Gracias por el aporte tan detallado!! ![]()

1 me gusta

El compi es un crack.

Y tú tmb puedes serlo! Aquí la empresa te deja todos los datos:

Tienes Excel con todo allí.

2 Me gusta

Si, ya brujulee por la web varias veces, pero debía tener el día bastante espeso que no era capaz de sacar una previsión más o menos clara de que van a hacer con el dividendo en el futuro…

De todos modos me pareció leer estos días que iban a revisar el anterior plan estratégico y sacar uno nuevo para adaptarlos a la realidad de los nuevos precios del petróleo.

2 Me gusta

Hola. Alguna noticias de los resultados de Petrobras y sus dividendos?

Muchas gracias

1 me gusta

Ajo y agua.

Se deja un 7% hoy

2 Me gusta

Que pasa que la gente contaba con ello?

Lo mejor para mis puts vendidas ![]()

![]()

1 me gusta

Vete a saber.. hace tiempo que dejé de buscar la racionalidad en el mercado con los resultados trimestrales

1 me gusta

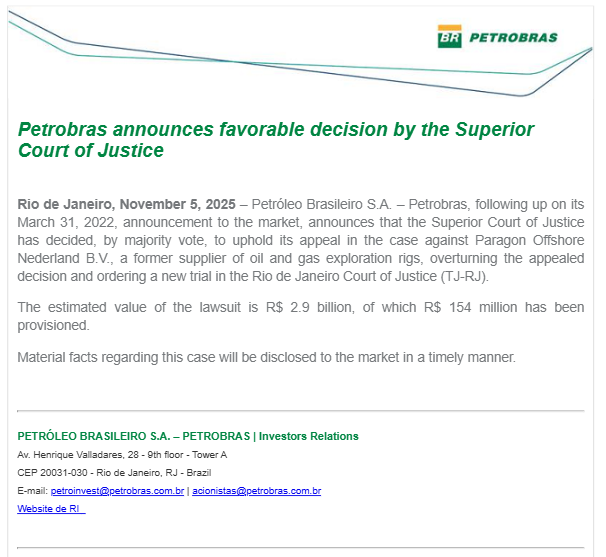

Petrobras announces favorable decision by the Superior Court of Justice

Rio de Janeiro, November 5, 2025 – Petróleo Brasileiro S.A. – Petrobras, following up on its March 31, 2022, announcement to the market, announces that the Superior Court of Justice has decided, by majority vote, to uphold its appeal in the case against Paragon Offshore Nederland B.V., a former supplier of oil and gas exploration rigs, overturning the appealed decision and ordering a new trial in the Rio de Janeiro Court of Justice (TJ-RJ).

The estimated value of the lawsuit is R$ 2.9 billion, of which R$ 154 million has been provisioned.

Material facts regarding this case will be disclosed to the market in a timely manner.

2 Me gusta

no entendía de que iba e hice esta infografía:

1 me gusta

Igual se le va la olla… dejo el informe que genero:

Analysis of the Petrobras Investor Release Dated November 5, 2025

Analysis of the Petrobras Investor Release Dated November 5, 2025

Executive Summary

On November 5, 2025, Petróleo Brasileiro S.A. – Petrobras (Petrobras) announced a “favorable decision” by Brazil’s Superior Court of Justice (STJ) in a long-running legal dispute with former rig supplier Paragon Offshore Nederland B.V. (Paragon). This ruling annuls a prior appellate judgment that had exposed Petrobras to a liability estimated at R$ 2.9 billion (approximately $550 million USD).

This report finds that while the STJ’s decision is a significant procedural victory that provides immediate relief to Petrobras’s balance sheet and income statement, it is not a final resolution. The STJ has remanded the case for a new trial at the Rio de Janeiro Court of Justice (TJ-RJ). The core liability, rooted in contract cancellations from the “Operation Car Wash” (Lava Jato) era, has been deferred, not extinguished.

