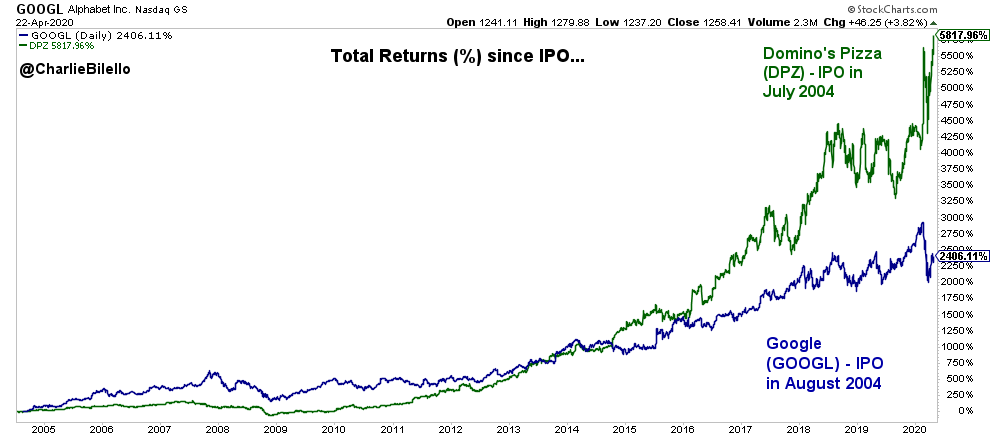

He encontrado un tweet muy curioso sobre esta empresa. ¿Alguien la sigue?

https://twitter.com/charliebilello/status/1129482088955207681

He encontrado un tweet muy curioso sobre esta empresa. ¿Alguien la sigue?

https://twitter.com/charliebilello/status/1129482088955207681

El gran “error” de Terry Smith. Las vendio en 2016 a 105$ dolares por accion porque las veia caras. Hoy cotizan a 280$. “Solo” gano un 600%.

Pues que hace 10 años fue una excelente oportunidad de inversión. Desde entonces ha multiplicado por 60, dividendos aparte.

Creo que llegamos tarde (como con Monster´s) y no sabría decirte si es mejor esta o la que cotiza en UK.

Con esta siempre anda el rumor de que podría ser la siguiente adquisición de Restaurant Brands (QSR).

Si algo me han enseñado los palos de la bolsa es que SIEMPRE la MATRIZ y NUNCA la FILIAL ![]()

¿Por que siempre sube mas de lo que menos llevo?

Madre mia. Las pizzas son los nuevos Teslas

Al final subio un 25,60%

Mercado de locos

¿Y al final la cosa por qué viene? ¿Han batido todos los records mundiales de venta de pizzas, margenes y beneficios? ¿Se les ha ido la pinza y lo han trasladado al dividendo?

Un saludo.

Parece que lo han petado el último trimestre

La gente ya solo come pizza

Sera el unico restaurante que sigue subiendo beneficios

With wide-moat Domino’s disclosing strong intra-quarter sales (including quarter-to-date U.S. comps of 14.0%), the key question heading into its second-quarter update was whether the company could maintain its momentum as dine-in focused rivals have started to reopen. The company answered this emphatically, with U.S. second-quarter comps of 16.1% implying accelerating sales trends as the quarter progressed. We believe this acceleration underscores that consumers continue view Domino’s value, digital ordering, and safety protocols (including contactless delivery options) in a more favorable light relative to other operators.

Looking ahead, Domino’s is operating from a position of strength. We believe its value proposition will become even more important, in the words of CEO Ritch Allison, “when we’re facing a recession and high unemployment.” Domino’s also appears to be prioritizing innovation more than it has in the past, including last week’s revamped chicken wing platform launch and other menu additions planned for the back half of the year. These factors should keep comps well ahead of industry averages, and we plan to raise our full-year U.S. comp outlook from the high-single-digits to the low-double-digits. We also see opportunities to accelerate its fortressing strategy (increasing store density by splitting franchisee territories) due to strong franchisee health and an increase in the amount suitable real estate availability due to other retail/restaurant closures. As such, we believe Domino’s can post 10% average annual revenue growth the next 10 years.

