En ING cobrados ambos

1 me gusta

@anbax @salvatierra

Me resulta raro/curioso efectivamente que cobre Altria y no PM.

Gracias. Indagaré más.

En IB ambos cobrados

2 Me gusta

En R4 tambien cobrados los dos

1 me gusta

A mí, para variar, en Selfbank tampoco está ingresado a día de hoy.

1 me gusta

… solo a falta de que regularicen la retención de PM en unos días.

Esta mañana ya me han ingresado dividendo de PM en Degiro pero la retención solo la han hecho de un 0’5 % aprox. imagino que rectificaran más tarde.

1 me gusta

Si, suelen hacer no sé cuantas correcciones, es algo curioso, si fuera algo nuevo podría entenderlo pero pm reparte dividendo 4 veces al año y en degiro lo tienen que corregir las 4. Me imagino al becario corrigiendo manualmente todas las retenciones de pm…

1 me gusta

Cierto es, lo han ingresado esta mañana. Y efectivamente la retención es muy rara… 2 centimos en mi caso  Esto ya me trastoca mi Excel

Esto ya me trastoca mi Excel

Pero bueno, lo importante es que esta cobrado supongo. Gracias a todos por los feedbacks

1 me gusta

A mi me han ingresado hoy los del día 1, tocará esperar

En el caso de PM, una parte importante del dividendo creo que va sin retencion en origen, el % libre no lo se.

4 Me gusta

Ummm a ver si va a estar bien entonces?

Gracias por ese dato

2 Me gusta

Acabo de mirar y la retención fue de un 15%

Desde hace ya algún tiempo IB lo hace así. Retiene inicialmente un 15% como con cualquier otra empresa de USA y unos pocos días más tarde hace la regularización típica de las compañías 80/20. Es decir, te devolverán pasta.

1 me gusta

Pues según mis cálculos en Degiro me han retenido el 0,55%…

Se escapó después de tocar no hace tanto los 70$

7 Me gusta

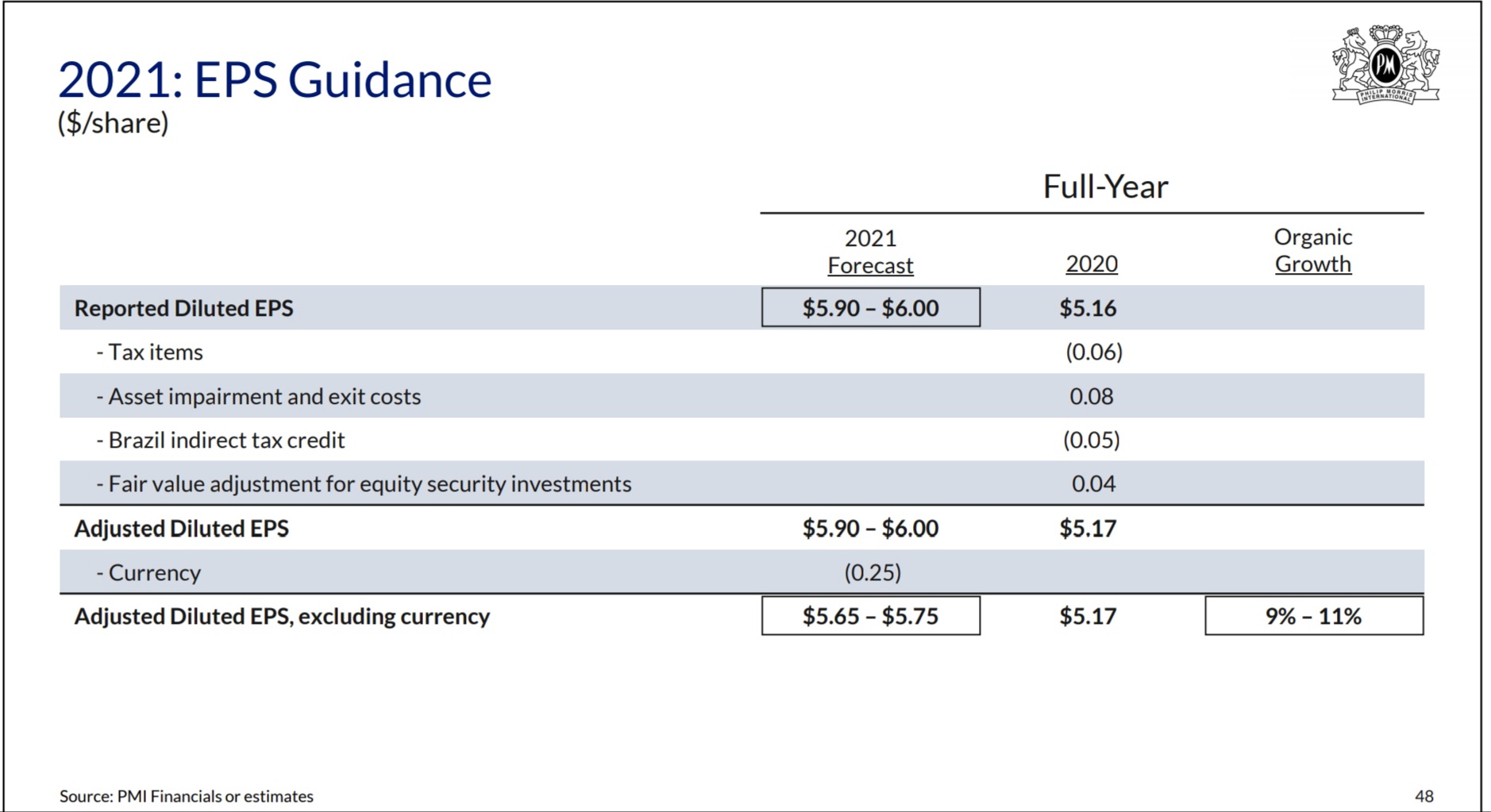

Philip Morris reaffirms FY2021 earnings outlook at Investor Day, unveils 2021-2023 targets

- Philip Morris International (NYSE:PM) reaffirms FY2021 diluted EPS of $5.90-$6.00, representing an increase of ~14%-16% vs. consensus of $6.

2021-2023 Targets & Assumptions:

- Net revenue and adjusted diluted EPS compound annual organic growth of more than 5% and 9%.

- ~40% of total net revenues from smoke-free products in 2023;

- Annual heated tobacco unit shipment volume of 140B-160B units in 2023;

- Around $2B in annualized gross cost efficiencies by 2023 vs. 2020 cost base;

- An average annual increase in adjusted operating margins of at least 150 bps on an organic basis;

- Around $35B in total operating cash flow over the three-year period at prevailing exchange rates;

- Estimated annual capital expenditures of around $0.B

- The company intends to begin a three-year share repurchase program of $5B-$7B in 2H21 and will maintain its progressive dividend policy while targeting a long-term dividend payout ratio of around 75% of adjusted diluted EPS.

- The company is moving to the next growth phase, further shifting to a better, more sustainable business by driving the development of the smoke-free category and leveraging leading commercial model with a launch of IQOS ILUMA—the next generation of IQOS heat-not-burn product featuring a new internal heating induction technology in 2H21.

- CEO comment: “As outlined today, we are well positioned to deliver excellent top- and bottom-line growth, as well as strong shareholder returns. We now aim to be a majority smoke-free product company by 2025, an important milestone toward our ambition to deliver a smoke-free future, to the benefit of adults who would otherwise continue to smoke, society, the company and our shareholders.”

8 Me gusta

4 Me gusta