The financial materiality of this event is best understood by contrasting the total R$ 2.9 billion claim against the R$ 154 million Petrobras has provisioned, a figure indicating the company’s internal assessment of the probable loss is only 5.3% of the total potential exposure. The STJ’s ruling validates this aggressive accounting posture for the time being, preventing a P&L charge of approximately R$ 2.75 billion.

This analysis deconstructs the legal ruling, details the financial stakes and their evolution, traces the dispute’s origin to the Lava Jato scandal, and identifies the true plaintiff as a litigation trust representing pre-2016 creditors. Finally, it contrasts this legacy legal headwind with new, highly favorable regulatory tailwinds, chiefly Law 15,075/2024, which enhances the value of Petrobras’s core assets.

Deconstruction of the November 5, 2025, STJ Decision

A Favorable Ruling, Not a Final Victory: The Legal “Reset”

The November 5, 2025, “Material Fact” issued by Petrobras details a “favorable decision by the Superior Court of Justice”. This ruling, however, is not a final judgment on the merits of the case. The STJ, acting as Brazil’s highest court for non-constitutional matters, explicitly “overturn[ed] the appealed decision and order[ed] a new trial in the Rio de Janeiro Court of Justice (TJ-RJ)”.

This is a critical distinction. Petrobras has not been absolved of liability. It has achieved a procedural victory that “resets” the legal battle. The STJ’s decision vacates a prior, adverse judgment from the TJ-RJ, forcing the case back to that same state-level appellate court for a new hearing. The immediate threat of a multi-billion-real judgment being confirmed has been deferred, and what was a contingent liability remains contingent.

The Legal Grounds for Annulment: A Procedural Flaw

While the official Petrobras press release is silent on the reason for the STJ’s decision, merely stating it was “by majority vote” , supplementary reporting from Brazilian legal news sources provides the missing detail. The STJ’s Third Panel (3ª turma) annulled the judgment because it “considerou irregular a composição do órgão julgador no TJ/RJ” (considered the composition of the judging body in the TJ-RJ irregular).

Petrobras’s legal victory was therefore achieved on a procedural technicality, albeit one of fundamental legal importance. The STJ did not rule on the core facts of the contract dispute—namely, whether Petrobras was justified in canceling Paragon’s rig contracts. It ruled that the TJ-RJ panel that found Petrobras liable in 2022 was improperly formed, rendering its entire judgment void. This legal strategy allowed Petrobras to avoid a potentially unfavorable STJ ruling on the complex facts of the case, which are entangled with the Lava Jato scandal. The “procedural reset” grants Petrobras a new appeal hearing at the TJ-RJ, presumably before a different, and properly composed, judicial panel.

Reversal of the March 2022 Judgment: The Full Litigation Timeline

The November 2025 announcement is a direct follow-up to Petrobras’s market announcement on March 31, 2022. That 2022 event was a significant loss for Petrobras. On that date, the TJ-RJ “decided, by majority vote, to grant the appeal of the company Paragon Offshore Nederland B.V.”. This 2022 ruling created the multi-billion-real liability by reversing a (presumed) lower trial court decision that had been in Petrobras’s favor.

The legal history is a multi-year battle between judicial levels:

- Trial Court (Implied): Paragon’s initial claim is dismissed or granted minimal damages, leading Petrobras to carry a low provision.

- TJ-RJ (March 2022): Paragon appeals. The TJ-RJ reverses the trial court, ruling against Petrobras and establishing the massive liability.

- STJ (November 2025): Petrobras appeals the 2022 loss. The STJ annuls the TJ-RJ’s judgment on procedural grounds and orders a new appeal trial at the TJ-RJ.

