En mi caso contrate el fondo para meter los ahorros de mis hijos por lo que no puedo hacer aportaciones periodicas, pero ahora que han juntado un dinerillo no se si meterlo directamente o esperar a ver si baja algo.

Tienes toda la razón. No se si cuando empecé con MyInvestor estaba con mínimo y que no me enteré.

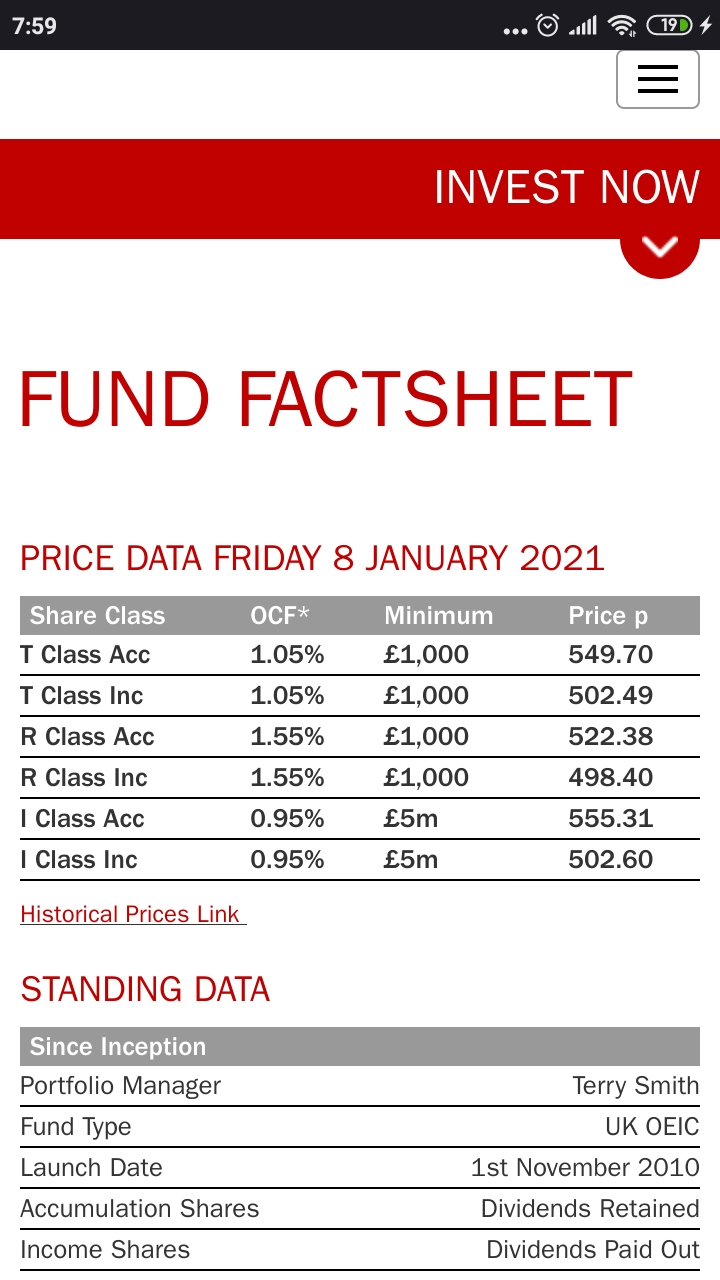

Lo curioso es que tienen la clase barata, la T, sin mínimo y la cara, la clase R, con mínimo de 1000€.

Como pensé que no podía invertir en Fundsmith comencé con Seilern World Growth, un fondo similar en la filosofía y en rentabilidades. De momento seguiré con Seilern

3 Me gusta

Pregunta de novato, al hilo de las clases, la R es más cara y tiene por lo tanto más gastos… pero a que se debe ese incremento de gastos?

Si es menos accesible debería de ser más barata no?

La clase normal es la R que creo que significa Retail. La T significa Terry y es la que tiene él.

