¿Pero por qué la gente se tira detrás de una acción que recorta dividendos?

Si es la señal clara de que la tienes que sacar de tu mente

¿Pero por qué la gente se tira detrás de una acción que recorta dividendos?

Si es la señal clara de que la tienes que sacar de tu mente

Yo soy muy taliban con el recorte de dividendos, puedo entender que alguien se quede las acciones que recortan el dividendo por aquello del Do Nothing pero ¿comprar una que ya lo ha recortado? Es clarísima señal de que el negocio va mal y esperan que vaya mal en los próximos años.

En España o Europa no se puede ser tan exquisito pero en USA, ¡será por buenas empresas que suben el dividendo durante decadas!

Siempre puede haber mas recortes,

Están adoptando una política de control de deuda.

Si recuperan nivel de ventas de sus marcas y beneficios medios pasados, lo normal es que el dividendo actual sea 100% sostenible y pagable.

Yo la veo bien para largo plazo…

En momentos como estos es cuando puedes adquirir gangas o trampas de valor…

Las cosas de Mister Market.

![]() con algo de suerte igual toca los 15$

con algo de suerte igual toca los 15$

he leído bien??? 510 títulos??? (y encima compra periódica)

Veo que en este foro se maneja pasta de la buena. ![]()

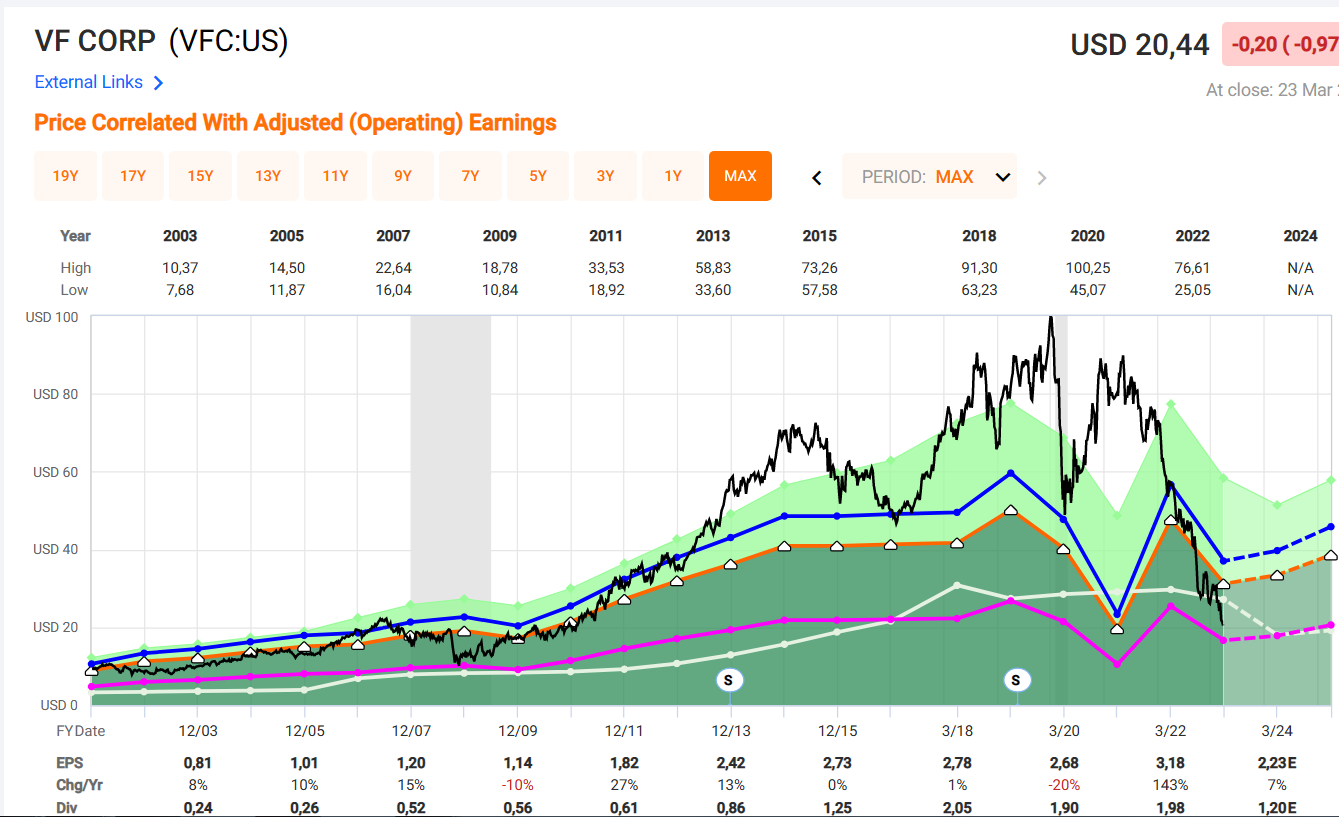

Como hablamos en días pasados VFC recortó dividendo para adoptar una política de control de deuda y llevar mejor los malos tiempos futuros.

A precios actuales no tiene mala pinta el negocio.

BPA 2016: 3$

BPA 2017: 2,57$

BPA 2018:3,6$

BPA 2019:3,35$

BPA 2020: 1,13$ (Covid)

BPA 2021 :3$

BPA 2022: 2,39$

Si cogemos los peores años de esta serie;2017,2020,2022.Sale BPA medio de 2,03$.con estos datos comprando a PER 10 nos sale rango de precios 20$ PER 15= 30$.

No estamos comprando caro… no es una ganga pero tampoco es caro.

Hola, acabo de comprar unas cuantas, así que ya podéis empezar a compraros Vans, y plumas North Face como locos…

actualmente junto con linea directa mi peor inversión en bolsa…la llevo cerca de 40 dolares de media…pero aún sigo confiando en que recupere, veo poder de marca…crucemos los dedos

