Rio Tinto vuelve a las ganancias con la recuperación de las materias primas, su programa de control de gastos y mejoras en la eficiecia.

Beneficio neto de 2016: 4.620 millones de dólares (2015 pérdida de 866 millones de dólares).

Aún así, los analistas habían previsto un beneficio de 5.180 millones de dólares.

Dividendo anunciado: 1,70 $

Recompra de acciones previstas en 2017: 500 millones de dólares.

Subidita guapa que lleva Rio Tinto, cerca de máximos históricos… uno de los “aciertos” de la OCU, pongo entrecomillado porque deshicieron parte de su posición a precios inferiores aunque la mantenían en consejo de compra, básicamente por una cuestión de diversificación y riesgos. Yo mantuve y además era una de mis posiciones importantes.

Hará pronto 2 años desde que cargué fuerte y llevo una plusvalía del 40% más dividendos cobrados un 7% de lo invertido, no tengo pensado vender por el momento… me parece incluso más difícil que comprar… pero sea dicho, ojalá todas las operaciones fueran así.

De todo este tiempo he aprendido una lección, el factor tiempo siempre es muy importante y aunque a todos nos guste que la acción se dispare justo después de comprarla, lo “normal” o esperable, es que sea un proceso de 2-3 años. Mientras tanto los ricos dividendos hacen más dulce la espera.

De mi suscripción a la OCU he aprendido también que suelen acertar bastante con los consejos de compra, pero casi nunca con el timming… por lo que siempre que cambian de consejo espero cierto tiempo hasta que la acción toque suelo… (incluso en sus comentarios la OCU ya lo dice, puede que la acción baje todavía más…)

¿Cómo la veis para entrar ahora? llevo tiempo queriendo entrar, y aún tiene recomendación de compra en la OCU. Pero ha subido tanto que no sé si aún tendrá buen margen…

Buenas tardes.

Con las últimas bajadas se está poniendo interesante para hacer una primera compra.

A estos niveles según Investing.com tiene un PER 6,22 y un dividendo 5,54%

Habrá que seguirla de cerca con el tema del Brexit…

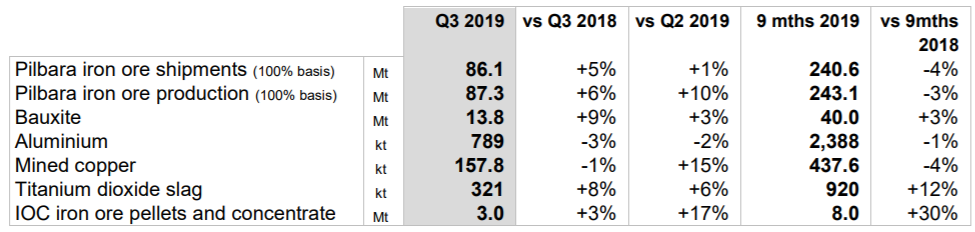

Pilbara iron ore shipments of 86.1 million tonnes (100% basis) in the third quarter were 5% higher

than the third quarter of 2018. Pilbara iron ore production of 87.3 million tonnes (100% basis) was

6% higher than the third quarter of 2018 and 10% higher than the previous quarter, reflecting a

good recovery from the operational and weather challenges experienced earlier in the year.

Third quarter bauxite production and shipments to third parties were 9% and 23% higher,

respectively, than the same period of 2018. Bauxite production from non-managed Joint Ventures

was lower than planned year to date.

Aluminium production of 0.8 million tonnes was 3% lower than the third quarter of 2018, primarily

reflecting a preventive safety shutdown at one of the three pot-lines at ISAL in Iceland and earlier than planned pot relining at Kitimat in British Columbia, Canada.

Mined copper production of 158 thousand tonnes was 1% lower than the third quarter of 2018, but 15% higher than the second quarter, reflecting higher grades at Kennecott and improved throughput at Escondida.

At the Oyu Tolgoi underground project, the primary production shaft (shaft 2) remains on track for

commissioning this month. Since July 2019, we have completed key infrastructure, including the

central heating plant, the shaft 2 jaw crusher system and the surface discharge conveyor. Work

continues on the mine re-design.

Titanium dioxide slag production of 321 thousand tonnes was 8% higher than the third quarter of

2018, reflecting a continued improvement in operational performance and the restart of furnaces in 2019.

Third quarter production at Iron Ore Company of Canada was 3% higher than the corresponding

quarter of 2018 and 17% higher than the previous quarter, reflecting a return to normal operating

conditions following the flooding incident which impacted June.

Guidance is unchanged, with the exception of bauxite production, which has been revised to

around 54 million tonnes (previously 56 to 59 million tonnes), and alumina production, which has

been revised to around 7.7 million tonnes (previously 8.1 to 8.4 million tonnes).

On 25 September 2019, Rio Tinto announced the signing of a Memorandum of Understanding with China Baowu Steel Group and Tsinghua University to develop and implement new methods to reduce carbon emissions and improve environmental performance across the steel value chain.

Third quarter exploration and evaluation spend was $177 million, 62% higher than the same period of 2018, primarily reflecting increased activity on advanced projects.

Strong safety performance in 2019, with no fatalities and a slightly improved all injury frequency rate, coming from a strong base. Continued improvement in prevention of catastrophic events through a step-change in process safety management.

$14.9 billion operating cash flow was 26% higher than 2018 and $9.2 billion free cash flow was 31% higher than 2018. Both are presented after $0.9 billion tax paid in 2019 relating to the 2018 coking coal disposals.

$5.5 billion capital expenditure was consistent with 2018. In late 2019, we announced the approval of two further investments, at Greater Tom Price (iron ore, $0.8 billion) and Kennecott (copper, $1.5 billion).

$21.2 billion underlying EBITDA was 17% above 2018, primarily driven by higher iron ore prices, with an underlying EBITDA margin7 of 47%.

$10.4 billion underlying earnings were 18% above 2018. Taking exclusions into account, net earnings of $8.0 billion were 41% lower than 2018, mainly reflecting $1.7 billion8 of impairments in 2019, primarily the Oyu Tolgoi underground project, consistent with our 2019 interim results, and the Yarwun alumina refinery. This compared with $4.0 billion of gains on disposals in 2018.

Strong balance sheet with net debt4 of $3.7 billion, a rise of $3.9 billion, mainly reflected $11.9 billion of cash returns to shareholders in 2019 through dividends and share buy-backs, and a $1.2 billion non-cash increase from the implementation of IFRS 16 “Leases”, partly offset by free cash flow of $9.2 billion.

$7.2 billion full-year dividend, equivalent to 443 US cents per share and 70% of underlying earnings, includes $3.7 billion record final ordinary dividend (231 US cents per share) declared today.

¿Alguien sabe a que se deben las ultimas subidas? No encuentro noticias relevantes más allá del Brexit.

La verdad es que lleva un tiempo dandome muchas alegrias pero no acabo de entender el porqué.

.

.