Que sea más o menos accesible en Myinvestor y otro comercializador no significa que sea así en todos lados.

Por ejemplo en UK casi todo el mundo tiene acceso a la clase I en sus brokers que es para institucionales y por tanto más barata. Yo la tengo en un SIPP de UK desde 2015 mientras que aquí está claro que me sería imposible acceder a ella.

2 Me gusta

Yo invierto en la SICAV que crearon en Luxemburgo. Gastos corrientes: 1.12%

Tienen otra alternativa un poco más económica pero no he visto que la oferte ningún broker nacional. Gastos corrientes: 0.97%

Y otra más cara. Gastos corrientes: 1.62%

2 Me gusta

En IronIA Fintech puedes acceder a la clase I, así como a clases limpias de muchas gestoras.

Un saludo

2 Me gusta

La T es la que tengo yo que está en Renta 4 disponible

LU0690375182

Fundsmith Equity Fund Sicav T EUR Acc

Un TER de 1,12%

Inversión mínima 2000€, sucesivas 1000€

Yo llevo la clase T en Openbank sin mínimo de aportación.

4 Me gusta

Terry estuvo de cervezas con Chowder

"You rarely get to purchase high quality businesses at cheap prices unless there is a ‘glitch’ which provides an opportunity to do so"

1 me gusta

Es parte del copia-pega que hay entre carta y carta ![]()

No se si lo metio hace tiempo para justificar la entrada en FB. La pildorita de esta carta es lo de los intangibles.

Tambien llama la atencion

But whilst Sir John Templeton did say that the four most dangerous words in investment are ‘This time it’s different’ (which is actually five words before anyone points this out) sometimes it really is different and if you miss such inflection points it is to the detriment of your net worth.

Esta me encanta:

We are not the sort of people who ever declare victory — we

invest with a strong sense of paranoia

Y esta otra habría que enmarcarla:

I lived through the rise and fall of the Japanese equity market. When

it reached its peak in 1989 with a PE of over 60 we were told that this

was because Japanese company accounting was much more

conservative than western companies. In fact, their shares were just

expensive.

y para terminar:

I will leave you with this thought: What are the similarities between a

forecaster and a one-eyed javelin thrower? Answer: Neither is likely

to be very accurate but they are typically good at keeping the attention

of the audience.

¿Entonces esta vez si que es diferente?

La cara de tontos que se les va a quedar a los que acaben en el lado equivocado de esa pregunta cada vez parece más grande desde luego. Lo que no sabemos es la respuesta

1 me gusta

This leads onto the question of valuation. The weighted average free cash flow (‘FCF’) yield (the free cash flow generated by the companies divided by their market value) of the portfolio at the outset of the year was 3.4% and ended it at 2.8%, so they became more highly rated as growth in the share prices has significantly outperformed growth of the free cash flows. Whilst this is a good thing from the viewpoint of the performance of their shares and the Fund, it makes us nervous as changes in valuation are finite and reversible, although it is hard to see the most likely source of such a reversal — a rise in interest rates — in the near future

O dicho de otra manera. Llevábamos una cartera muy buena y la veíamos cara de narices. Pues ahora seguimos con una cartera muy buena pero oiga usted, resulta que está aún más cara, quien lo iba a decir. Así que si en unos años o cuando sea vuelve a donde consideramos que es su precio justo, pues nos meteremos un buen tropezón. Avisados quedan nuestros apreciados navegantes

4 Me gusta

Resumen de cartas:

2011: The trailing free cash flow (“FCF”) yield at the start of the year was about 7% and about 5.8% at the end

2012: The weighted average free cash flow (“FCF”) yield, which is our primary valuation yardstick, of the companies in the portfolio started the year at about 5.8% and finished it at about 5.7%

2013: The weighted average FCF yield of the portfolio started the year at 5.7% and ended it at 5.1%

2014: The weighted average Free Cash Flow (‘FCF’) yield of the portfolio (the free cash flow generated by the companies divided by their market value) started the year at 5.1% and ended it at 4.5%