The full timeline, placing the legal battle in its corporate context, is as follows:

Table 1: Timeline of the Petrobras-Paragon Litigation (2014-2025)

| Date | Event | Legal/Corporate Venue | Financial Impact/Valuation |

|—|—|—|—|

| 2014 | Paragon Offshore spun off from Noble Corporation. | Corporate Transaction | N/A |

| Sep 2015 | Petrobras terminates Paragon DPDS2 contract. | Breach of Contract | $493M in disputed backlog (for both rigs). |

| Feb 2016 | Paragon Offshore files for Chapter 11 Bankruptcy. | U.S. Bankruptcy Court, Delaware | N/A |

| Aug 2016 | Petrobras terminates Paragon DPDS3 contract. | Breach of Contract | See above. |

| Jul 2017 | Paragon emerges from Chapter 11; Litigation Trust formed. | U.S. Bankruptcy Court, Delaware | Legal claims transferred to trust. |

| Mar 2018 | Borr Drilling acquires Paragon’s physical rig assets. | Corporate Transaction | N/A |

| Mar 31, 2022 | TJ-RJ rules against Petrobras, granting Paragon’s appeal. | Rio de Janeiro Court of Justice (TJ-RJ) | Claim: R$ 1.9B; Provision: R$ 59M. |

| Nov 5, 2025 | STJ annuls 2022 TJ-RJ ruling, orders new appeal trial. | Superior Court of Justice (STJ) | Claim: R$ 2.9B; Provision: R$ 154M. |

Financial Materiality: Analyzing the R$ 2.9 Billion Exposure

Decoding the Provision: R$ 154M (Probable) vs. R$ 2.9B (Possible)

The November 2025 release states: “The estimated value of the lawsuit is R$ 2.9 billion, of which R$ 154 million has been provisioned”. This discrepancy is the key to understanding Petrobras’s risk posture.

In financial reporting, these terms have precise meanings. The “Estimated Value” (R$ 2.9 billion) represents the total possible loss, or the full amount of the claim. This is the maximum exposure Petrobras is disclosing to investors. The “Provisioned” amount (R$ 154 million) is a liability that has been recognized on the balance sheet. A company only provisions a contingent loss when it is deemed (1) probable (i.e., more likely than not to occur) and (2) the amount can be reasonably estimated.

Therefore, Petrobras’s legal and accounting teams have concluded that the probable loss from this R$ 2.9 billion claim is only R$ 154 million. The remaining R$ 2.746 billion is classified as a possible loss—a risk significant enough to disclose in financial statement footnotes, but not probable enough to require a charge against earnings.

Provisioning only 5.3% of the total claim is an aggressive stance, signaling strong confidence from Petrobras in its underlying legal defense. The STJ victory serves as a crucial accounting justification. Had Petrobras lost its STJ appeal, the R$ 2.9 billion liability would have been confirmed, forcing an immediate charge to the company’s income statement of R$ 2.746 billion (the total claim less the existing provision). This procedural win allows the liability to remain classified as “contingent” and “possible,” protecting the 2025 income statement from a catastrophic, multi-billion-dollar non-cash expense.

Evolution of Risk Assessment (2022-2025)

A comparison of the 2022 and 2025 announcements reveals a significant evolution in the financial figures. - March 2022 Data: “estimated value… is R$ 1.9 billion of which R$ 59 million have been provisioned”.

- November 2025 Data: “estimated value… is R$ 2.9 billion, of which R$ 154 million has been provisioned”.

This change quantifies the impact of the 2022 TJ-RJ loss and the cost of ongoing litigation.

Table 2: Evolution of Financial Exposure (2022 vs. 2025)

| As of Date | Official Estimated Value (Total Claim) | Provisioned Amount (Probable Loss) | Un-provisioned “Possible” Exposure | Provision as % of Total Claim |

|—|—|—|—|—|

| March 31, 2022 | R$ 1.9 Billion | R$ 59 Million | R$ 1.841 Billion | 3.1% |

| November 5, 2025 | R$ 2.9 Billion | R$ 154 Million | R$ 2.746 Billion | 5.3% |

The R$ 1 billion (53%) increase in the “estimated value” from 2022 to 2025 is most likely attributable to contractual interest, inflation indexing common in Brazilian judgments, and currency adjustments on a claim that was originally based in U.S. dollars.

