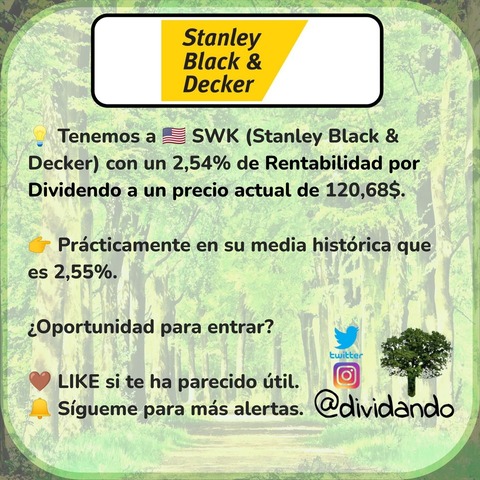

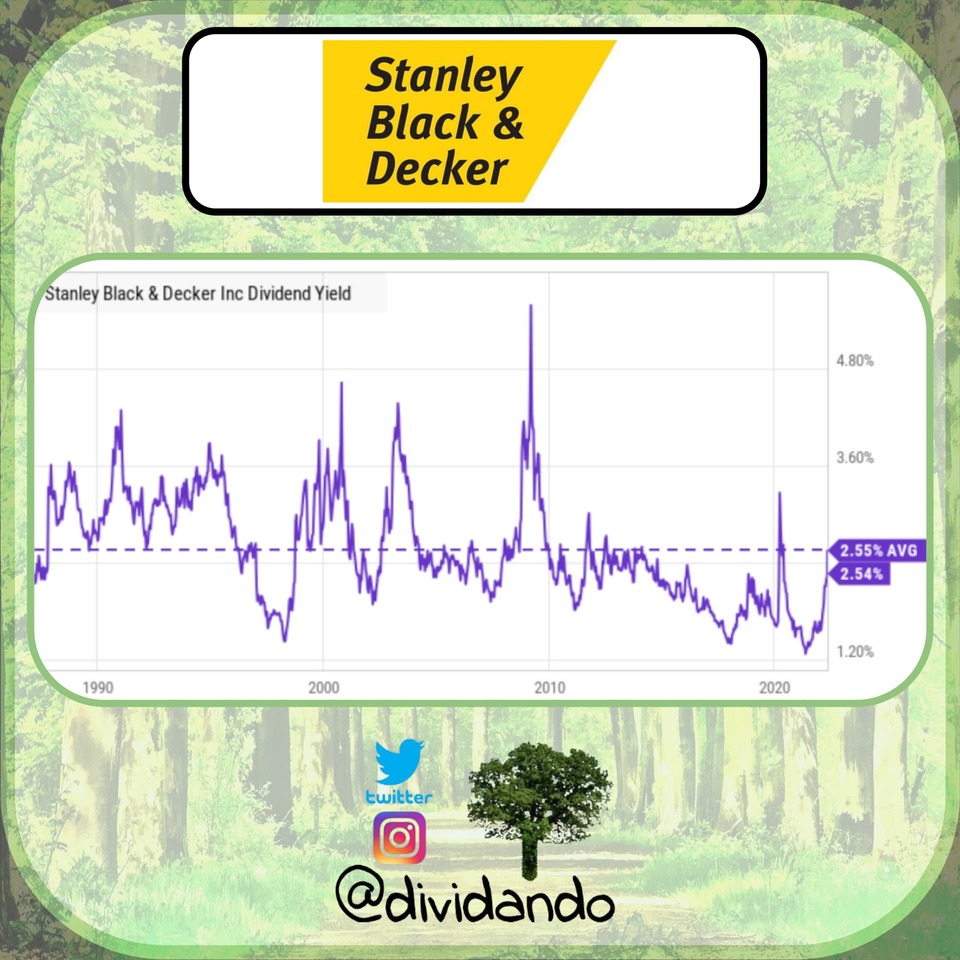

Rentabilidad algo baja, del 1.85% a cotización actual, pero 51 años incrementando dividendos con crecimientos medios (DGR1=6,60%, DGR3=6,40%, DGR5=5,40% y DGR10=7,40%)

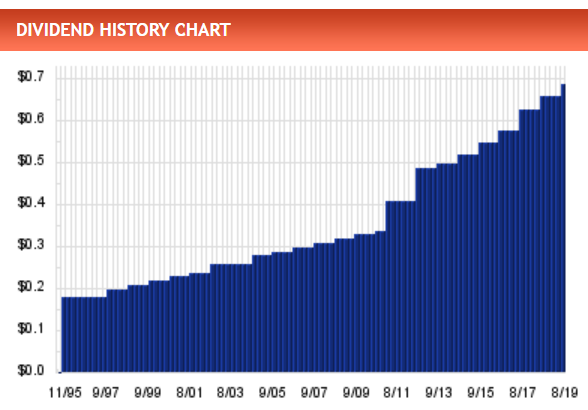

Siempre en subida aunque dió un pequeño respiro a final de 2018, que daba un 2.5% de RPD.