2015: The weighted average Free Cash Flow (‘FCF’) yield of the portfolio (the free cash flow generated by the companies divided by their market value) started the year at 4.5% and ended it at 4.3%

2016: The Free Cash Flow (“FCF”) yield (the free cash flow generated by the companies divided by their market value) on the portfolio at the outset of the year was 4.3% and ended it at 4.4%

2017: The weighted average free cash flow (‘FCF’) yield (the free cash flow generated by the companies divided by their market value) on the portfolio at the outset of the year was 4.4% and ended it at 3.7%

2018: The weighted average free cash flow (‘FCF’) yield (the free cash flow generated by the companies divided by their market value) of the portfolio at the outset of the year was 3.7% and ended it at 4.0%

2019: The weighted average free cash flow (‘FCF’) yield (the free cash flow generated by the companies divided by their market value) of the portfolio at the outset of the year was 4.0% and ended it at 3.4%

2020: The weighted average free cash flow (‘FCF’) yield (the free cash flow generated by the companies divided by their market value) of the portfolio at the outset of the year was 3.4% and ended it at 2.8%

11 Me gusta

Que locura, los retornos a esperar son la mitad. Bueno, supongo que si solo llevas tabaco y petróleo no

Posiciones 30/Sep/2020

| Nombre | Peso (%) | Fwd P/E | Sector |

|---|---|---|---|

| Microsoft Corp | 7.4 | 33.0 | Technology |

| PayPal Holdings Inc | 7.0 | 59.9 | Financial Services |

| Facebook Inc A | 4.9 | 23.8 | Communication Services |

| IDEXX Laboratories Inc | 4.7 | 66.2 | Healthcare |

| Novo Nordisk A/S B | 4.3 | 23.9 | Healthcare |

| Philip Morris International Inc | 4.2 | 14.8 | Consumer Defensive |

| Intuit Inc | 4.2 | 47.8 | Technology |

| The Estee Lauder Companies Inc Class A | 4.1 | 48.5 | Consumer Defensive |

| McCormick & Co Inc Non-Voting | 4.0 | 30.1 | Consumer Defensive |

| L’Oreal SA | 3.6 | 36.2 | Consumer Defensive |

| Stryker Corp | 3.6 | 26.0 | Healthcare |

| Visa Inc Class A | 3.5 | 38.8 | Financial Services |

| PepsiCo Inc | 3.5 | 23.1 | Consumer Defensive |

| KONE Oyj Class B | 3.4 | 31.8 | Industrials |

| Reckitt Benckiser Group PLC | 3.2 | 20.3 | Consumer Defensive |

| Becton, Dickinson and Co | 2.7 | 20.1 | Healthcare |

| Unilever PLC | 2.6 | 18.9 | Consumer Defensive |

| Coloplast A/S B | 2.5 | 44.1 | Healthcare |

| Amadeus IT Group SA A | 2.5 | 102.0 | Technology |

| Automatic Data Processing Inc | 2.5 | 31.2 | Industrials |

| Intertek Group PLC | 2.5 | 30.7 | Industrials |

| Nike Inc B | 2.4 | 36.4 | Consumer Cyclical |

| Johnson & Johnson | 2.4 | 17.1 | Healthcare |

| Waters Corp | 2.2 | 30.3 | Healthcare |

| Starbucks Corp | 2.2 | 35.7 | Consumer Cyclical |

| Brown-Forman Corp Class B | 2.1 | 39.2 | Consumer Defensive |

| Sage Group (The) PLC | 2.1 | 25.8 | Technology |

| Diageo PLC | 2.1 | 26.3 | Consumer Defensive |

| InterContinental Hotels Group PLC | 2.0 | 41.2 | Consumer Cyclical |

Creia que RB la habia rotado a principios de la pandemia

11 Me gusta

Anda lleva mas-menos las que llevo yo en mi fondo de inversion personal y no cobro el 1,25%. Menos mal que es de lo que menos cobra