More telling is the provisioned amount, which grew by 161% (from R$ 59M to R$ 154M). This provision grew much faster than the total claim, raising the provision-to-claim ratio from 3.1% to 5.3%. This indicates that in the period between its 2022 loss at the TJ-RJ and the 2025 STJ appeal, Petrobras’s internal assessment of its probable loss had worsened. The 2022 loss clearly damaged the company’s confidence, forcing it to increase the provision. This “provision creep” was on a dangerous trajectory that the STJ victory has, for now, arrested.

Reconciling Competing Valuations

While the research contains various figures, the company’s official filings provide clarity. The R$ 1.9 billion figure was the official 2022 valuation. News reports from 2022 of “~400 million” were simply conversions of that R 1.9B figure. A legal news report mentioning R$ 4.5 billion is an outlier and likely an error or includes punitive damages not recognized by Petrobras. The R$ 2.9 billion figure from the November 5, 2025, release, which was also filed with the U.S. Securities and Exchange Commission (SEC), stands as the definitive, official estimated value of the lawsuit.

Genesis of the Dispute: Contract Cancellations in the Shadow of Scandal

The Original Contract Dispute (2015-2016)

The lawsuit originates from Petrobras’s decision in 2015-2016 to prematurely terminate drilling contracts for two of Paragon’s deepwater drillships: the Paragon DPDS2 and the Paragon DPDS3. At the time, Paragon stated these two contracts alone represented $493 million in its contract backlog.

The DPDS2 contract was terminated in September 2015, well ahead of its scheduled March 2017 conclusion. The DPDS3 was terminated in August 2016, versus its original August 2017 end date.

The official legal basis for the dispute is technical. Petrobras’s interpretation was that it could terminate the contracts due to excessive “non-working ‘shipyard’ time” and maintenance delays. Paragon’s interpretation was that this shipyard time, which was extensive, should have extended the contract terms rather than voided them. The R$ 2.9 billion claim is the legacy of this $493 million contract dispute, compounded by nearly a decade of interest and penalties.

The “Operation Car Wash” (Lava Jato) Context

These contract cancellations did not occur in a vacuum. They were executed at the height of the “Operation Car Wash” (Lava Jato) corruption scandal, which erupted in March 2014. The scandal involved “billions of dollars in kickbacks” and “hundreds of millions of dollars in corrupt payments to politicians” facilitated by Petrobras executives to rig supplier contracts.

Paragon Offshore was directly implicated in the scandal’s periphery. Paragon’s own SEC filings acknowledged that its commercial agent in Brazil “pleaded guilty in Brazil in connection with the award by Petrobras of a drilling contract to one of Paragon’s competitors” as part of the wider investigation.

This provides the critical, unstated context for the contract dispute. While Petrobras’s official legal argument was technical (shipyard delays), its true motive for terminating the contracts was almost certainly their link to the corruption scandal. Petrobras was under immense pressure from U.S. and Brazilian authorities to clean house and void tainted contracts. Petrobras likely used the “shipyard time” as a convenient, technical pretext to void contracts that were politically and legally toxic. This underlying complexity is why the legal battle has been so protracted and contentious.

The Plaintiff’s Labyrinth: Who is Paragon Offshore Nederland B.V.?

Corporate Lineage: Spin-off, Bankruptcy, and Acquisition

The plaintiff, “Paragon Offshore Nederland B.V.,” is a Dutch subsidiary of a company that no longer exists in its original form. - 2014: Paragon Offshore plc was spun off from Noble Corporation.

- 2016: Crippled by the oil price crash and contract cancellations (including from Petrobras), Paragon filed for Chapter 11 bankruptcy.

- 2017: Paragon emerged from bankruptcy, having shed approximately $2.3 billion in debt.

