Hola, no llevo aún nada de Altria (ni del sector del tabaco) y llevo tiempo esperando a que deje de caer de precio para entrar. Cómo veis entrar a precios actuales?

Philip Morris ha dado resultados mejor de lo esperado, así que supongo que las otras tabacaleras también lo darán. Ya parece que pasó la tormenta en ellas.

Un saludo.

2 Me gusta

Acertar el fondo es utópico.

Para los que ya vamos cargados, $50 quizá no sea un precio muy atractivo comparado con los últimos tiempos…

Pero para abrir posición a mí me parece genial. Es un 35% arriba del mínimo de 52 semanas y, muy importante, el dividendo es un 33% a la media de 5 años.

4 Me gusta

Muchas gracias por vuestra ayuda , da gusto ;-). Al final me he decido y he entrado.

5 Me gusta

Hola, alguien que entienda de fundamental, que os parecen los resultados? he leido bastantes opiniones contrapuestas y la verdad no se que pensar…

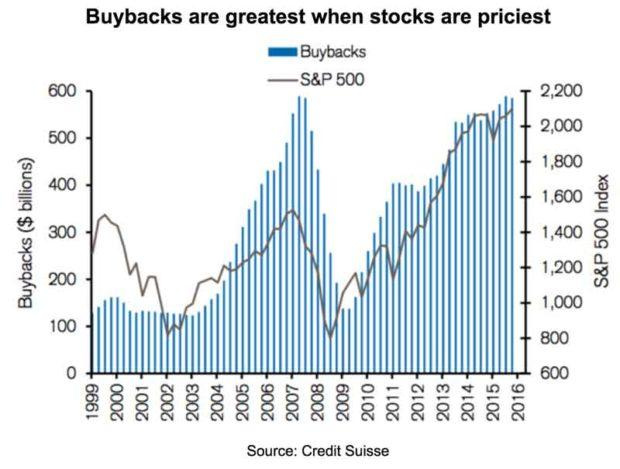

Es una opinión un poco subjetiva y probablemente con poco fundamento pero a mí cuando empresas como MO, AOS o WBA (por citar las más recientes) se ponen a recomprar acciones como si no hubiese mañana una voz interior me dice que deben estar a precio de saldo. Pero seguro que si @alvaromusach se pasa por el foro después de las vacaciones me desarma la argumentación en un pispas

3 Me gusta

No han gustado las previsiones de caida del volumen de cigarrillos tradicionales para los proximos años.

A pesar de todo ha mantenido las previsiones de beneficio por accion

3 Me gusta

Diria que en general las empresas son malisimas recomprando sus propias acciones.

4 Me gusta

Altria posted a solid second quarter that was slightly better than our estimates with flattish volumes and 6% revenue growth, but a slightly weaker-than-anticipated operating margin meant that EBIT was in line with our forecast. We are reiterating our $58 fair value estimate and wide moat rating. The stock sold off, however, because management lowered its guidance for industry volumes both for this year and in the medium term. Although we think the medium-term acceleration in volumes is not in itself a cause for alarm, given that Altria’s strategic investments in JUUL and other adjacent categories is likely to cannibalize cigarettes, we remain skeptical that the company can replicate its cigarette margins in these other businesses.

The year-to-date industry volume decline of 5.5% implies a sequential slowdown, but it is still well above the decline rate of recent years of around 3% to 4%. Management has guided that the industry will be down 5% to 6% this year, down a full percentage point at both ends of the range. We believe the biggest driver of this is likely to be the raising of the minimum smoking age to 21 in 18 states–around half of the U.S. population. JUUL will also have cannibalized some cigarette volume, although it is not likely that the introduction of iQOS in September will cannibalize cigarette volumes materially this year, as we expect distribution beyond the initial test market of Atlanta to roll out fairly slowly.

The key risk to Altria’s story is that margins in the emerging categories will not replicate those of its core business, cigarettes. The second-quarter operating margin was up a healthy 60 basis points, but this was boosted by a cost savings program that will have finite impact. Our base case assumption is that margins will mildly fade over the next five years due to negative mix and lower cost reduction programs, and faster migration to adjacent categories may heighten this risk. Nevertheless, we see modest upside to the shares.

2 Me gusta

Hablando en general no me atrevería a afirmar lo contrario, ya que tirar el dinero de otros es un ejercicio muy fácil.

