Los Cazadividendos

Walgreens Boots Alliance (WBA)

Empresas

Estados Unidos

fortknox

14 Octubre, 2021 18:16

155

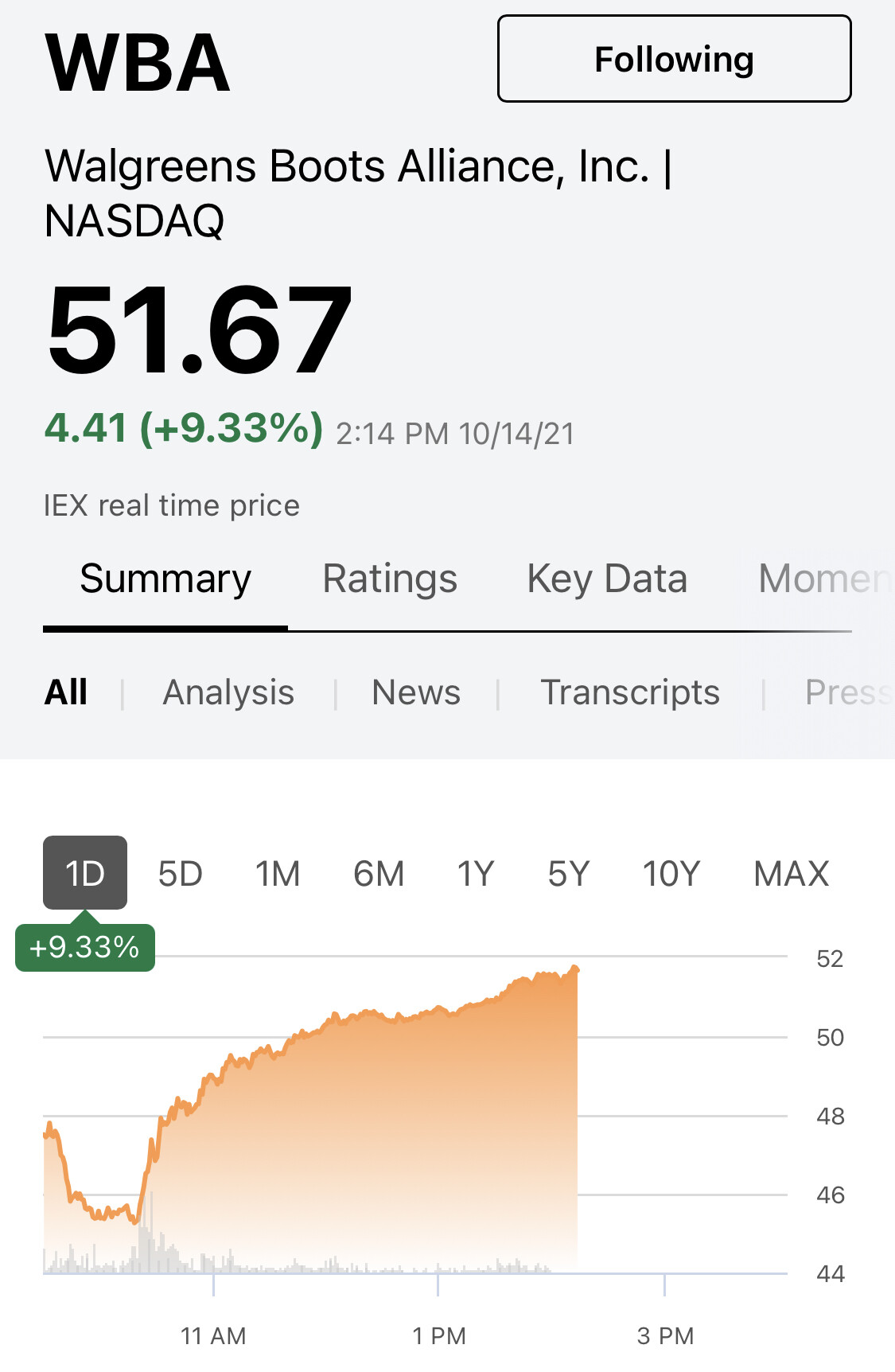

imagen

1125×1724 160 KB

2 Me gusta

mostrar publicación en el tema