De SeeksQuality, que hoy ha aumentado su posición en CVS (a 62,7$).

"anybody thinking of buying or selling CVS on this earnings report really needs to read through the full conference call (transcript on SA) and slide deck.

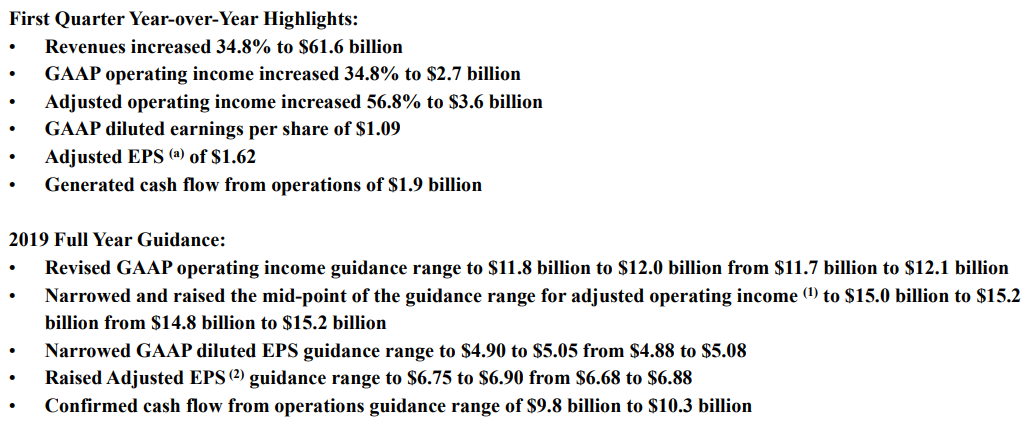

What strikes me is how many initiatives are in progress! From the first few pages of the slide deck:

- Continued rollout of MinuteClinic, claiming 80% of primary care services now available there.

- New concept stores unveiled this month, the next-gen MinuteClinic.

- Home visits by Coram for infusion services, up 15%.

They are up front about the challenges – price pressure on pharmacy, questions surrounding PBM rebates, and LTC weakness. But they also have what I believe are solid initiatives in place to address them.

- A new PBM contracting model, guaranteeing client cost and passing on all rebates to the customer. They aim to prove that they can generate customer value without any shady dealing. (Can the other PBM’s do the same? CVS/Caremark is one of the stronger ones.)

- Cost controls in the LTC segment. This is necessary, if poorly defined. If the division is losing money, then work to prune it back until it becomes profitable again.

- Synergy with Aetna. Delayed by the slow approval process and delayed further by the consent agreement with the judge, but I believe that runs just six months (and the clock is already ticking). Once they receive final approval, they may be able to more fully exploit the verticals.

- Product differentiation for Aetna, through the consumer-facing segments of CVS.

- Technological partnerships, such as Attain by Aetna (Apple Watch) recently announced.

- New health care offerings in place for 2021 selling season. You can bet these will be unique to CVS/Aetna, as there is no other company that spans so many verticals in healthcare. (United Health is another integrated offering, but lacks the consumer front.)

Now maybe I’m living in a cave, and everybody else is already doing these things? Maybe CVS is chasing the competition (like IBM in the cloud?) and merely trying to rehash the same old stuff with new window dressing? Or maybe this is an entirely new model for health-care delivery that will add a low-cost easy-access service tier to what is already in place?

My belief is that much of this is truly innovative, and will drive revenues over the next three years. The most novel stuff isn’t really ready for 2019, but pieces of the program will gain traction by 2020 and I expect everything announced to be launched by 2021. By 2022 we should be seeing full benefit from these initiatives – though I would expect continuing growth beyond that.

The risk is that these bomb, stifled by regulators, poor consumer buy-in, etc. You can point to the Omnicare acquisition that they overpaid for as an example that management isn’t perfect. What company is? Apple, Amazon, Google, Microsoft… Have none of them ever seen a project or acquisition bomb? Acquisitions are risky, because you are always betting that you can generate more profit from the business than the current operators.