3Q’19 Revenues Totaled $3.6 Billion, Up 4% Versus Prior Year, Driven By Organic Growth And Acquisitions

Operating Margin Rate Was 13.3%; Excluding Charges Operating Margin Rate Was 14.5%, Flat Versus Prior Year While Overcoming $90 Million Of External Headwinds

3Q’19 Diluted GAAP EPS Was $1.53; Excluding Charges, 3Q’19 Diluted EPS Was $2.13

Announcing New Cost Reduction Program Expected To Deliver $200 Million In Annual Cost Savings

Revising 2019 Full Year Diluted GAAP EPS Guidance Range To $6.50 - $6.60 From $7.50 - $7.70 And Adjusted EPS Guidance Range To $8.35 - $8.45 From $8.50 - $8.70

3Q’19 Key Points:

Net sales for the quarter were $3.6 billion, up 4% versus prior year, as positive contributions from volume (+3%), acquisitions (+3%) and price (+1%) more than offset currency (-2%) and divestitures (-1%).

The gross margin rate for the quarter was 34.1%. Excluding charges, the gross margin rate for the quarter was 34.3%, down 120 basis points versus prior year as volume leverage, productivity and price were more than offset by tariffs and foreign exchange.

SG&A expenses were 20.8% of sales. Excluding charges, SG&A expenses were 19.8% of sales compared to 21.0% in 3Q’18, reflecting continued disciplined cost management.

The tax rate was 20.1%. Excluding charges, the tax rate was 21.5% versus 19.5% in 3Q’18.

Average diluted shares outstanding for the quarter were 150.6 million, consistent with the prior year.

Working capital turns for the quarter were 5.9, up 0.2 turns versus prior year.

2019 Outlook & Cost Reduction Program

Management is revising its 2019 EPS outlook to $6.50 - $6.60 from $7.50 - $7.70 on a GAAP basis primarily due to restructuring charges associated with the cost reduction program announced today, in addition to the factors below.

The Company is reducing its adjusted EPS range to $8.35 - $8.45 from $8.50 - $8.70 and reiterating its free cash flow conversion estimate of approximately 85% - 90%.

The cost reduction program is currently being implemented and is expected to deliver $200 million in annual cost savings with an approximate pre-tax restructuring charge of $150 million expected to be recognized primarily in 2019.

Full Year Revenues Totaled $14.4 Billion, Up 3% Versus Prior Year, With 3% Organic Growth

Full Year Operating Margin Rate Was 12.2%; Excluding Charges, Full Year Operating Margin Rate Was 13.5%, Relatively Consistent Versus Prior Year Despite $445 Million In External Headwinds

Full Year Diluted GAAP EPS Was $6.35; Excluding Charges, Full Year Diluted EPS Was $8.40, Up 3% Versus Prior Year

Full Year Free Cash Flow Was $1.1 Billion, 113% Of Net Income

4Q’19 Revenues Totaled $3.7 Billion, Up 2% Versus Prior Year

4Q’19 Operating Margin Rate Was 11.8%; Excluding Charges 4Q’19 Operating Margin Rate Was 13.6%, Up 30 Basis Points Versus Prior Year

4Q’19 Diluted GAAP EPS Was $1.32; Excluding Charges, 4Q’19 Diluted EPS Was $2.18

Expect 2020 Full Year Diluted GAAP EPS Of $8.05 To $8.35; Adjusted EPS Of $8.80 - $9.00; 2020 Free Cash Flow Conversion To Approximate 90%-100%

Pues con las rentabilidades que está dando actualmente me subo al carro de SWK y abro posición en esta empresa. La marca es la marca y a largo creo que se seguirán utilizando estas herramientas.

Lleva mas de un 35% de caida desde los resultados de febrero, no es demasiado?. Con la presumible subida de dividendo que le toca es posible que supere el 3% de rendimiento. Es toda una aristócrata, oportunidad?.

Yo abrí posición con 10 acciones a 118$. No sé si me precipité pero bueno, estaba en torno al 2,60% de rentabilidad y siendo el empreson que es no me la jugué a que por unos dólares se me escapara

Sigue a lo suyo, desangrándose. Mas del 50% de caída en un año y es toda una aristócrata del dividendo. Dividendo ya superior al 3% y con la subida de este año a la vuelta de la esquina. No acabo de entender semejante caída.

No hace mucho leí una recomendación para no entrar de momento. El caso es que ni sé donde lo leí ni el motivo concreto pero sí, en el rádar está…

Saludos

Me sorprende lo poco en boca que está esta dividend king. 54 años incrementando el dividendo, con una RPD actual del 3,70%, con un payout de entre el 40-60%.

