El libro es de Miguel de Juan y su título no es muy innovador: “EL inversor español inteligente”. Es un ex de banca de inversión (a la que pone a caldo) y que se ha montado su propio fondo de inversión. Un buen tío.

Añado que, para mi, es de los gestores españoles mas honestos.

Soy partícipe del Argos y nos mantiene informados vía whassap y mail de todos los movimientos del fondo. Si alguno se anima a invertir en el Argos, mandadle un mail y dadle vuestro movil ![]()

Aquí un novato que se ha leído este hilo por primera vez y no puede estar mas agradecido por la cantidad de información aportada!

3 Me gusta

A la hora de tomar decisiones de compra, creo que entran en juego más factores que el Yield y el crecimiento de éste. El yield puede subir, como puede bajar, así que la seguridad del dividendo es algo muy importante. Si me encuentro ante dudas entre dos empresas, obviamente me fijaré en la rentabilidad que puedo esperar, pero la viabilidad futura de la empresa es, para mi, mucho más importante. Después, hay empresas como 3M o Disney que pagan dividendos bajos, (3m ahora menos bajos porque está bajando considerablemente de precio) que hacen recompras de acciones que pueden ir del 1% al 4% anual. Aunque el dinero se pague de forma directa como ocurre con un dividendo, el Buyback Yield (como algunos le llaman) se recibe de forma indirecta mediante el aumento del precio de la acción, seguridad en el dividendo y posteriores splits.

A lo largo de los años, alguien que compre ahora McDonald’s con un Yield del 2% puede esperar que cuando hayan recomprado el 50% de sus propias acciones obtenga el 4% de la inversión inicial, y si vas reinvirtiendo los dividendos puedes terminar por duplicar tus acciones, con lo que te puedes acabar viendo con un 8% anual, sumando además el Buyback Yield que te ofrecen, y suma y sigue. Todo esto hablando de una empresa tan segura como lo es McDonald’s y sin tener en cuenta el crecimiento de la empresa y la inflación que hará que sus productos suban de precio.

Pero en definitiva, si se recompran acciones aumenta el porcentaje de la empresa que posees, y eso se traduce en mejor dividendo y más seguridad sobre éste.

7 Me gusta

Interesante el tema de que es lo mejor.

En mi caso he adoptado las dos posiciones en mi cartera, tengo valores de un tipo y de otro.

Por que no aprovecharse de las cosas buenas de los dos tipos de acciones. Ademas, tal como pienso yo, una accion no tiene por que estar toda la vida en una cartera, se puede comprar para un tiempo determinado.

3 Me gusta

Yo también creo que lo mejor es llevar una mezcla de los dos y así he compuesto mi cartera. Me vale que la media ponderada de ambos valores (rpd inicial y crecimiento) sea la que necesito.

Eso sí, tengo un suelo de la rpd del 2% Por debajo, necesitas crecimientos demasiado grandes y prolongados, lo cual es una rareza históricamente (en esta web se ven cosas muy interesantes como que solo una compañía, MDT, ha aumentando el dividendo al menos un 7% anual durante los últimos 25 años)

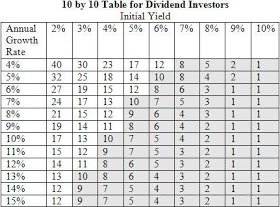

Creo que ya la subí en otro hilo, pero a mi esta tabla me gusta mucho pues muestra el número de años necesarios para conseguir un YoC del 10% con diferentes combinaciones de rpd y crecimiento. El objetivo del ejercicio (conseguirlo en menos de 10 años) no es posible con la rpd del 2% ni para los crecimientos más altos (que como digo, a su vez son utópicos en esos plazos)

16 Me gusta

¡Gracias! Muy interesante la página esa de crecimientos de dividendo

1 me gusta

Me parece muy ilustrativa, porque tendemos a echar cuentas tomando la rpd actual y el crecimiento de dividendo de los últimos 3 ó 5 años y proyectándolo indefinidamente en el tiempo. Y la realidad nos muestra que para crecimientos altos, eso no es posible. O tan residual que encontrarlo es una lotería.

4 Me gusta

Destacar que en esta tabla no se contempla la re-inversión de dividendos. Esta tabla es del artículo 10 by 10: A New Way to Look at Dividend Yield and Growth | Seeking Alpha