So why is there any reason to believe that CVS/Aetna will be able to generate greater profit than CVS and Aetna as stand-alone? Look to the slide deck and see if that answers your questions."

"The debt is definitely huge! The combined company has $138B of liabilities, up $80B from last year. Assets are up $100B, but about $65B of that is Goodwill and Intangibles. Insurance operations carry both Assets and Liabilities, so the large increase in numbers is to be expected, but we are still looking at a heck of a lot of net debt.

Looking at the debt maturities, I would guesstimate that half their operating cash flow over the next three years will go towards retiring debt. That is huge, but not unsustainable given their moderate dividend. The deal was financed with 3, 5, 10, 20, and 30 year borrowing, but on top of the other debts it seems likely that the 2021 maturities are the major hump. If they can get past that successfully, without the need for an equity raise, then they will be in great shape going forward.

This article focuses on the debt, with a skeptical tone:

realmoney.thestreet.com/…

They quote 4.6x Debt/EBITDA, which sounds about right to me. They need to clear about 20% of that debt to retreat from “scary” levels and 30%+ to get back to healthy levels, HOWEVER an increase in EBITDA would contribute to clearing the excess. They presently have a bit over $70B in debt, so clearing $15B (along with a 10%-15% increase in EBITDA) might get the job done.

In short, they need to pay down those 2019, 2020, and 2021 maturities as/before they come due. Not much due this year. The 2020 maturities should be easy enough to clear. And that 2021 bill of $10B? If they haven’t gotten started on that by 2020, it will be a tough bill to handle – they would need to roll it out further in that case. On the other hand, there is every reason to expect that they can manage the whole $15B+ if they spread it out evenly over 2019-2021. We are looking at $10B+ OCF and $7B+ FCF. Their dividend run rate is around $2.5B. They can’t afford share buybacks or further acquisitions (!), and they can’t afford a meaningful dividend increase, but they ought to be able to maintain the dividend and repair the debt by the end of 2021."

"Right now we are looking at a price of ~9x forward earnings, with growth expectations of 9%-10% going ahead from here. A company with that kind of growth will typically trade at 15x-20x earnings, even with a substantial risk premium baked in. Thus if CVS can execute over the next two to three years, I expect a P/E expansion of 50%+ in addition to fundamentals growth of 9%-10% and an ongoing yield of 3%.

If management can hit expectations, you could be looking at a 25% annualized total return over the next three years. There are real risks involved, but the valuation cannot be ignored. It is a similar P/E to AT&T, which is facing its own debt/integration risk and would be thrilled with 5% fundamental growth (a more realistic estimate is 2%). It is substantially cheaper than IBM which is facing its own major debt/integration risk and is a year behind in the assimilation process, and again which is looking at 2%-5% growth. It is 20% cheaper than WBA which has the same Moodys debt rating and fewer growth avenues going forward. It is 30% cheaper than GIS, another debt/growth/turnaround candidate hoping for 5% growth.

I know dividend investors will point to the yield and the dividend freeze as evidence that T, IBM, and GIS are much better values, however in my opinion you are buying the COMPANY and the CASH FLOW rather than the DIVIDEND. And right now CVS is comparable/cheaper than those three, with superior fundamental growth prospects.

Think about it – the three year plan has them spending $2.5B annually on the dividend and $5B annually on retiring debt. By the end of three years (if not a year earlier due to EBITDA growth) the need for aggressive debt retirement will be past. They could easily choose to double the dividend payment at that time. More likely, they would aim for a 30% payout ratio (which in recent years they have indicated as a target) and a $3/share dividend, a 50% increase from the current level.

That won’t happen this year. That won’t happen next year. If they were to announce a large dividend increase this year or next, I would immediately sell. That would be a STUPID decision for management, when they need to first fix the debt. But once the Debt/EBITDA is down to the low 3’s, you can expect large increases again with a “catchup” increase covering the last 2-3 years. I do not believe they intend to permanently limit the payout."