Third quarter 2019 net sales of $4.6 billion increased 1 percent compared to the year-ago period. Organic sales increased 4 percent.

Diluted net income per share for the third quarter was $1.94 in 2019 and $1.29 in 2018.

Third quarter adjusted earnings per share were $1.84 in 2019 and $1.71 in 2018. Adjusted earnings per share exclude certain items described later in this news release.

Diluted net income per share for full-year 2019 is expected to be $5.75 to $6.00.

The company is now targeting full-year 2019 organic sales growth of 3 to 4 percent and adjusted earnings per share of $6.75 to $6.90. The prior outlook was for organic sales growth of 3 percent and adjusted earnings per share of $6.65 to $6.80.

Fourth quarter 2019 net sales of $4.6 billion were even with the year-ago period, while organic sales increased 3 percent. Full-year 2019 net sales of $18.5 billion were even with the year-ago period, while organic sales increased 4 percent.

Diluted net income per share for the fourth quarter was $1.59 in 2019 and $1.18 in 2018. Full-year diluted net income per share was $6.24 in 2019 and $4.03 in 2018.

Fourth quarter adjusted earnings per share were $1.71 in 2019, up 7 percent compared to $1.60 in 2018. Adjusted earnings per share exclude certain items described later in this news release.

Full-year adjusted earnings per share were $6.89 in 2019, up 4 percent compared to $6.61 in 2018. The company’s previous guidance was for adjusted earnings per share of $6.75 to $6.90.

Net sales in 2020 are expected to increase 1 percent year-on-year, including organic sales growth of 2 percent. Diluted net income per share for 2020 is anticipated to be $5.95 to $6.65. Adjusted earnings per share in 2020 are expected to be $7.10 to $7.35.

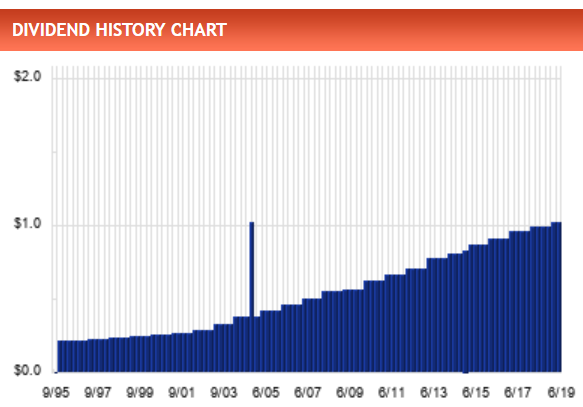

The company’s Board of Directors has approved a 3.9 percent increase in the quarterly dividend, which is the 48th consecutive annual increase in the dividend.

Estoy entre KMB y RB para incorporar a mi cartera (ya llevo PG), cuál consideráis más optima a largo plazo? En principio me había decantado por KMB pero con la idea de intentar diversificar geográficamente surge la posibilidad de RB.

En fin, que a ver si aportáis algún dato que me haga decantarme por una o por otra ya que me gustan mucho ambas.

