Cotiza en Amsterdam y ahora es parte del AEX 25. Me llama la atención la cotización, como se ha comportado el valor a lo largo de los años y que es un holding controlado por varias familias. Paga un dividendo muy pequeño con crecimiento tmb algo lento… No pude ver bien el tema de la recompra de acciones.

Me ha parecido muy difícil encontrar info o análisis de esta empresa. Alguien la sigue? Creo que cotizaba en Milan anteriormente.

Creo que es dueña de Stellantis, Ferrari, Iveco, CNH Industrial, la Juventus, el periódico The Economist y otras cosas mas. Quien me puede ayudar a entender mas?

It is cheap. It is trading at a 47% discount to its NAV, close to the historical record.

Such a discount comes from a few misconceptions about the stock, not because of serious issues with the underlying businesses or their management.

Strong capital allocation. Exor has been extracting value from its old legacy assets and redirecting more capital to fast-growing businesses. It follows a clear, value-focused investment philosophy. Exor has grown its NAV by 19.8% since 2009, and I expect this rate to be maintained in the mid-term.

Entro con una rubicompra sobre los 75 EUR. He tomado 10 acciones en HeyTrade.

La diferencia del NAV to asset value que da un descuento de mas del 30% y las recompras diarias + el dividendo me seguridad de que el equipo ejecutivo esta intentando achicar este spread. Ahora que cotiza como parte del indice AEX me da mas convicción todavía.

Net cash position up €4.7 billion, at €0.8 billion at year-end

NAV at year end at €28.2 billion. NAV per share declined 7.6%, while outperforming the MSCI World Index by 6.6 p.p., mainly driven by the market performance of listed companies and cash position

Board of Directors nominates for AGM appointment Nitin Nohria as new Chairman, Senior Non- Executive Director and Sandra Dembeck and Tiberto Ruy Brandolini D’Adda as new Non-Executive

Directors

Board of Directors approved today final €150 million tranche of the €500 million share buyback

program

Ordinary dividend of €100 million corresponds to €0.44 per share to be paid, subject to AGM

approval

Nada mal, al comprar Philips pasaran de recibir EUR 850MM a EUR 1098MM en el 2024. Lindo incremento.

Calculo que seguirán pagando sobre los 100MM de divis, pero harán recompras para recortar el descuento con el NAV. Tmb dijeron que seguiran haciendo tender offers, pq les ha resultado muy eficiente ya que no es un titulo con grandes volumenes.

La parte de “Investments” que es mas del 7% de la torta a 2024, lo compone en un 85% Lingotto.

Lingotto es una gestora de fondos privada. Ya existia antes como Exor funds o algo asi. Se inicio para gestionar los activos de PartnerRe, la aseguradora que compro Exor y vendio luevo a Covea. Esta ultima mantiene los fondos alli, Exor agrega inversiones y ahora buscan expandir la gestion de capitales con dinero de 3eros y montar toda una gestora nueva.

We are committed to delivering attractive long-term returns to our limited partners, protecting their capital from permanent losses while accepting concentration, illiquidity and volatility.

Se apuntaron a uno de los managers iniciales de Baillie Giffords:

Potential investments could include music royalties, insurance, structured equity and structured credit, along with various forms of real assets. The fund will focus on capital preservation and structured downside protection.

Por esto tmb me interese Royalty Pharma (RPRX), creo que hay un mercado de capital que no es muy eficiente. Ver Whitehaven (financiando la compra de los activos de BHP) y otras empresas “malas” y ver como tmb farmacéuticas tienen que salir a buscar pasta para financiar sus ciclos de I+D, pq el mercado no da mas de si.

The Exor 2024 annual report reveals a year of mixed results and provides important insights into the company’s holding structure, strategy, and financials, all crucial for retail investors. While strong performances from holdings like Ferrari drove growth, others like Stellantis and CNH navigated downturns. The report highlights Exor’s strategic focus on healthcare, luxury, and technology for future growth, alongside details on its Net Asset Value (NAV), free cash flow, and capital allocation.

Why it matters:

Portfolio Concentration & Strategy: Exor’s decision to sell a portion of its Ferrari stake signals a move to reduce portfolio concentration, potentially lowering risk. Its active approach to acquisitions and divestitures directly impacts shareholder value.

Healthcare Focus: Increased investment in Philips and bioMérieux demonstrates a strong conviction in the healthcare sector, offering potential long-term growth opportunities.

Stellantis Challenges: Difficulties faced by Stellantis, including leadership changes and market headwinds, highlight the cyclical nature of the automotive industry and associated risks.

NAV Discount: The report notes a persistent discount to Net Asset Value (NAV), which could represent either an opportunity or a risk. Understanding the reasons behind this discount is essential for investors.

Free Cash Flow & Shareholder Returns: Exor’s free cash flow generation, alongside its dividend payments and share buybacks, indicates its ability to reward shareholders and fund future investments.

Capital Allocation: Exor’s decisions on acquisitions, divestitures, and share buybacks directly impact shareholder value and the company’s future prospects.

The bottom line:

Exor’s overall investment thesis remains cautiously positive, backed by a diversified portfolio and a focus on high-growth sectors.

The shift towards reporting as an Investment Entity places greater emphasis on the fair value of investments when evaluating performance.

Investors should closely monitor the progress of Stellantis’s turnaround, the performance of healthcare investments, and the company’s success in deploying capital.

