Encontrado:

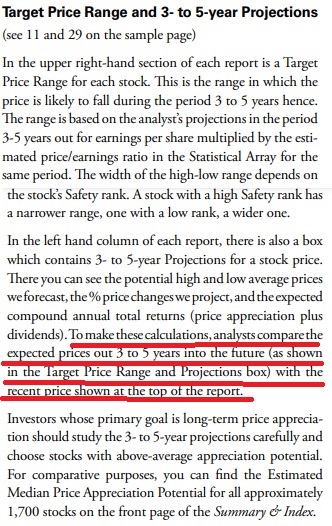

Pero sigo diciendo lo mismo, si el low son 200$ y el precio considerado es el recent price (172,27$) eso es una diferencia del 16,09% no del 15%

Encontrado:

Pero sigo diciendo lo mismo, si el low son 200$ y el precio considerado es el recent price (172,27$) eso es una diferencia del 16,09% no del 15%

Acerca de la inclusión de VZ en la cartera de alguien, en función de los objetivos.

"I can only speak for myself.

I think these discussions don’t look at the big picture, we seem to isolate and nit-pick an item or two when in reality it takes a number of pieces to come together to build a desirable portfolio.

I also have to deal with my own insecurities and fears. Having been through three recessions and a number of corrections, I’ve experienced the damage that can be done with portfolio values. In fact, there was a discussion on that earlier today about the fear of losing 20-30% of one’s portfolio value. A week or two ago we were discussing drawdowns and what we might do during the next market correction.

Well, in dealing with drawdowns, it is a known fact that many more growth companies lose their market value than do value companies during recessions. Part of the reason for that is that growth companies are priced in at higher performance expectations and when those expectations aren’t realized, the price takes a steeper cut.

Owning recession beaters is part of building a portfolio, and in some cases that requires owning high yield, low growth companies. One of the criteria I look to use to help minimize the drawdown is to keep the portfolio beta at a low number. The lower the number under 1.0, the less price volatility the portfolio is supposed to have.

When it comes to capital gain growth, I don’t know how to generate that. I’m at the mercy of the market. If I have certain expectations and those expectations haven’t been realized when the time has come, I don’t get to take a mulligan and get a do over.

I can control to a certain point the types of assets and companies I buy, my portfolio yield, my portfolio dividend growth, and my portfolio beta to meet certain expectations and be able to insure that at least those goals are met. As to price growth, I have to pray to the stock gods that it will follow in time. I can’t take credit for that.

Now when I look at all of that criteria and put the pieces together, then I may very well have a place for a company like VZ or T for that matter. They serve a certain function. To what degree they serve is up to the portfolio owner and the goals they establish for themselves.

VZ or T for that matter may not have a place in your portfolio but that doesn’t mean they don’t have a place in the portfolio of others. It’s not my place to tell them their goals are wrong. If I can share an idea or two in how to utilize those assets to help them meet their goal I’ll do that, but I rarely tell someone to sell something and replace it with another. I simply ask them if it is doing what it is they expected it to do and if not, they have a decision to make, not me.

From my perspective it’s not important that I understand what others are doing or not, I try to focus in on whether what they say relates to me or not and if the answer is yes, I’ll go to work making a plan to utilize the concept or idea they speak of.

As I have said many times, what I do may not be for everyone and what I sell in one portfolio, I may be buying in another. It all comes down to personal goals and expectations, and if those expectations are far more than is needed, who are we to question those motives. It’s not our portfolios."

@luisg parece que estoy leyendo a un forero ilustre.

Young Folk Portfolio … Portfolio Adjustments (20 de septiembre)

I made quite a few moves today to help the portfolio raise its dividend safety rating, increase its dividend growth, and provide more diversification moving forward.

Today I sold all shares in ARKK, ARKW and ETHE. I trimmed $2K each from MKC and TSLA.

(22 septiemrbe) Today I replaced ARKX with UNH.

I have a Legacy Portfolio set aside, one that I don’t report on publicly, that is full of the disruptive innovation companies so it didn’t make sense to hold the above position in both accounts."

Pues nada, poco a poco volvemos a la normalidad.

Vende las empresas disruptoras y dice cosas preciosas…

La verdad es que no se como se pudo dejar deslumbrar por los cantos de sirena de Cathie, Chamath y todo el high growth. Al final supongo que es el problema de los objetivos, que si los superas te vas a poner a hacer experimentos con gaseosa y hacer historias raras.

