Altria estaría en +20% premarket y en 2 semanas a 120$ porque crecería al +20% anual según estimaciones. Yo me apunto!

4 Me gusta

En el enlace lo explica claro clarinete…

¿Esta pasando? ¿Reddit se fija en el tabaco?

4 Me gusta

Ostia, estaría bien…

A ver si van a ser estos y no el interés compuesto los que me hacen IF

4 Me gusta

Creo que el titular es un poco erroneo no?

Lo que yo habia entendido es que en beneficios estan por debajo de lo estimado y los ingresos por encima de los previstos por los analistas. Pero me ha parecido leer antes que eran mejores en ambos casos que el 2019.

Nuestros expertos Tabaqueros nos aportaran seguro un poquito mas de luz…

Sinceramente ese titular está un poco forzado.

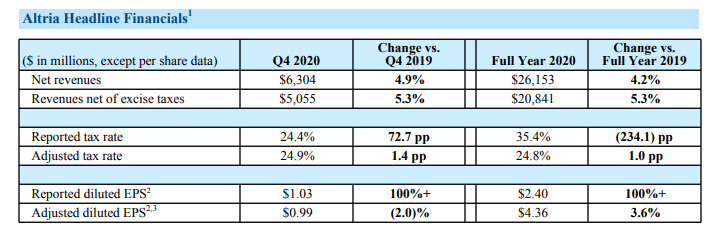

Los resultados:

Ingresos subiendo un 4-5%, beneficio subiendo un 3,6%, comenzando una recompras de acciones del 2,5% de la compañía y a PER<10. Y con expectativas de seguir creciendo en 2021:

Altria expects its 2021 full-year adjusted diluted EPS to be in a range of $4.49 to $4.62, representing a growth rate of 3% to 6% from an adjusted diluted EPS base of $4.36 in 2020.

20 Me gusta

Exacto, así lo había entendido yo

Gracias @juanjoo por la aclaración

1 me gusta

31/01/2021

Altria reported another robust performance at the top line in the fourth quarter of 2020. Although we are not changing our $54 fair value estimate, this performance increases our conviction that Altria is undervalued.

Full-year 2020 net revenue grew by 5.3%. This is a rate some other large cap fast-moving consumer goods companies, trading at much higher valuations, can only dream of in the current environment. Even making allowances for what seem likely to be higher channel inventory levels, we estimate revenue grew by almost 4%. Cigarette volumes fell by 0.4% (and by around 3% on an underlying basis, in line with the third quarter), and oral tobacco volumes were also down only very modestly, implying almost 6% price/mix across the portfolio last year. This is a strong performance for two reasons. First, cigarette volumes have been robust in spite of the disruption caused by COVID-19. We believe smokers are consuming more at home than they would if they had been in the office, and this has been confirmed by other commentary and data points by other cigarette manufacturers. While this tailwind may ease after the pandemic is under control, economic stimulus measures in the U.S., which seem likely to continue under the new Democrat-dominated government, have also supported the spending of low-income workers. Second, mid-single-digit price/mix contradicts the notion, misplaced in our view, that the tobacco algorithm is broken. Volumes in 2020 were no doubt supported by consumers switching back to cigarettes from vaping, and Altria estimates the vaping category fell by 10% in 2020. We expect the decline rate to revert to the high end of historical norms of around 3.5%, once that impact is cycled. This should ensure that Altria can grow its top line at a low-single-digit rate in the medium term, and we believe this is not being fairly priced into the company’s market value.

10 Me gusta

De quien es esta valoración @anbax? Morningstar?

De la estrella de la mañana efectivamente

1 me gusta

Buena análisis. Estoy dando vueltas a salir ya de BPY y doblar posición en Altria. Tengo que reposar la idea un poco más ya que se convertiría en la 5ª posición de mi cartera en valor actual y la 1ª en dividendos y en dinero invertido…

6 Me gusta

https://charioteerinvesting.com/mo-4q20-earnings-analysis-buyback-announced/

Análisis de los resultados del cuarto trimestre y una valoración dfc al final mirando el escenario más negativo.

Es curioso que no le da mucha importancia a la María (Cronos) en el futuro.

Saludos

6 Me gusta

Como dirían los value, el crecimiento de Cronos y su impacto te lo llevas gratis. Si funciona, genial, y si no te quedas en la hipótesis más pesimista

3 Me gusta

Falsa alarma… joder que susto…

1 me gusta