Exor’s active portfolio management and focus on shareholder returns (dividends, buybacks) are generally favorable for retail investors but can lead to significant gains or potential losses, requiring ongoing vigilance.

The company’s focus on maintaining a strong balance sheet and managing debt is reassuring for risk-averse investors.

Outlook / Long-Term View

Exor’s strategic direction, particularly its emphasis on healthcare and technology, suggests a focus on long-term growth and innovation. Strategic decisions, like the Ferrari stake sale and focus on new acquisitions, will significantly shape its future. While cyclical downturns pose near-term challenges, the company’s active management and capital allocation aim to maximize long-term shareholder value. Investors should monitor Exor’s ability to narrow the NAV discount while generating sustainable free cash flow. For a retail investor, Exor represents a diversified investment in global leaders but requires careful monitoring of individual company performance, sector-specific risks, and the effectiveness of its capital deployment strategy.

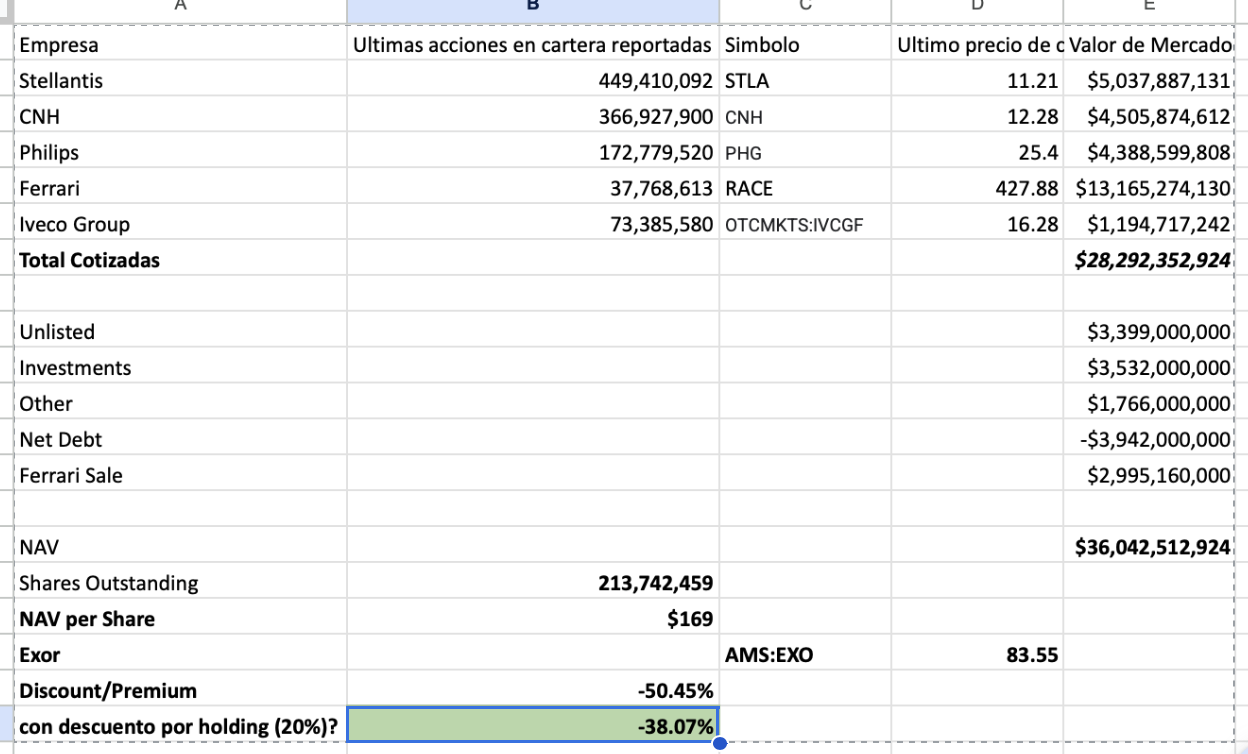

Recopilando datos de la nueva cartera a cierre del 2025. Me da que ya estaría en precio. Buscando ambos objetivos: descuento mayor al 45% y descuento mayor al 35% si ajusto (20%) por holding. Ahora se estarían cumpliendo ambos objetivos, reportando: 56% de descuento vs NAV y 46% de descuento vs NAV ajustado (-20%) con descuento por holding.

Por otro lado parece que se preparan para hacer otra inversión fuerte como hicieron con Philips.

23 de marzo (Reuters) - Exor (EXOR.AS), abre una nueva pestaña, espera recaudar 2 mil millones de euros (2.320 millones de dólares) en ingresos este año de la venta de sus participaciones en cuatro empresas, dijo el lunes la firma de inversión de la familia Agnelli.

La empresa ha firmado acuerdos de venta de acciones con el fabricante de camiones y autobuses Iveco Group (IVG.MI), abre una nueva pestaña, el grupo de medios GEDI, la empresa de atención médica Lifenet y el vehículo de inversión Nuo, y se espera que los ingresos superen 1,4 veces el capital invertido, dijo Exor.

Reciba un resumen diario de noticias comerciales de última hora directamente en su bandeja de entrada con el boletín de Reuters Business. Regístrate aquí.

Las ventas han permitido a Exor aumentar su efectivo disponible para el despliegue a más de 3.500 millones de euros, poniéndolo en condiciones de buscar una inversión “similar en escala y ambición a Philips”, dijo el CEO John Elkann en una carta a los accionistas.