Los beneficio neto cae pero las ventas suben (los he visto muy por encima). Es una grandisima empresa y que segun mis criterios ha estado a punto de salir, puedo permitir un corte del dividendo máximo del 50%. Entiendo que en este caso está justificado por la propia deuda, no tiene sentido mantener el dividendo y aumentarlo con esa deuda. A largo casi que prefiero que se quite la deuda, ahora hay que ver como evoluciona y ver posible precio de ampliación el futuro.

A Altria no le hara mucha gracia ese recorte de dividendo

Exactamente, no recuerdo que % tenía aquí pero creo que rondaba el 10%. Hablo de memoria, precisamente presenta resultados hoy y le tengo una orden puesta.

50% de recorte y 30% de retención de dividendos. Sayonara baby!!!

Entre esto y lo de WPP hay días en que es mejor no levantarse de la cama ?

Yo empecé posición hace unos meses en 78 euros y estoy tentado de hacer otra compra ahora.

Que bajen ahora el dividendo, o incluso lo eliminen, desde mi punto de vista, es una buena decisión, lo primero que hay que hacer es bajar deuda, absorber la compra de Sab Miller y cuando vuelva a tener un balance saneado vuelta al dividendo

De aquellos barros, estos lodos. Esto es lo que pasa por pagar demasiado por una adquisición. Además los resultados del último trimestre son desastrosos. Veremos si T, VOD o GSK no siguen el mismo camino en breve…

Anheuser-Busch InBev (NYSE:BUD) is down 9.6% in premarket trading after the company reduces its dividend by 50%.

The company is looking to steady its balance sheet after the monster deal to buy SABMiller in 2016 piled on debt.

Q3 Non-GAAP EPS of $0.82 misses by $0.24; GAAP EPS of $0.48 misses by $0.28.

Que soléis hacer en estos casos: vendéis siempre o esperáis?

Te respondo lo que hago yo: ver si ese capital te rentará más de manera sostenible con otra inversión, si es así, liquidas e inviertes en el otro sitio. Con la cabeza fría

Yo voy a ver que hace en los próximos días para comprar un paquete.

Sin ser ningún experto, es una empresa de un sector que me gusta, a priori no tiene grandes peligros de disrupción, dentro de 100 años se seguirá bebiendo cerveza, para mi tiene ventajas competitivas de imagen de marca y red de distribución que son difíciles de replicar y hace falta mucho dinero para ello, que está pasando por un mal momento por la adquisición de su mayor competidor.

Esta y diageo son mis posiciones en cartera de bebidas alcohólicas. Ahora Diageo está en máximos históricos y bastante más cara, por lo que esta caida para mi representa una oportunidad para ampliar posición aquí.

Como he dicho antes, a mi lo que más me ha gustado ha sido la decisión de bajar el dividendo… también es cierto que actualmente no necesito el dividendo para vivir, por lo que yo voy a muy largo plazo…

Que soléis hacer en estos casos: vendéis siempre o esperáis?

Como ves cada uno tenemos nuestra propia visión sobre el futuro de BUD. Los últimos resultados parecen indicar que está perdiendo cuota de mercado (pese a la adquisición de SAB Miller) y que la competencia de las cervezas artesanales es cada vez mayor. De hecho no hay más que entrar en cualquier bar para darse cuenta de la ingente cantidad de cervezas a las que tiene acceso cualquier cliente, algo impensable hace escasamente una década. No me hubiese importado quedarme con las acciones y esperar a que el equipo directivo tomase las medidas necesarias para invertir esa tendencia siempre y cuando la RPD se hubiese mantenido por encima del 4%. Pero con un 2% escasito prefiero asumir las pérdidas y poner a trabajar ese dinero en valores que ahora mismo considero más interesantes y con dividendos más jugosos.

Yo haré lo mismo que tú Luke Skydividend. Mantendré con pérdidas latentes y esperaré a que poco vaya recuperando el dividendo. Es posible que tarde todavía algún tiempo ya que el endeudamiento que tiene es monstruoso.

Respecto a la empresa yo sigo siendo optimista para el largo plazo. Dudo mucho que el consumo de cerveza no siga creciendo, especialmente en los países emergentes, durante las próximas décadas y siendo líder del mercado debería poder sacar partido de esta situación

Yo me inclino a pensar que quizá ya bajó todo lo que tenía que bajar.

De hecho hoy estuve tentado de comprar! porque rompió su resistencia del canal bajista. Veo mucha fuerza en el gráfico.

