Wells Fargo fue sancionado en septiembre con 174 millones por malas prácticas entre 2011 y 2015.

Y Warren Buffet reduce posición para eludir los requisitos que tendría que cumplir por superar el 10% del accionariado del banco. Lo explica Dividendo Rentable:

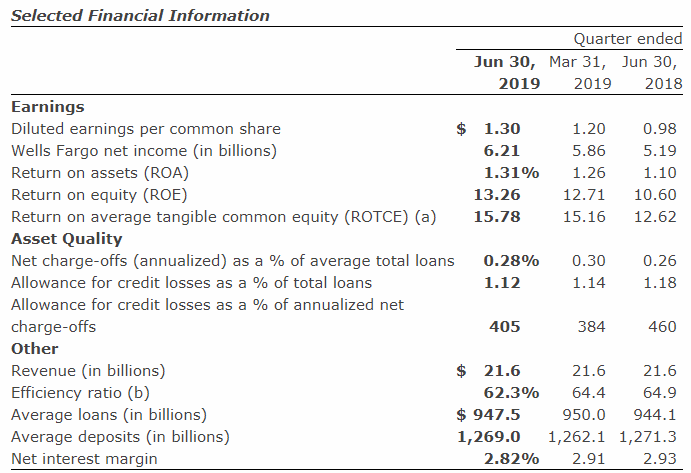

Net income of $4.6 billion, compared with $6.0 billion in third quarter 2018

Diluted earnings per share (EPS) of $0.92, compared with $1.13

Third quarter 2019 included a $1.6 billion, or $(0.35) per share, discrete litigation accrual (not tax-deductible) for previously disclosed retail sales practices matters, and a $1.1 billion, or $0.20 per share, gain from the previously announced sale of our Institutional Retirement and Trust (IRT) business

Revenue of $22.0 billion, up from $21.9 billion

Net interest income of $11.6 billion, down $947 million

Noninterest income of $10.4 billion, up $1.0 billion

Noninterest expense of $15.2 billion, up $1.4 billion

Average deposits of $1.3 trillion, up $25.0 billion

Average loans of $949.8 billion, up $10.3 billion

Credit quality:

Provision expense of $695 million, up $115 million from third quarter 2018

Net charge-offs of $645 million, down $35 million

Net charge-offs of 0.27% of average loans (annualized), down from 0.29%

Reserve build1 of $50 million, compared with a $100 million reserve release1 in third quarter 2018

Nonaccrual loans of $5.5 billion, down $1.2 billion, or 17%

Strong capital position while returning more capital to shareholders:

Common Equity Tier 1 ratio (fully phased-in) of 11.6%2

Returned $9.0 billion to shareholders through common stock dividends and net share repurchases, up 2% from $8.9 billion in third quarter 2018

Quarterly common stock dividend of $0.51 per share, up 19% from $0.43 per share

Period-end common shares outstanding down 442.4 million shares, or 9%

Third quarter 2019 included the partial redemption of our Series K Preferred Stock, which reduced diluted EPS by $0.05 per share, while third quarter 2018 included the redemption of our Series J Preferred Stock, which reduced diluted EPS by $0.03 per share

Hay un reportaje en Netflix de Wells Fargo.

La serie de documentales se llama “Dirty Money”, no recuerdo si está en la primera o segunda temporada, pero es interesante.

No quiero ganarme haters por aquí, sólo que si no lo habéis visto, veáis un nuevo punto de vista.

The Federal Reserve has released the results of its annual stress tests. Our key takeaway is that the banking system appears to be well-capitalized, even in scenarios that are materially worse than the typical “severely adverse” scenario that the Fed normally uses. This supports our overall thesis, which is that the banks are much better positioned and will be much harder to break this time around. Our base case has been that most banks will be able to maintain their dividends, and we think the latest disclosures support this thesis as well. Based on the released results, we calculate that a select few banks may need to cut their dividends after third-quarter results, including CapitalOne (we think a 100% cut), Wells Fargo (we think less than 100%), and Comerica (we think less than 100%); however, we think the majority will be fine. Banks will have to resubmit their capital plans later in the year, and the Fed has said it will continue to monitor the economic downturn as it develops, so this will remain an active situation with more updates and changes to come. There is still a high degree of uncertainty around the future economic state and what future credit costs will be, but we are generally encouraged by today’s results

Y no solo recorte de dividendos, también prohiben temporalmente la recompra de acciones:

<<During the third quarter, no share repurchases will be permitted. In recent years, share repurchases have represented approximately 70 percent of shareholder payouts from large banks. The Board is also capping dividend payments to the amount paid in the second quarter and is further limiting them to an amount based on recent earnings.>>

Deben sobrar dedos de la mano para contar las empresas que recompran acciones con la cotización hundida y potencialmente por debajo de su valor teórico.

¿No será porque igualmente no se llegaría a la cotización objetivo para cobrar los bonus? Supongo que no, que es para tener un colchón porque vienen baches y hay que mantener el dividendo.

Que yo sepa no han recortado el dividendo, han prohibido las recompras de acciones y las subidas hasta que la economía se recupere. Pero en principio pueden seguir pagando el dividendo actual siempre que las cuentas les den para ello.