- 2018: The restructured Paragon was acquired by Borr Drilling.

The True Beneficiary: The Paragon Litigation Trust

Crucially, the entity suing Petrobras is not Borr Drilling. The 2018 acquisition by Borr was for Paragon’s physical assets—its rig fleet.

During the 2017 bankruptcy reorganization, a “Litigation Trust Agreement” was established. The sole purpose of this trust was to “pursue claims against Noble Corporation plc… and other third parties” and “distribute the proceeds to beneficiaries”. “Paragon Offshore (Nederland) B.V.” was one of the debtor entities whose assets, including legal claims, were transferred to this trust.

Petrobras is therefore not in a fight with an active industry competitor. It is in a legal battle with the “ghost” of Paragon: a single-purpose trust representing pre-2016 creditors who were otherwise wiped out. This lawsuit is the trust’s primary asset, and any recovery is 100% profit for those legacy creditors. This explains the plaintiff’s tenacity and makes a simple settlement less likely.

Strategic Implications and Forward-Looking Analysis

Impact on Petrobras’s Risk Profile

The November 5, 2025, ruling is a significant positive event for Petrobras. It removes an immediate, multi-billion-dollar judgment from its books, deferring the potential liability indefinitely. It validates, for now, the company’s aggressive accounting stance of provisioning only R$ 154M against a R$ 2.9B claim. The risk, however, is not extinguished. The case now returns to the TJ-RJ, the very court that ruled against Petrobras on the merits in 2022.

The Broader Legal and Regulatory Horizon: Headwinds and Tailwinds

Investors should analyze Petrobras through a dual lens: the management of legacy risks versus the emergence of new, favorable opportunities.

Legacy Headwind: The Paragon lawsuit is one of the last major “zombie liabilities” from the Lava Jato era. This period has been immensely costly, forcing Petrobras into a $3 billion settlement in a U.S. securities class action and a $853.2 million FCPA settlement with the DOJ and SEC. The Paragon case is a multi-billion-dollar remnant of this same period.

New Tailwind (Law 15,075/2024): In stark contrast to its legacy legal battles, Petrobras is now operating in a new, highly favorable domestic regulatory environment. Law 15,075/2024, enacted in December 2024, is unequivocally positive for Petrobras. Its key provisions include: - Local Content Flexibility: Allows the “transfer of local content surpluses among contracts,” easing a major administrative and financial burden.

- Royalty Reduction: Authorizes the Executive Branch to “reduce the royalty rate… by up to 5%” for “Round Zero” contracts as an incentive for new investment.

- Extension of Production Sharing Agreements (PSAs): Most critically, the law allows for the “extension of the Production Sharing Agreements terms… as long as it is demonstrated that it is advantageous for the Federal Union”.

The STJ ruling and the new law, while unrelated, together paint a picture of a company with strong institutional support from both the judicial and legislative branches of the Brazilian government.

Conclusion and Analyst Recommendations

The STJ’s November 5, 2025, decision is a significant tactical victory. It defers a R$ 2.9 billion liability (R$ 2.746 billion un-provisioned) by vacating a 2022 appellate court loss on procedural grounds. The case, which concerns a $493 million contract dispute from 2015-2016 deeply intertwined with the Lava Jato scandal, now returns to the TJ-RJ for a new appeal.

Based on this analysis, the following recommendations are issued: - Monitor the New TJ-RJ Appeal: The key legal catalyst is now the new judgment from the Rio de Janeiro Court of Justice (TJ-RJ). The outcome, likely in 2026-2027, will determine if the R$ 2.9 billion liability is reinstated, dismissed, or modified.

- Monitor Quarterly Provisions: The primary indicator of Petrobras’s internal risk assessment is the “provisioned” amount (currently R$ 154 million). Any material increase in this line item in future quarterly reports will be the first signal that its confidence in winning the new appeal on the merits is fading.