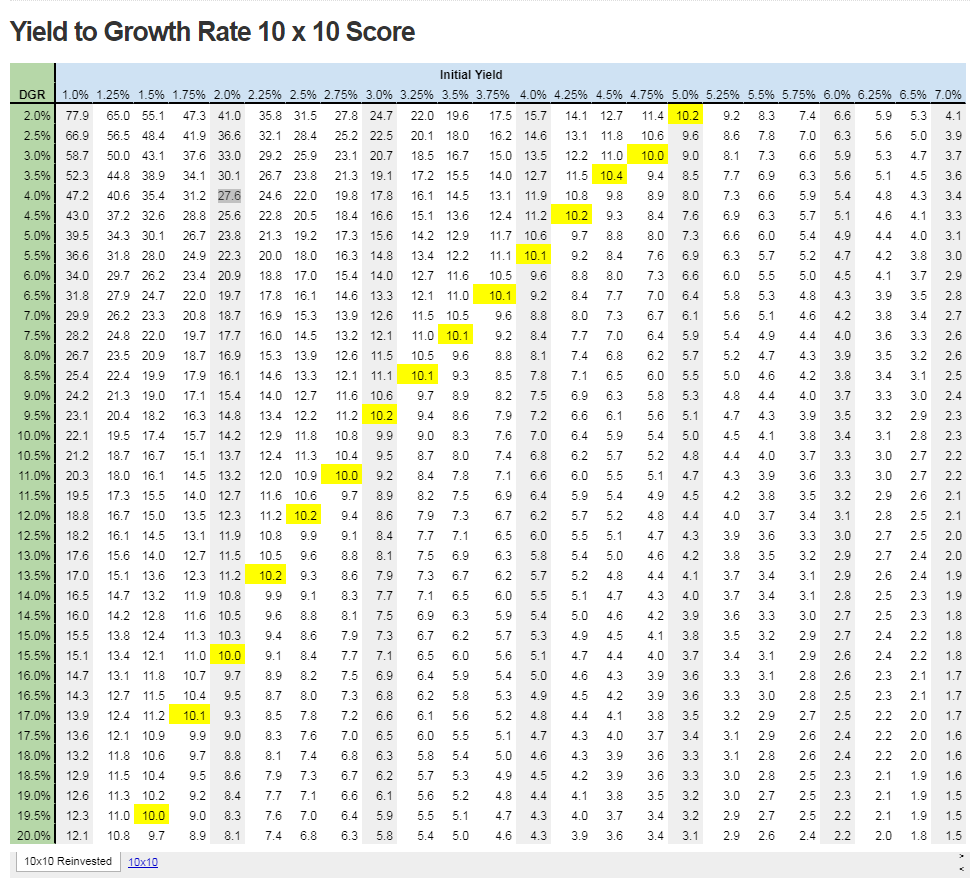

En esta otra web, https://www.dividendgeek.com/10x10-score/, se contempla esta misma tabla contando la re-inversión de dividendos:

19 Me gusta

Muchas gracias por compartir el artículo @lluis. Personalmente soy un fan de empresas como Markel, sin dividendo o Apple, futura Arisócrata del dividendo. Tampoco le hago ascos a Altria, puesto que todavía no soy lo suficientemente rico como para dejar de invertir en tabaco.

2 Me gusta

Recientemente ha habido un debate en el blog DGI de S.A. donde participa mucha gente de la que pongo comentarios aquí.

El tema es: Inicio de una cartera para una persona joven (pongamos 24 años).

Las recomendaciones han sido muy variadas, pero se puede centrar en dos aspectos:

A) Inicio con empresas de calidad que tengan yield relativamente alto aunque crecimiento de dividendo lento (clásico ejemplo T). Con los dividendos que dan se puede iniciar posiciones en empresas de crecimiento.

B) Inicio con empresas de bajo yield, pero alto crecimiento de dividendo. Llegado un momento y debido a la teórica alta revalorización, se puede recortar algunas posiciones para conseguir dinero y comprar empresas de mayor dividendo.

Por supuesto. Como en el Whisky, siempre existe la opción blend:

C) 2/3 Empresas alto dividendo, 1/3 crecimiento.

Todo esto ya se ha tratado en este magnífico hilo. Tan sólo pongo la breve introducción para añadir los comentarios copiados de la conversación:

Disculpad el tocho. No es realmente necesario leerlo, pero me ha gustado para refrescar el tema.

"CHOWDER

In your case, and mine, we started out with that foundation of what we used to refer to around here as core holdings.

Most of the people around here talking about buying growth are the ones that are on schedule to meet their income needs or have achieved them already. Those people I don’t care about. I’m trying to focus on those who are behind schedule. I’m trying to insure they retire on time with more than enough to help eliminate anxiety at a time when they no longer have a paycheck to fall back on.

As to the young people, I have been very consistent with my advice. Establish that foundation of quality higher paying dividend companies, track where you are as to whether you are on schedule or not, and if you are, then go for growth.

In my son’s portfolio I know where his portfolio needs to be at the end of every year for the next 30 years to achieve the long term objective we established 10 years ago. Once he got ahead of schedule, I started buying some growth type companies like DG, MA and V as opposed to continually adding to T, D and O. He has a mixture of income and growth but I insured he was ahead of schedule on income first. Without those compounding dividends, he can’t hit his long term objective.

Every year I establish a new short term objective based on how the portfolio has performed while always keeping the long term objective in mind.

