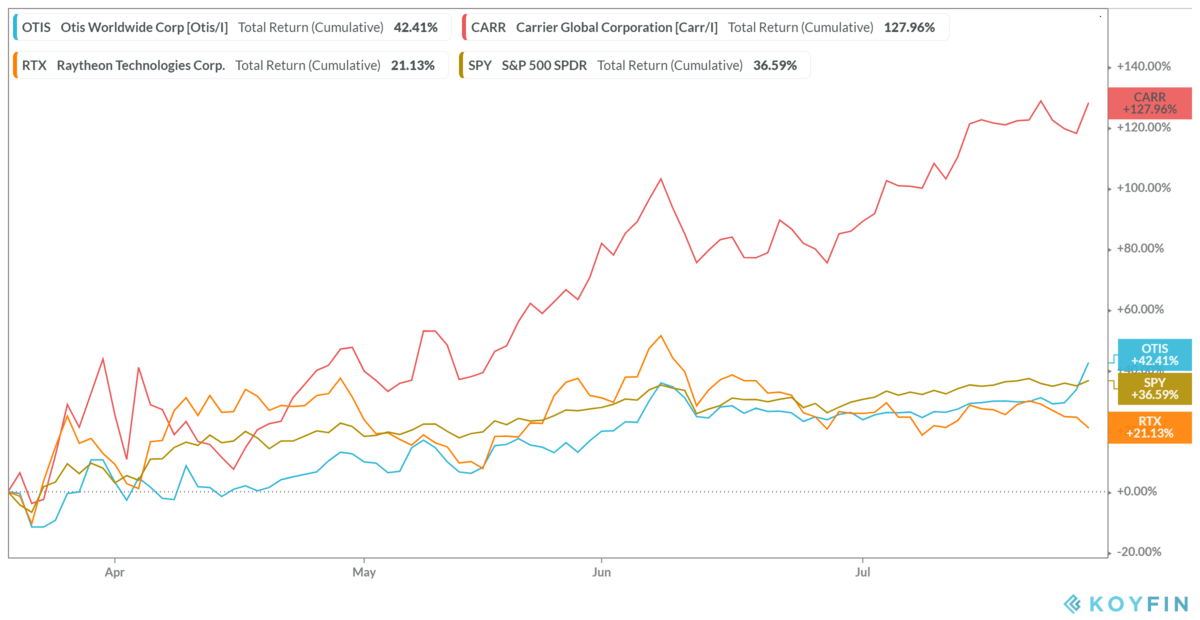

Al final el spin off con narrow moat (Carrier) ha sido mucho mas rentable que los negocios con wide moat (Raytheon y Otis)

It’s very difficult todo esto

Al final el spin off con narrow moat (Carrier) ha sido mucho mas rentable que los negocios con wide moat (Raytheon y Otis)

It’s very difficult todo esto