La ventaja que tiene Chowder es que se puede permitir patinazos gordos porque va sobrado.

¿le ha dado puerta también a las criptomonedas?

Sí, con la mili que tiene hecha parece mentira que se haya dejado engatusar por estos vendeburras. Ojo, que en una cartera para muchísimos años puede tener algo de sentido llevar algo de esto. Pero no entrando a los precios que cotizaban.

Se aburriría el hombre de poner vagones en círculo y decidió meterse en territorio Comanche con el Winchester en busca de El Dorado y algo de emoción.

Yo veo lo positivo, el tipo se ha ido por el camino equivocado, pero como ha publicado todo lo que hace, alguien le habrá dicho: “pero dónde vas??”

Y eso, le ha salvado,

Bueno, Chowder aún no ha escapado de los CEFs, que va incrementando poco a poco en su Older Folk Portfolio. Yo espero estar mucho tiempo en ese barco. Te puedes subir a él, pero no cargues todos los millones de golpe que hay poco volumen y se nos distorsiona la cosa

Un clásico de Chowder.

"I have found in the past that when I had trouble making decisions it was because I lacked a clearly defined plan. I was listening to too many people, trying too many things.

I found that when I set a clearly defined goal as to what it was I wanted to achieve, the decisions were easy to make, there wasn’t any hesitation, no regrets and I simply trusted my research and stuck with the plan."

Respecto a la cartera de su hijo, como dice @kapandji, ha vendido casi todo los disrruptivo, excepto TSLA.

Abora centrado en dividendos y growth (en young folk portfolio).

Pero OJO, mantiene una cartera que será legado para sus hijos donde sigue con esas posiciones y criptos.

Varias de las vendidas estaban en rentabilidad negativa de 1 dígito y quizá haya ganado con otras (se supone iba comprando desde verano). Supongo le ha salido cuenta con paga.

"TOP 10 HOLDINGS –

Young Folk Portfolio — Company … % of Portfolio

TGT – 3.6%

MCD – 3.6%

TSLA – 3.5%

LMT – 3.4%

ADP – 3.3%

HD – 2.9%

JNJ – 2.9%

ABT – 2.6%

PEP – 2.6%

DG – 2.6%

Looking for a balance between growth and income.

Middle Age Portfolio

O – 7.5%

DUK – 7.1%

ABBV – 5.0%

KO – 4.2%

ADP – 4.0%

PG – 3.8%

NEE – 3.8%

SO – 3.5%

JNJ – 3.3%

DNP – 2.9% (cef)

Need immediate aggressive income growth, thus higher % of portfolio for higher yielding assets."

Interesante esta cartera modelo de Chowder buscando un Yield > 3% con un crecimiento orgánico del dividendo superior al 10%. Al final ahí esta el sweet spot de la estrategia:

https://seekingalpha.com/instablog/728729-chowder/5659112-dividend-growth-model#comments

Tiene buena pinta pero seguro que tampoco bate al mercado

La dictadura del SP500 es peor que la de Pol Pot

Si alguien tiene como objetivo en su vida batir al SP500…lo mejor es que se compre el SP500.

No conocía mucho LYB (LyonDellBasell) y SNA (Snap-On). LYB por lo que veo es como una BASF pero más shareholder friendly, con buenas recompras y mejor crecimiento del dividendo. Un nuevo beat de USA a Europa en una empresa similar, por eso será que el SP500 es imbatible. Y SNA otra industrial que parece un martillo pilón con crecimiento del divi de doble dígito.

Otro “kamikaze” que batió el S&P500

Una cartera interesante para protegerte de la inflación.

Llevo 10 empresas de las que presenta.

Mucho peso al industrial y poco al consumer staples para mi gusto.

Ah! y servicios públicos también demasiado cargado.

Eso comenta en algún comentario, que buscando un crecimiento orgánico > 10% no puedes basar tu cartera en Consumer Staples porque ya no hay ninguna que vaya a conseguir esos crecimientos, sumado a que andan alrededor de máximos la gran mayoría con yields inferiores al 3% en varios casos como PEP, PG o KO. Con lo cual no pueden hacer palanca ni en yield ni en crecimiento.

Pero, ¿eso no es muy parecido al famoso número de Chowder? para mi conceptualmente es casi igual.

En este modelo se espapa decir que está convencido que la inflación subirá, sino no se entiende que solo haya 8% de tecnología y 20% de industriales.