Si se vuelve a meter en el canal bajista (lo dudo), le haría un seguimiento intensivo para comprar si toca el soporte del canal

19 July 2019 – Anheuser-Busch InBev (Euronext: ABI) (NYSE: BUD) (MEXBOL: ANB) (JSE: ANH) has agreed to divest Carlton & United Breweries (CUB), its Australian subsidiary, to Asahi Group Holdings, Ltd. for 16.0 billion AUD, equivalent to approximately 11.3 billion USD, in enterprise value. The transaction represents an implied multiple of 14.9x 2018 normalized EBITDA. As part of this transaction, AB InBev will grant Asahi Group Holdings, Ltd. rights to commercialize the portfolio of AB InBev’s global and international brands in Australia.

The divestiture of CUB, once completed, will help AB InBev to accelerate its expansion into other fast-growing markets in the APAC region and globally. It will also allow the company to create additional shareholder value by optimizing its business at an attractive price while further deleveraging its balance sheet and strengthening its position for growth opportunities.

In addition, AB InBev continues to believe in the strategic rationale of a potential offering of a minority

stake of Budweiser Brewing Company APAC Limited (Budweiser APAC), excluding Australia, provided that it can be completed at the right valuation.

Substantially all of the proceeds from the divestiture of the Australian business will be used by the company to pay down debt. AB InBev’s commitment to reach a net debt to EBITDA target ratio of below 4x by the end of 2020 is not dependent on the completion of this transaction.

Anheuser-Busch InBev reports Second Quarter and Half Year 2019 Results (25/07/2019)

Highlights:

Best quarterly volume performance in over five years with total growth of 2.1%, driven by strong

performances in many of our key markets including Mexico, Brazil, Europe, South Africa, Nigeria,

Australia and Colombia

Top-line growth of 6.2% and EBITDA growth of 9.4% with margin expansion of 123 bps to 42.0%

Continued success of our premiumization strategy supporting top and bottom line growth with global brand revenue growth of 8.0% (11.3% outside of the brands’ home markets) and High End Company revenue growth of nearly 20%

Committed to a Better World – We are halfway to reaching our goal of securing 100% of our purchased electricity from renewable sources by 2025

Key figures:

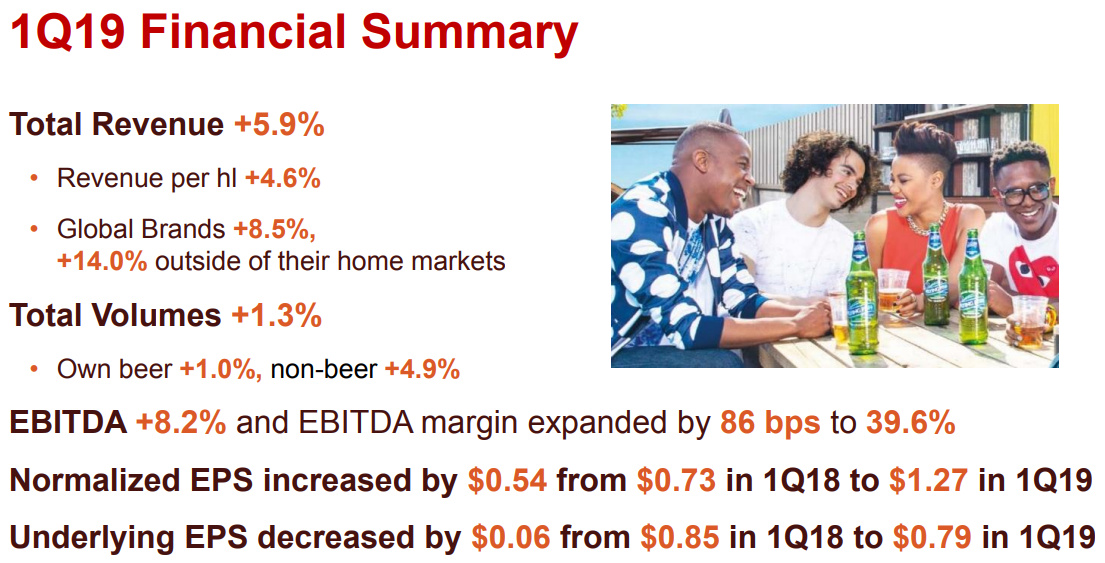

Revenue: Revenue grew by 6.2% in the quarter, with revenue per hl growth of 3.8%, driven by healthy volume growth, global premiumization and revenue management initiatives. In HY19, revenue grew by 6.0%, with revenue per hl growth of 4.2%.