Si te sirve de consuelo no estás solo tú en esa situación ![]()

Desde mi punto de vista tiene unas marcas muy potentes y si desde el management son capaces de encuazar la situación a largo plazo quizás no siga siendo tu peor inversión

Con lo de hoy creo que se puede dar por alcanzada la proyección técnica que comenté el pasado mes de diciembre. El desarrollo que lleva invita a pensar en la posibilidad de que pueda dilatar la zona, pero en teoría poco a poco debería poder verse algún indicio de que desde dicha zona pueda comenzar a gestarse un cambio en la tendencia, si no un giro total en la misma si al menos comenzar a asentarse en espera de poder intentar algo más. La inercia que trae es muy fuerte y lo suyo sería, para el que tenga intención de hacer algo, esperar al menos a que se pueda apreciar algún detalle técnico que invite a asumir el riesgo. Lo ideal sería en un tiempo prudencial poder encontrar alguna divergencia que apoye ese posible escenario de reacción.

Es imposible encontrar una certeza absoluta pero las probabilidades de que, entendiendo el concepto de zonal, el castigo comience a menguar pueden ser reales.

Un saludo.

Pero lo de hoy es por los resultados de Foot Locker ¿no?

Parece que la gente ha dejado de comprar zapatos para ahorrar y poder pillarse el nuevo Iphone con chip de Nvidia

Ya verás cuando les llegue el Iphone a casa y quieran salir a la calle a vacilar y se den cuenta de que están descalzos o en el mejor de los casos con un calzado muy lejos de lo que la ocasión requeriría ![]()

Si no calzas unas Vash, digo Vans, no estás en la onda.

No he sido capaz de resistir la tentación y he añadido unas pocas a 19 ![]()

Nunca viene mal recordar lo que pasó

→

→

Downgraded on May 26, 2023

In this week’s much-anticipated earnings release, VF Corp reported profits roughly in line with expectations and issued full-year earnings guidance that met analyst estimates. However, this wasn’t enough to reverse the stock’s continued decline.