Hola

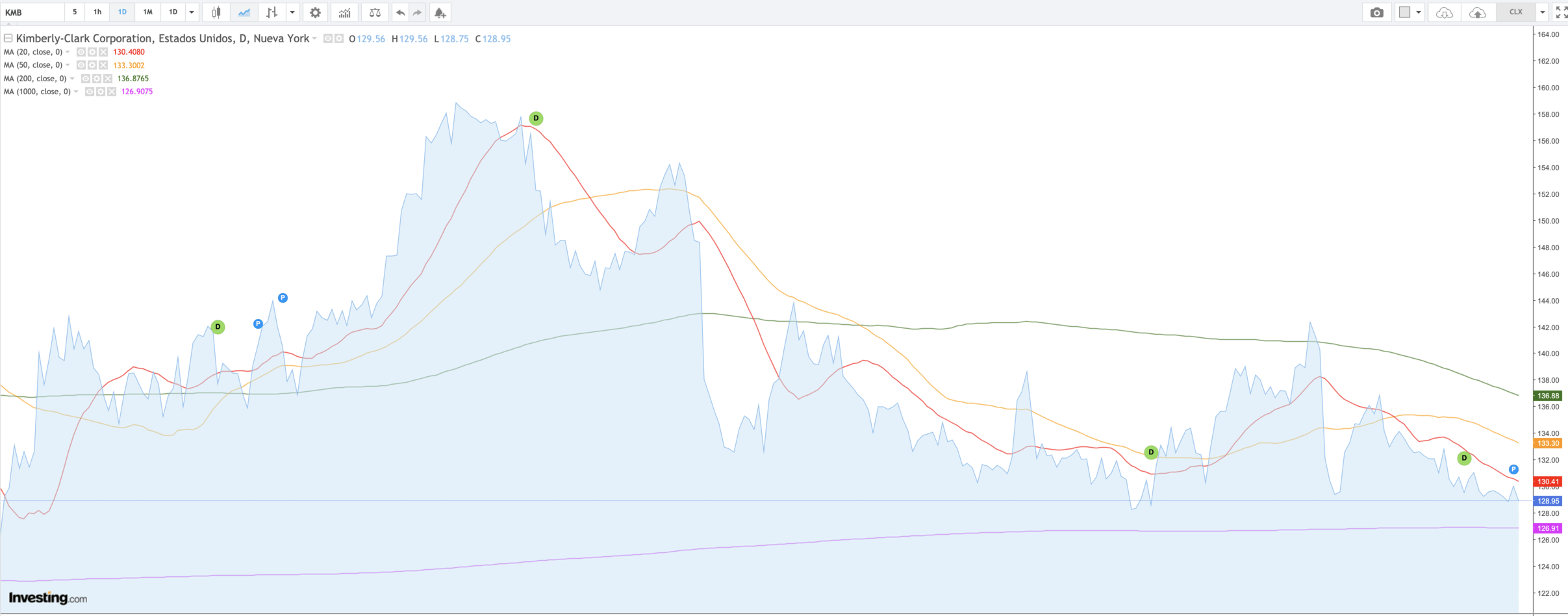

Creo que KMB está en máximos o casi. Sin entrar en más análisis. El precio tan alto es de poco para acá, un mes o así. Por algún sitio leí que su precio objetivo podía estar en 138 pero no sé…

Y luego estudiarla un poco con estos tiempos…

Pues efectivamente,

De aquel furor por el papel higiénico vienen estos lodos. Así que nada, ya he visto que algunos habéis aprovechado. Buena idea… .Esta semana a lo mejor me animo también, si llego a tiempo…

La caída de la demanda de papel higiénico provoca la peor caída de las ventas de Kimberly-Clark en una década

Las ventas en el segmento de tejidos de consumo cayeron más rápidamente de lo esperado por la compañía y las interrupciones en la cadena de suministro afectaron negativamente; es probable que haya más aumentos de precios

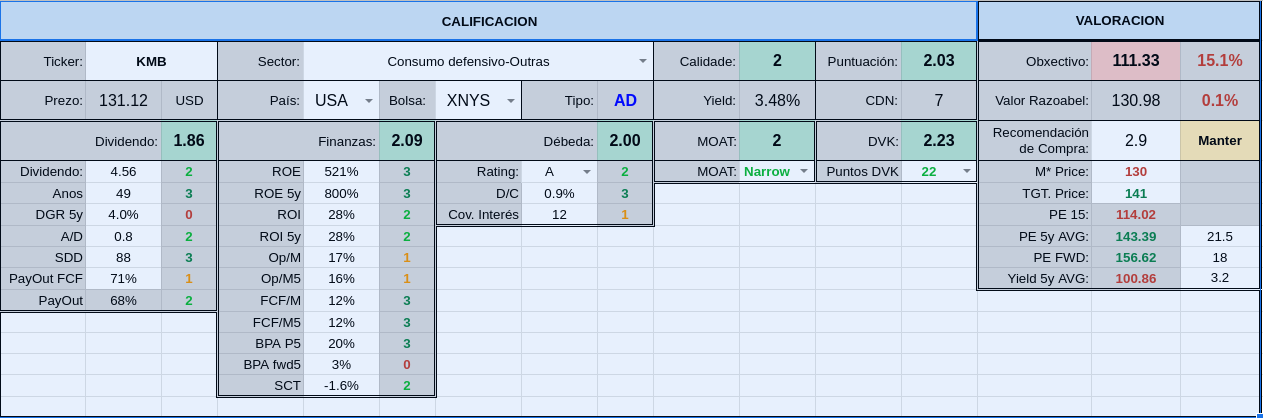

Por si te sirve de algo. Síntesis rápida y resumida que hago de primer filtro antes de seguir investigando.

El precio objetivo es orientativo, al ser de calidad 2 en mi escala de 0 a 3, le asigno un margen del -15% sobre el valor razonable.

Los datos son extraídos de M* y finviz en su mayoría.