La cotización ha caído más de un 50% desde máximos, ahora mismo si excluimos el pico de marzo 2020 está en mínimos de unos 7 años:

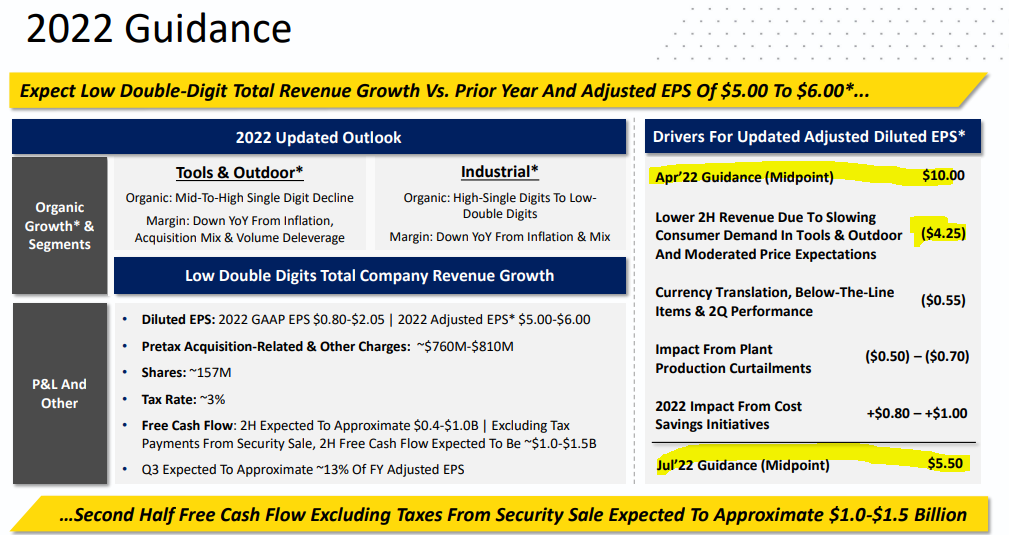

Todo esto es debido a la ralentización de la demanda. Según la propia empresa ha pasado de prever en abril 10$ de EPS para todo 2022 a 5.50$ en Julio:

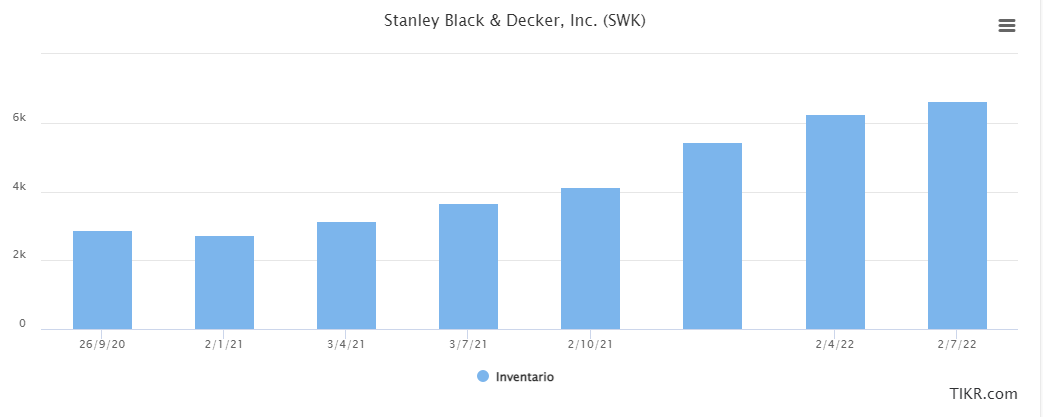

El Viernes estuve cerca de entrar, en la presentación de resultados parece que el principal problema son los inventarios, problema temporal según ellos.

Por lo demás, parece tener la deuda controlada (aunque leyendo comentarios en SA no lo veo tan claro), y payout en torno al 30%. Los dividendos suben en los últimos años un 5-6 anual.

Es posible que entre en los próximos días si la cotización se acerca a los 90$

Yo entré el viernes en 95$.

Tiene 90 puntos de seguridad en SSD y la revisaron en junio, aunque la deuda es un poco alta.

No me parece una empresa core de una cartera pero al ser un dividend king la meto en cartera.

Un saludo.

Supongo que ayuda el hecho de no tener seguimiento en M*

Además tiene Narrow moat que aunque algunos digan que algunas narrow moat son mejor que las wide moat la realidad y la experiencia nos dice que no es así.

Dudo que SWK sea la primera posición en ninguna cartera DGI por lo que el interés en la misma es bajo.

También esta en mínimos VFC y casi nadie habla de ella por los mismos motivos.