Management’s guidance hinges on the current highly promotional environment, spurred by heavy inventory levels across the industry, returning to healthier levels by the fall.

This debatable assumption would help the company’s margins rebound as VF Corp works on right-sizing its own inventory, which finished the quarter up 62% versus last year (albeit an improvement over the prior quarter’s 101% increase).

We don’t expect the apparel maker’s profitability to remain subdued forever. But the timing of an earnings recovery is especially important with the firm’s net debt to EBITDA leverage ratio sitting well above management’s target level near 2.0x.

Source: Simply Safe Dividends

VF Corp expects deleveraging to take place over the next couple of years. But progress could stall if the anticipated rebound in profits gets pushed out due to softening demand.

Unfortunately, this scenario is looking more likely.

In recent weeks, major retailers have warned of a pullback in consumer spending on discretionary items like clothing and footwear as inflation and higher interest rates continue to squeeze pocketbooks.

Here are some relevant excerpts from earnings calls this month (emphasis added):

Foot Locker:

We had forecasted a pickup in growth in April as we move past the tax refund drag and benefited from a more favorable launch calendar during the month. And while trends did improve, they did not improve nearly to the extent we expected and that weakness has continued into May.

As a result, we increased our promotional activity late in the first quarter and more so in the second quarter, and we expect that level of promotional activity to continue through the balance of the year… we now expect a sharper decline in both sales and earnings this year due to steeper macro headwinds.

Target:

…we continue to benefit from traffic and sales growth in our frequency categories, food and beverage, household essentials and Beauty, which helped to offset softer year-on-year sales in our more discretionaryhome, apparel and hardlines categories… total sales were strongest in February, began decelerating in March and softened further near the end of April.

Walmart:

…below the surface, we continue to see signs that customers remain choiceful, particularly in discretionary categories. In Q1, we saw a nearly 360 basis point shift in U.S. sales mix from general merchandise to grocery and health and wellness. To benchmark, the magnitude of this shift exceeds the 330 basis points of category mix shift we experienced in all of last year.

If apparel demand weakens and leverage remains higher than expected later this year, would VF Corp consider further reducing its dividend to prioritize debt repayment?

While the company’s projected payout ratio near 50% provides some comfort, this scenario probably cannot be ruled out.

Given the growing headwinds from the shift in consumer spending and the continued turnaround struggles at skateboard shoemaker Vans (32% of revenue; sales fell 12% last quarter), we are downgrading VF Corp’s Dividend Safety Score from Safe to Borderline Safe.

That said, while VF Corp’s dividend appears to have a somewhat thinner margin of safety, the stock looks cheap if you believe Vans, The North Face (31% of revenue; sales grew 17% last year), and Timberland (15%; sales up 4% last year) will remain relevant.

Source: Simply Safe Dividends

While it has been a painful couple of years, to say the least, we plan to maintain our position in VF Corp in our Long-term Dividend Growth portfolio with a belief that the main challenges facing the company are either fixable or transitory.

VF Corp hit a perfect storm of headwinds in the last few years. Covid-related supply chain issues led to excessive inventory orders just as more demand shifted from goods to services. The underperformance of Vans (hard to say how much of that is Covid-related noise) and balance sheet pressure from buying Supreme in 2020 haven’t helped either.

And now, the looming prospects of a recession appear to be further denting demand for discretionary goods, putting management’s full-year guidance at risk.

While acknowledging that fashion trends are hard to forecast, we don’t have a negative long-term outlook for key brands like North Face and Vans, which have performed well for several decades, sell thousands of different products, compete in very large markets, and serve consumers globally.

Should brand performance weaken further (outside of uncontrollable events like a recession), we would likely exit. For now, we are willing to give VF Corp another 12 to 18 months to demonstrate an ability to return to profitable growth.

¿Para que necesito ropa y comida teniendo un iphone y una RTX 4000?