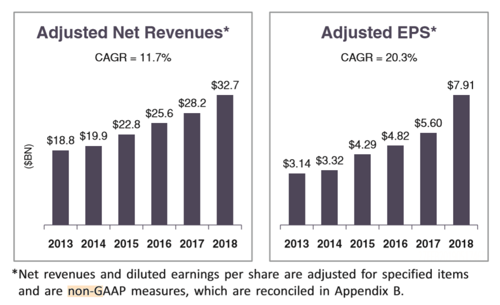

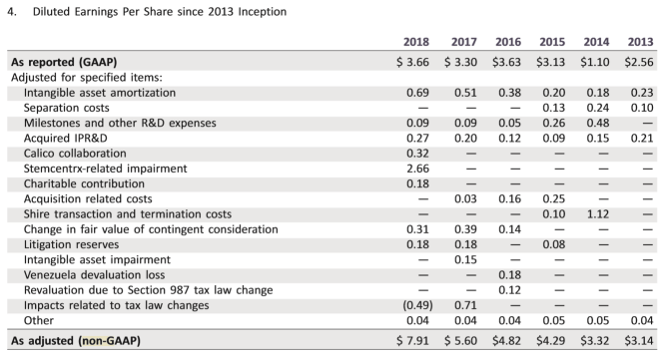

Based on Non-GAAP earnings per share, Abbvie has managed to grow the bottom line since it separated from Abbot at the end of 2012.

However, if you focus on GAAP earnings per share, it looks like the profits did not increase at all since 2013.

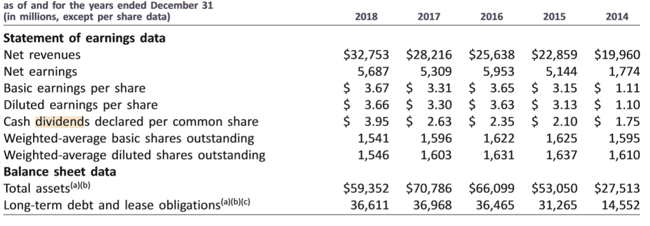

It looks like annual dividends have increased from $1.75/share in 2014 to $3.95/share in 2018. Abbvie hiked its quarterly dividends to $1.07/share in the last quarter of 2018. This brings the annual dividend to $4.28/share.

I do believe that the answer is somewhere in the middle. However, I do believe that the combined company has a lower margin of safety in dividends than before. It is very likely that any short-term pressures on management due to a more challenging competitive position, or a more challenging economic or financial environment may prompt them to freeze dividends and even cut them if they have to.

The stock price is lower, and could be a bargain today at 8.30 times adjusted non-gaap earnings and a dividend yield of 6.50%. The adjusted non-gaap payout ratio looks ok at 54%. Using GAAP earnings, the P/E ratio is at 17.80 but the dividend payout ratio is above 100%.

However, there is a higher risk of a dividend cut down the road due to increase in debt by an estimated $38 billion, from the current level of long-term debt of $36 billion. There are always risks in integrating two separate cultures, which may reduce the amount of synergies that are actually realized. We also have risks that the existing revenues for Humira decline faster than expected and sooner than expected, pressuring management to pay off debt using funds for dividends and buybacks.

If you are an investor who may not worry if a company they buy cuts dividends on them, perhaps Abbvie could be worth further researching. If it turns out ok, similar to how Pfizer turned out after its 2009 dividend cut, good returns could be generated. If it doesn’t however, you will have the double whammy of lower dividends and lower net worth for the portion allocated to Abbvie.

6 Me gusta

Este análisis me gusta más y me parece más acertado que el de sure dividend.

2 Me gusta

Este hombre suele tener “algo” de idea de lo que habla, y no veía con malos ojos a Abbvie antes y no parece verla con malos ojos ahora tampoco.

Un saludo.

Y esta gente que está especializada en healthcare acaba de publicar sus revisiones y a ABBV le ha subido su valoración un 40%.

Un saludo.

1 me gusta

Lo que dice esta gente y similares mejor no creerse mucho. Hay mejores y peores analistas, pero muchos recomiendan cosas dependiendo qué les interese.

Hay mucho movimiento oculto por detrás…

3 Me gusta

2 Me gusta

ABBV es una empresa que como le funcione el portfolio de productos en investigación puede ser un bombazo.

Eso si, como no le funcione se puede ir a los infiernos.

2 Me gusta