Abro hilo para LVMH (Louis Vuitton Moët Hennessy), posiblemente la empresa lídel del sector del lujo. Me sorprendió ver una empresa de este sector en la cartera de alguno de los referentes (Lluís me parece recordar) porque pensaba que era una empresa que movía mucho menos dinero.

Pego la noticia con el incremento del 11,4% en el beneficio de 2016:

Joya de empresa. La pille sobre los 110€ y no para de dar alegrias, la ultima una subida de dividendos del 13%. Tambien hace unos años repartio acciones de Hermes, que tambien conservo. Esta es de las de no vender nunca.

Qué pena que tenga una rpd tan bajita. Es una empresa que me encanta y me tienta, creciendo a doble dígito. Pero del 2% no bajo.

Los asiáticos, y los chinos en particular, se vuelven locos por el lujo occidental (cuando aquí siempre hemos venerado el lujo asiático; se confirma que a todo el mundo le gusta más lo de fuera…)

A ver si alguna vez el mercado nos da la oportunidad. Pero es difícil.

Mucho tendria que bajar para que la RPD que tiene ahora de 1,6% se nos pusiera al 3%. Ese 3% es el minimo que pido, solo me lo he saltado con MMM, HD y RB. Con LVMH la compraria si llegara al 2,8%.

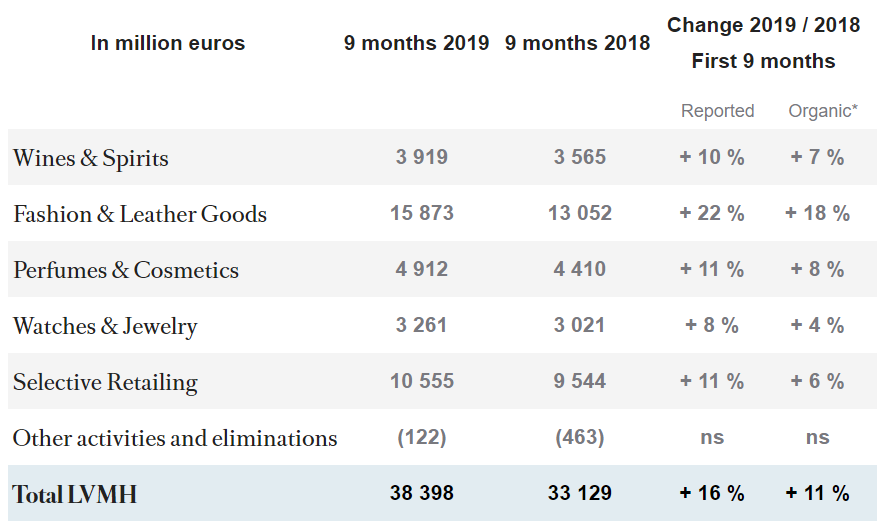

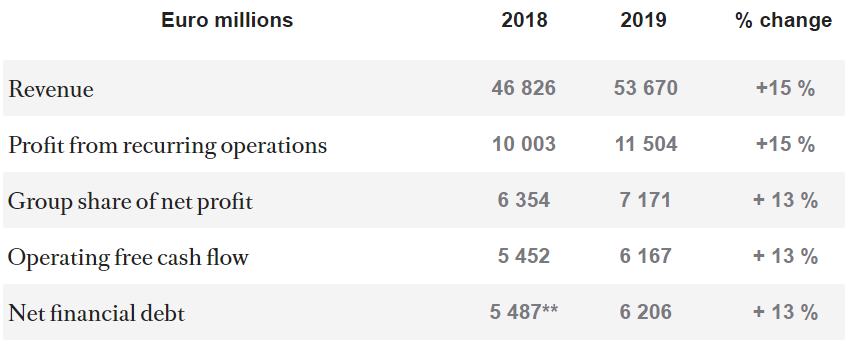

LVMH Moët Hennessy Louis Vuitton, the world’s leading luxury products group, recorded a 16% increase in revenue, reaching € 38.4 billion in the first nine months of 2019. Organic revenue grew 11% compared to the same period of 2018.

In the third quarter, revenue was up 17% compared to the same period in 2018. Organic revenue growth was 11%, a performance in line with the trend recorded in the first half of the year. The United States and Europe saw good progress in the third quarter, as did Asia, despite the difficult context in Hong Kong.

We are increasing our fair value estimate for Tiffany & Co to USD 135, to reflect the successful bid by LVMH. The transaction is approved by the boards of both companies and is expected to close in the middle of 2020 after approvals of Tiffany’s shareholders and regulatory bodies. The transaction does not have a material impact on our fair value estimate for LVMH.

We believe the multiple paid (EV/sales of 3.7 times and EV/EBITDA of almost 16 times) to be steep. In our view, Tiffany would need to accelerate revenue growth to the high single digits and operating margin to above 25% to justify the price paid (this compares with three-year historical revenue growth of 2.7% and average operating margin of 18.3%). The high price paid underscores the scarcity of established fine jewellery brands in the market and high entry barriers to this industry, in our opinion.

We expect Tiffany to continue operating as a standalone brand within LVMH organization, but we expect it to benefit from better and faster negotiating terms with landlords, pulling research and development resources (for example for developing perfumes), and sharing know-how and talent pools.

As we stated previously, accelerating growth at Tiffany (which would ultimately lead to margin expansion through operating leverage) would be the path to unlock value but would require additional resources (store openings, refurbishment, and brand building activities).