- Model PSA Extensions: Analysts should shift focus to modeling the significant positive financial impact of Law 15,075/2024. The ability to extend high-value Production Sharing Agreements represents a tangible, long-term value-creation opportunity that may far outweigh the now-deferred and contingent risk of the Paragon lawsuit.

1 me gusta

1 me gusta

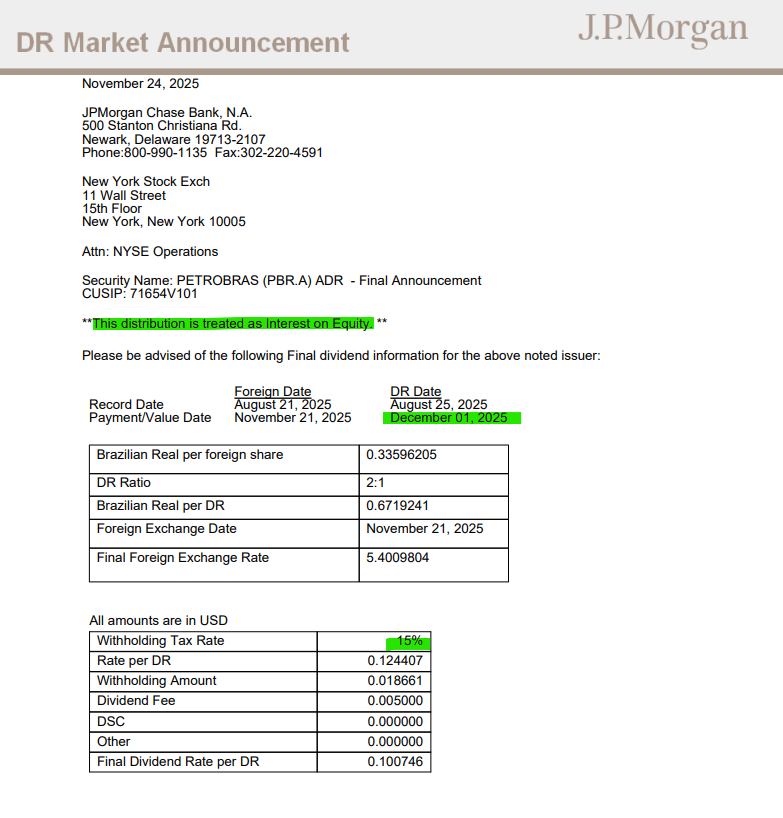

Si no estoy equivocado esta pagaba un dividendo el 1 de diciembre, pero en ing esta semana no me lo han ingresado ¿Será que no tocaba y me estoy columpiando? ¿Alguien lo ha cobrado?

En Degiro e IBKR pagaron,

2 Me gusta

Parece que me lo han pagado hoy por fin. Lo que noto es que ING me aplica retención en origen en casi todos los dividendos del adr este. Creía que Brasil no tenía retención en origen ¿A vosotros en otros brokers os cobran la retención en origen o es sólo en ing? Desde mayo sólo me han pagado los dos primeros dividendos sin retención en origen, uno en mayo y otro en junio, creo recordar. El resto vienen todos con la doble retención desde entonces

Petrobras cotiza en España a través del mercado Latibex (Bolsa de Madrid) con el ticker PBR, y también directamente en EE. UU. (NYSE) como American Depositary Receipts (ADRs) bajo los tickers PBR y PBR.a.