Pero si juntamos que los fundadores tengan un porcentaje relevante de la empresa con la recompra de acciones, diría que la conclusión sería justo la contraria. Tirar el dinero de uno mismo suele ser más complicado. Mira a Aengus Kelly, cuya tesis está muy bien explicada primero por Estebaranz y luego por Horos.

4 Me gusta

Second Quarter

- Net revenues increased 5.0% to $6.6 billion, primarily due to higher net revenues in the smokeable products segment. Revenues net of excise taxes increased 6.4% to $5.2 billion.

- Reported diluted EPS increased 8.1% to $1.07, primarily driven by higher reported operating companies income (OCI), higher reported earnings from Altria’s equity investment in ABI and lower income taxes, partially offset by higher interest expense and 2019 Cronos-related special items.

- Adjusted diluted EPS increased 8.9% to $1.10, primarily driven by higher adjusted OCI in the smokeable and smokeless products segments, higher adjusted earnings from Altria’s equity investment in ABI and lower spending as a result of Altria’s decision in 2018 to refocus its innovative products efforts, partially offset by higher interest expense.

First Half

- Net revenues decreased 1.3% to $12.2 billion, primarily due to lower net revenues in the smokeable products segment. Revenues net of excise taxes increased 0.3% to $9.6 billion.

- Reported diluted EPS decreased 16.6% to $1.66, primarily driven by 2019 Cronos-related special items, higher interest expense (which includes acquisition-related costs associated with the JUUL and Cronos transactions) and lower reported earnings from Altria’s equity investment in ABI, partially offset by higher reported OCI.

- Adjusted diluted EPS increased 2.0% to $2.00, primarily driven by higher adjusted OCI in the smokeable and smokeless products segments and lower spending as a result of Altria’s decision in 2018 to refocus its innovative products efforts, partially offset by higher interest expense.

2019 Full-Year Guidance

- Altria reaffirms its guidance for 2019 full-year adjusted diluted EPS to be in a range of $4.15 to $4.27, representing a growth rate of 4% to 7% from an adjusted diluted EPS base of $3.99 in 2018.

1 me gusta

Altria sube el dividendo trimestral de 0.80$ a 0.84$ y se convierte en Dividend King (50 años consecutivos subiendo el dividendo o mas).

17 Me gusta

Se lució S&P cuando la sacó de la lista de Dividend Aristocrats después del spinoff de Philip Morris.

Menos mal que estaba el difunto Dave Fish para poner las cosas en su sitio

p.s. incremento del 5% y forward yield 7.20% … no está nada mal.

6 Me gusta

Desde luego, yo estoy aguantándome las ganas de entrar a ver hasta donde puede bajar…

Espero una buena noticia, algo relevante que haga que se corte la sangría, Beat and Raise ^^

A mi precio se pone en un 7,44% YOC aunque siendo conservador hubiera preferido un aumento del 3% y el resto a reducir deuda que con lo de Juul ha crecido bastante, pero oye a nadie le amarga un dulce.

6 Me gusta

¿El próximo dividendo ya va con la subida o desde qué fecha aplica esta subida?

Sí, el próximo

Altria (NYSE:MO) declares $0.84/share quarterly dividend, 5% increase from prior dividend of $0.80.

Forward yield 7.26%

Payable Oct. 10; for shareholders of record Sept. 16; ex-div Sept. 13.

3 Me gusta

Y esta parte pasó un poco desapercibida cuando presentó resultados a finales del mes pasado

“Altria’s Board authorized a new $1 billion share buyback program, which it plans to complete by the end of 2020. The company repurchased 3.7 million shares in the second quarter at an average price of $52.93 per share, for a cost of $195 million”

5 Me gusta

Vaya precios !! ![]()

3 Me gusta

Una pregunta sobre eso de la fusión com PM… ¿Alguien sabe cómo va a quedar el canje de acciones de altria y el dividendo si se juntan? En algún sitio he leído que altria se llevaría un 40% y pm el 60% restante. En mi caso que tengo 100 acciones de altria, ¿se supone que me darían 80 de PM o no es así?

Lo del dividendo eso ya no sé ni como cogerlo… ¿Se mantendría el dividendo que da PM o qué?

4 Me gusta