Yo no. Y depués de mucho pensar (y leer) la dejo en cartera.

4 Me gusta

Hola Jaquemate

Has encontrado algo interesante en lo que has leido?

Gracias y salu2

Lo ha vuelto a hacer.

The software firm was chosen to advance the next phase of the Army’s competitive $823M indefinite delivery, indefinite quantity (IDIQ) contract.

2 Me gusta

4 Me gusta

Buena noticia, Ahora solo cabe esperar que no vuelvan a diluir la empresa de nuevo.

We are raising our fair value estimate for narrow-moat Palantir Technologies PLTR to $31 per share from $28 after third-quarter results provide us with increased conviction in the company’s strong growth prospects, even while amassing scale. Year-over-year sales growth of 36% matched our expectations, while adjusted earnings per share of $0.04 came in slightly higher than we anticipated.

Shares fell as much as 10% after Palantir reported results, which we believe is due to government revenue declining 6% sequentially, although against a tough comparison, and the fourth-quarter outlook potentially being conservative. Taking a longer-term view and being upbeat about Palantir’s tailored use case software modules making its software more easily consumable across industries and organization sizes, we believe the negative reaction creates an attractive entry point for investment.

The strong sales growth came from commercial growth accelerating to 37% while government grew 34%, both year over year; commercial was 44% of revenue in the quarter. Palantir’s customer count grew by 34 net new customers to 203, with commercial customers up 46% sequentially. Total remaining deal value grew to $3.6 billion, up 50% year over year, and commercial deal value grew to $2.2 billion, up 101% year over year. While we expect steady government backlog and new contracts to account for more than half of sales for years to come, we believe commercial can become the larger contributor in the long term. We positively view the momentum in commercial and Palantir expanding its use cases through new modules, which we believe serve as hooks to initially land a customer before proliferating Palantir’s use cases across an organization and its ecosystem. This can lead to solid operating margin expansion in the long term. We believe the 30% adjusted operating margin in the quarter was a strong result amid Palantir’s ramping up sales and distribution investments to spur lofty growth goals.

3 Me gusta

Yo a esta empresa la tengo en el radar, su futuro parece prometedor pero está por verse como transforma todo eso que gana en retribución al accionista, porque hasta ahora todo se evapora en retribuciones a los empleados/directivos.

Con todo el “hype” que tiene en las redes y no sale disparada fuera del rango 20-30$ quizá sea por eso, habrá que tener paciencia.

3 Me gusta

Tremendo bajón que lleva, rondando ahora los 13,50 $.

Morningstar le da un FV de 31$ y Narrow Moat.

Alguien conoce en qué quedó lo de la dilución?

Oportunidad o trampa?

3 Me gusta

(M*)

We are maintaining our $31 fair value estimate for narrow-moat Palantir Technologies PLTR after its fourth-quarter results exceeded our expectations for revenue growth but lagged our anticipation for earnings as the firm aggressively ramps up its headcount. Palantir’s shares being punished for missing FactSet consensus earnings expectations in the quarter, and heightened investments expected in 2022, create a solid buying opportunity for long-term investors. We think the sell-off is near-term reactionary and is missing the long-term vision of Palantir becoming an essential component of data operations for commercial and government entities. Palantir proliferating its salesforce is crucial to keep the strong momentum in commercial customer adds and driving profound retention metrics once landing a client, in our view. We think its software creating insight from deluges of data becomes invaluable to customers. The reaffirmation of expecting at least 30% annual sales growth through 2025 with a keen focus on expanding margin with scale provides us with confidence that its prospects are still in their early stages.

Compared with the prior year, revenue grew 34% in the quarter, led by commercial growing by 47% and government expanding by 26%. The bulk of Palantir’s growth comes from existing customers, and we believe its trailing 12-month 131% net dollar retention shows its ability to land then expand spending from organizations. With Palantir’s software becoming essential once embraced, we think growing the customer base is key for the long term. The company added 34 new commercial customers in the fourth quarter and ended 2021 with 147 commercial clients and 90 government customers. We believe Palantir’s more nascent software module approach, making its products easily consumable and addressing specific use cases, is helping drive customer engagements, and the company is acting wisely in hiring aggressively to keep landing clients and diversify its revenue streams.

8 Me gusta

Cathie Wood se ha quitado 30M de acciones de PLTR durante la última semana

Coooompra Claraaaaa … que diría Captur

3 Me gusta

“Buy high and sell low seems to be the mantra of ARK Invest lately”.

2 Me gusta

Yo he cogido unas cuantas a 10 en el pre

-10% en pre-market

1 me gusta

Por si alguien aún no ha tirado la toalla y está dentro.

1 me gusta

“Hold cash, blue-chip stocks, take care of your health and relationships, and keep gambling to under 1% of your net worth”