Volume: Total volumes grew by 2.1% in 2Q19, with own beer volumes up 2.2% and non-beer volumes up 1.8%. In HY19, total volumes grew by 1.7%, with own beer volumes up 1.7% and non-beer volumes up 3.4%.

Global Brands: Combined revenues of our three global brands, Budweiser, Stella Artois and Corona, grew by 8.0% globally, and by 11.3% outside of their respective home markets. In HY19, the combined revenues of our global brands grew by 8.2% globally and by 12.4% outside of their home markets.

Cost of Sales (CoS): CoS increased by 7.2% in 2Q19 and by 4.4% on a per hl basis. In HY19, CoS increased by 6.6% and by 4.5% on a per hl basis.

EBITDA: EBITDA grew by 9.4% in the quarter, with EBITDA margin expansion of 123 bps to 42.0%, as a result of top-line growth and enhanced by premiumization and ongoing cost discipline. In HY19, EBITDA grew by 8.8% and EBITDA margin expanded by 104 bps to 40.9%.

Net finance results: Net finance costs (excluding non-recurring net finance results) were 1 004 million USD in 2Q19 compared to 1 301 million USD in 2Q18. The improvement was primarily due to a markto-market gain of 173 million USD in 2Q19 linked to the hedging of our share-based payment programs, compared to a loss of 16 million USD in 2Q18, resulting in a swing of 189 million USD. Net finance costs were 1 365 million USD in HY19 as compared to 2 878 million USD in HY18.

Income taxes: Normalized effective tax rate (ETR) increased from 24.7% in 2Q18 to 25.9% in 2Q19. Excluding the impact of gains relating to the hedging of our share-based payment programs, our normalized ETR was 27.2% in 2Q19 as compared to 24.6% in 2Q18. Normalized ETR decreased from 26.1% in HY18 to 23.1% in HY19 and, excluding the impact of gains relating to the hedging of our share-based payment programs, our normalized ETR increased from 25.0% in HY18 to 27.4% in HY19.

Profit: Normalized profit attributable to equity holders of AB InBev was 2 470 million USD in 2Q19

versus 2 159 million USD in 2Q18 and was 4 986 million USD in HY19 versus 3 602 million USD in HY18. Underlying profit (normalized profit attributable to equity holders of AB InBev excluding mark-tomarket gains linked to the hedging of our share-based payment programs and the impact of hyperinflation) was 2 295 million USD in 2Q19 as compared to 2 175 million USD in 2Q18 and was 3 866 million USD in HY19 as compared to 3 860 million USD in HY18.

2019 outlook

Overall Performance: In FY19, we continue to expect to deliver strong revenue and EBITDA

growth, driven by the solid performance of our brand portfolio and strong commercial plans. Our

growth model is even more focused on category expansion, targeting a more balanced top-line

growth between volume and revenue per hl. We expect to deliver revenue per hl growth ahead of

inflation based on premiumization and revenue management initiatives, while keeping costs (sum

of CoS plus SG&A) below inflation.

Cost of Sales: We continue to expect CoS per hl to increase by mid-single digits, with currency

and commodity headwinds to be offset by cost management initiatives.

Synergies: We maintain our 3.2 billion USD synergy and cost savings expectation on a constant

currency basis as of August 2016. From this total, 547 million USD was reported by former SAB

as of 31 March 2016, and 2 604 million USD was captured between 1 April 2016 and 30 June 2019. The balance of roughly 50 million USD is expected to be captured by the end of 2019.

Net Finance Costs: We expect the average gross debt coupon in FY19 to be between 3.75-

4.00%. Net pension interest expenses and accretion expenses including IFRS 16 adjustments

(lease reporting) are expected to be approximately 160 million USD per quarter. Net finance costs

will continue to be impacted by any gains and losses related to the hedging of our share-based

payment programs.

Effective Tax Rate (ETR): We expect the normalized ETR in FY19 to be in the range of 25% to

27%, excluding any gains and losses relating to the hedging of our share-based payment

programs.

Net Capital Expenditure: We expect net capital expenditure of between 4.0 and 4.5 billion USD

in FY19.

Debt: Approximately 40% of our gross debt is denominated in currencies other than the US dollar,

principally the Euro. Our optimal capital structure remains a net debt to EBITDA ratio of around

2x. We expect our net debt to EBITDA ratio to be below 4x by the end of 2020.

Dividends: We expect dividends to be a growing flow over time, although growth in the short term

is expected to be modest given our deleveraging commitments.