We’re planning to raise our $355 fair value estimate by a mid-single-digit percentage to reflect a more optimistic revenue outlook but believe the market has effectively priced in this long-term growth. While we don’t see a ton of downside catalysts as macro and industry forces make Domino’s top-of-mind for consumers, we’d prefer a greater margin of safety at current levels.

Domino’s fourth-quarter U.S. comps of 11.2% fell slightly short of our 12.2% expectation, but we still believe the firm is well-positioned for growth. Store openings picked up at the end of the year, closing out the fourth quarter with 388 total net new units (far surpassing our expectation of 43 net new units for the quarter). These additional openings were driven by strong growth in domestic and international markets (with 103 and 242 more than expected, respectively). Lower supply chain costs lifted the firm’s fourth-quarter operating margins up 26 basis points (to 18.0%) compared with last year. As the firm continues to leverage costs and run a more efficient supply chain, we anticipate operating margins will reach just over 20% by 2029.

Along with earnings, the firm provided a new two- to three-year outlook that calls for global retail sales growth of 6%-10% and global net unit growth of 6%-8%. Even though this outlook is lower than the three- to five-year guidance provided in early 2019 (global retail sales growth of 8%-12% and net unit growth of 6%-8%), these updated targets align with our expectations for three-year average annual revenue and global net unit growth of just under 9% and 7.5%, respectively. When taken together, the higher unit base next year should warrant a small increase to our fair value estimate of $386. With shares down high-single digits on the news, we view the stock as modestly undervalued at current levels.

While uncertainty persists, we are encouraged that Domino’s plans to continue increasing investments in its technology (particularly as it relates to its digital order platforms and GPS tracking), key components underpinning our wide-moat rating and factors that have aided its performance since the pandemic took hold. Additionally, the firm is planning to make investments in operational technologies that are slated to improve speed and efficiencies in the kitchen, which we think should help it withstand competitive intensity.

Otra que aparece en el radar.

Para tener un SSD=55 los veo espléndidos con los incrementos de dividendos.

Debe ser propio de mi inexperiencia. Pero, no es curioso que aumente el dividendo un 20% y la accion caiga un 7%??

Wide-moat Domino’s posted impressive first-quarter results, with midteens system sales growth (15% in the U.S. and 18% abroad) driving a modest earnings beat. While the market response was initially tepid, we believe that April 29’s subsequent rally (up about 2%) more accurately reflects the firm’s underlying strength, with strong net unit openings, volume retention in markets where dine-in restrictions have softened, and stable service times (despite labor market tightness) representing a pleasant surprise for investors. Though we plan to raise our fair value estimate to $350 per share from $340, we believe the shares look rich, trading at roughly an 18% premium to our updated valuation.

Underperformance by Domino’s company-owned stores (6% comparable-store sales growth against 14% for domestic franchisees) was surprising, but appears to be attributable to a heavily urban footprint, posing interesting questions about the firm’s target markets moving forward. While daytime population should normalize somewhat in larger cities, we wouldn’t be surprised to see new openings concentrated in larger suburbs, a strategy adopted by some limited-service peers, bringing the firm closer to customers as the prevalence of working from home may slow (or reverse) urban migration.

Though delivery volume is likely to moderate in the back half of the year, we continue to expect low-single-digit U.S. comparable-store sales growth (3.6%) through 2021 as carryout volume and a return to conventional promotional activity offset a mix shift toward full-service dining. Carryout growth in 2020 clocked in below its prepandemic run rate, implying that the firm lost some market share, given the reliance of many full-service pizza restaurants on the channel and commensurately outsize growth. However, we view Domino’s current strategies (carside carryout, fortressing, and a frictionless digital interface) as likely to drive sustained share gains in the space moving forward.