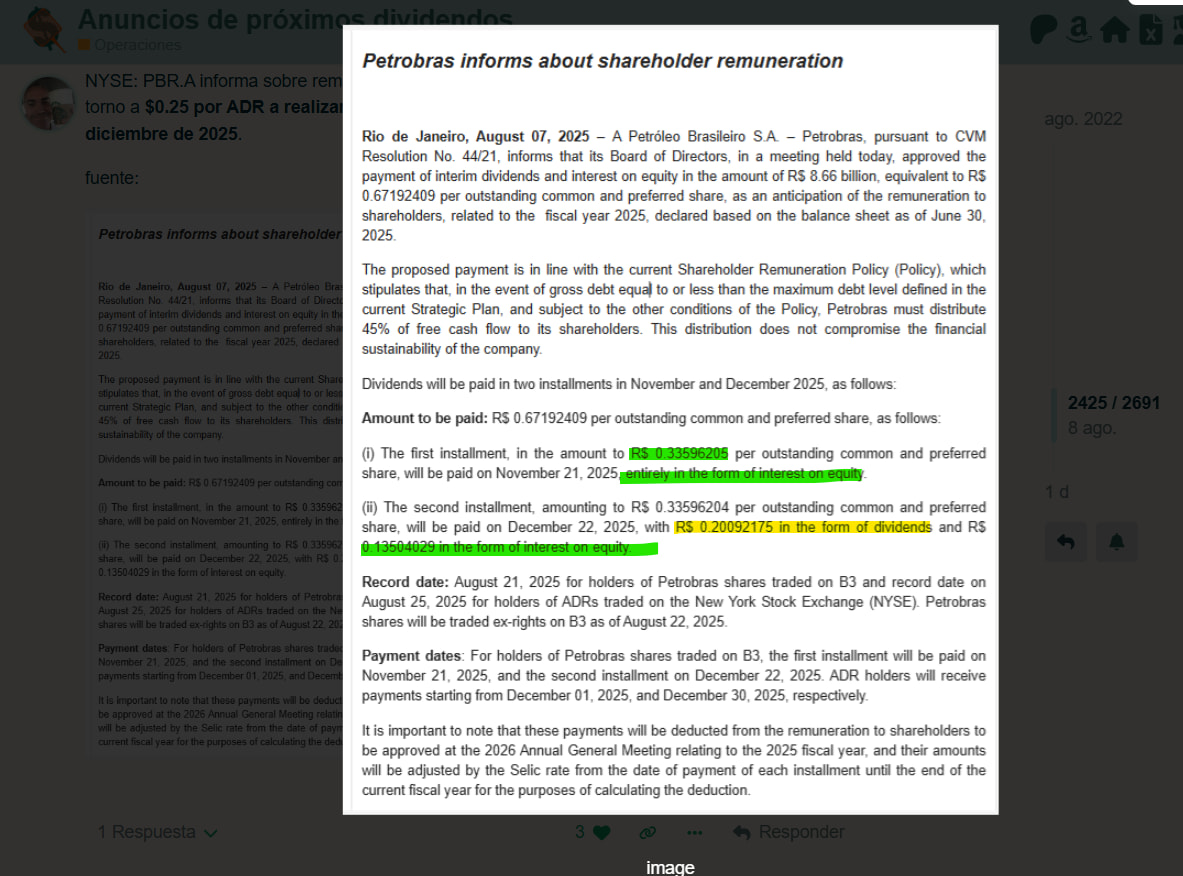

hola @furacu Petrobras hace pagos de dos tipos

Dividendos: Los pagos habituales de cualquier empresa. NO llevan retención en origen porque Brasil no tiene.

Interest on equity: Aquí está la clave, porque en este caso, los pagos los hacen como gastos de interés deducible de impuestos para la empresa por lo que SÍ llevan una retención en origen del 15%.

En el pago de esta fecha, tal como lo indican en el anuncio, se hacía completamenta de forma de Interest on equity

Que lleva una retención del 15%

El segundo pago, que lo recibiremos en torno al 30-31 de diciembre, va en dos partidas, R$0.20 como dividendo (sin retención) y el resto, R$0.13, como interest on equity

5 Me gusta

Esta ya me empieza a recordar a las bip y bep de los brookfields que cada pago de divis era un cachondeo hace años. Me da que en enero la largo y a otra cosa, porque desde mayo pocos dividendos me ha pagado, la verdad ![]()