Palantir se engloba en la última categoría

2 Me gusta

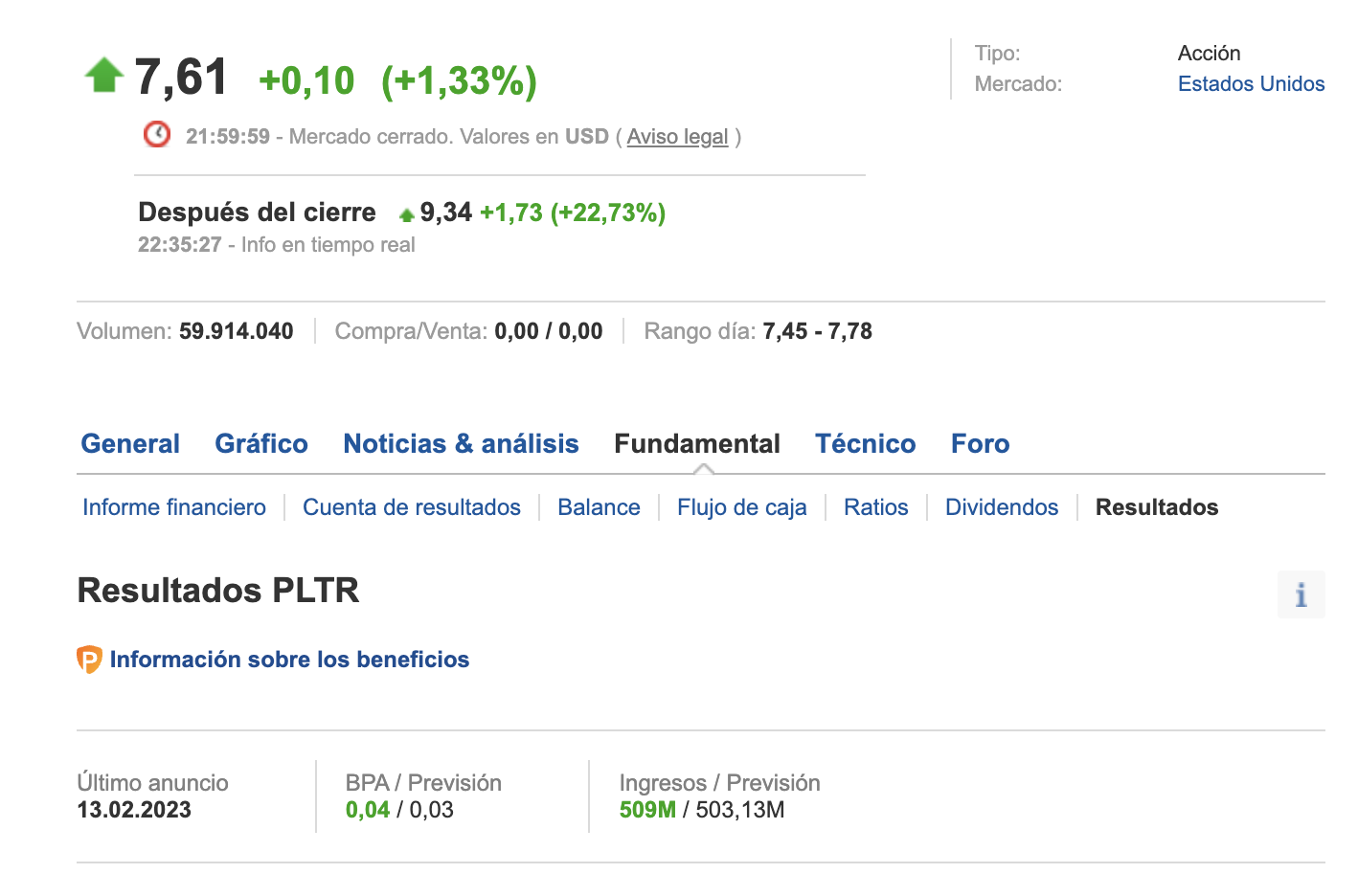

Acciones de Palantirsubió hasta un 19% en operaciones extendidas el lunes después de que la compañía publicara ganancias del cuarto trimestre que superaron las estimaciones de los analistas en los resultados.

Así es como lo hizo la compañía:

- BPA: 4 céntimos ajustados frente a los 3 céntimos esperados por los analistas, según Refinitiv

- Ingresos: $509 millones frente a los $502 millones esperados por los analistas, según Refinitiviv.

Los ingresos de Palantir para el trimestre aumentaron un 18 % año tras año, y sus ingresos comerciales en EE. UU. crecieron un 12 %. La compañía de software, que es conocida por su trabajo con el gobierno, dijo que su número de clientes comerciales de EE. UU. aumentó un 79% año tras año, pasando de 80 clientes a 143.

La compañía también reportó su primer trimestre de ingresos netos positivos sobre una base GAAP, de $31 millones.

“Con este resultado, Palantir es rentable”, dijo el CEO Alex Karp en el comunicado . “Este es un momento significativo para nosotros y nuestros seguidores”.

Palantir dijo que espera reportar entre $ 503 millones y $ 507 millones en ingresos durante su primer trimestre, y entre $ 2,18 mil millones y $ 2,23 mil millones para todo el año.

En una carta a los accionistas , Karp dijo que la compañía espera generar ganancias para el año fiscal en curso, lo que marcaría el primer año rentable de Palantir en la historia de la compañía.

Dijo que un importante negocio comercial estadounidense ha surgido en Palantir en los últimos dos años y que refleja la “demanda implacable” de los clientes. En 2018, Palantir generó un total de $ 38 millones de su negocio comercial en EE. UU., pero a partir de 2022 generó $ 335 millones, dijo Karp.

“Cuando recién comenzábamos, muchos dudaban de nuestra capacidad para evolucionar más allá de algo más que un proveedor especializado de software para un puñado de clientes gubernamentales, y mucho menos generar ingresos significativos del sector gubernamental en su conjunto”, escribió Karp. “Ellos estaban equivocados.”

La compañía llevará a cabo su llamada trimestral con inversores a las 5:00 p. m. ET del lunes.

1 me gusta