Adidas venderá tres marcas de golp por 425 millones de dólares a finales de 2017 y mantiene sus previsiones de beneficios para el 2017 a pesar de estas ventas.

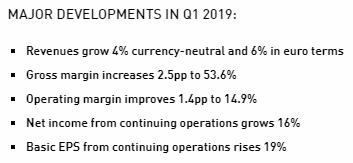

Revenues grow 4% currency-neutral and 5% in euro terms

Gross margin increases 1.2pp to 53.5%

Operating margin improves 0.4pp to 11.7%

Net income from continuing operations grows 10%

Basic EPS from continuing operations rises 13%

adidas confirms outlook for FY 2019

The company continues to expect sales to increase at a rate of between 5% and 8% on a currency-neutral basis.

Adidas continues to project a sequential acceleration during the second half of the year.

The company’s gross margin is forecast to increase to a level of around 52.0% (2018: 51.8%) in 2019.

The operating margin is expected to increase between 0.5 percentage points and 0.7 percentage points to a level between 11.3% and 11.5% (2018: 10.8%).

Net income from continuing operations is projected to increase to a level between € 1.880 billion and € 1.950 billion, reflecting an increase of between 10% and 14% compared to the prior year level of € 1.709 billion.

Ya no se trata de situación financiera, la de Adidas no es mala, es simplemente cultura. Si Adidas o LVMH fuesen de USA seguirían pagando a base de deuda a corto plazo este año y a correr.

Si, si, la vi jejeje. Pero bueno, tampoco es ir a por dividendo puro y duro con Adidas sino que es comprar una gran empresa que en un año está a un tercio de su precio. El 95% que tengo es USA y quiero diversificar. Adidas en este momento me parece muy apetecible. Ya no cuento con su dividendo.