Two years ago he was almost 3 years ahead of schedule and I decided to start adding more growth type companies, but as I did, the income margin of safety was dropping, so this year I’m looking at yield again. I started adding to those higher dividend paying companies again to help insure he stayed ahead of schedule on income. Next year, if all goes according to plan this year, I may start adding potential high growth companies that don’t pay a dividend, but I will put that off if he isn’t on schedule, if he doesn’t have that margin of safety.

You can’t always have growth and income at the same time. They often times go in opposite directions and thus I need to adjust and determine which has priority for this year. I can’t do anything about last year or next year. I can only control this year, so it’s important to me to know where the portfolio should be this year in order to stay on track.

Further on up in the comment stream, someone stated they were going to open a new portfolio for a 24 year old and start with 8 companies. My suggestion was to start with at least 5 income type companies and then 3 growth if they wanted some growth. So I’m not oblivious to growth. I’m opposed to not having clearly defined goals so one knows from year to year whether they’re on schedule or not and what I need to do as I look forward.

Several years ago I said the narrative around here was going to change and it did. I knew that the bull market would help people like you and me be on schedule to achieve our goals. I knew you, I and others would adjust to that and invest in companies or other types of assets we didn’t invest in initially.

We like to think it’s because we are smarter investors having learned from our mistakes, and although that may be true, the catalyst for any success we’ve had so far was a raging bull market that insured we stayed on schedule. If we were in a lost decade type of environment, our attitudes about how we invest would be different. I learned that after having been through several recessions so I learned what works regardless of what the market does and still allows me to be ahead of schedule. And that’s what I share here on SA for those who need to be on schedule.

Looking forward is fine, but where does one stand now? That determines how they should invest under the current market conditions."

MIGUEL LORCA

"You have been very consistent with this advice, however, it doesn’t make it correct. If you look at the growth companies you added to your son’s portfolio, you would have been better off just investing in them to begin with.

What evidence do you have that buying high-yield first (D, T, VZ, etc) produces better results than first buying stocks like DG, MA, V, ABT, NEE, COST, UNP, SYK?"

CHOWDER

"Every one of those companies is in the young folk portfolio and all of them wouldn’t be at this time if I didn’t have the help of having dividends to buy them. Those dividends came from companies like T, VZ and O.

I’m keeping it simple here hoping you can finally relate to something that you have lacked the ability to understand."

SEEKSQUALITY

"That’s a bit disingenuous… You could have easily chosen to purchase Miguel’s list of stocks with the original contributions, then trimmed a portion of the gains to buy companies like T, VZ, and O. You CHOSE to follow the path you did. It wasn’t forced upon you.

Now I’m definitely not saying that you were wrong to choose the path you did! But there are always alternatives, some better and some worse. It was your choice to secure the income first, then build growth off that."

CHOWDER

"Now why in the world would I want to trim positions in a young person’s portfolio, only to have to buy them back at higher prices later?

That doesn’t compute with me. In fact, I’m surprised you even said that as I assumed from all the table pounding I have done about building positions of size, not trimming them and making them smaller."

SEEKSQUALITY

"if your initial purchases were low dividend growth stocks, you wouldn’t really have an alternative! They wouldn’t be throwing off enough income to purchase the other stocks you want.

Your choices are dictated by your management style, which is as it should be! They are nonetheless choices."

MIGUEL LORCA a CHOWDER

“To me you are stating things without any evidence. Your son doesn’t actually need 54 holdings and your remaining positions would likely be quite large if you had started off with lower-yield, high growth stocks like the ones your son currently has. UNP, COST, SYK, ABT, etc have all grown much faster than T, for example. Had you started with them they would be positions of size.”

SEEKSQUALITY a MIGUEL LORCA

"the growth dividend stocks CAN be purchased first, however they won’t throw off enough income to fund new positions. If you want to expand the number of holdings in the portfolio, then you need to either come up with new money or start trimming.

After about ten years, the growth of a portfolio is greater than any new money you might add. It becomes increasingly difficult to fund a new full position from new contributions. For example, the amount that I recently invested in ADP is twice as much as my last five years of retirement account contributions COMBINED. So I fund new positions by trimming/eliminating old ones.

Chowder doesn’t like to “sell winners”, and selling losers won’t get you far unless you make a lot of mistakes, so this approach doesn’t work for him. He needs that dividend income to fund new positions.

Alternatively he might have begun with small positions in every stock he wants to own rather than beginning with a subset and building out from that? But when you are beginning with $5k or $10k at a time, it is hard to sliver that 30 different ways. And only recently have we enjoyed $0 commissions.

Finally, if you want a young investor to buy into the concept of DGI, it can be helpful to have meaningful dividends thrown off by the portfolio from the start. I believe Chowder’s approach is a psychologically easier one to manage."

CHOWDER

"the growth dividend stocks CAN be purchased first, however they won’t throw off enough income to fund new positions. If you want to expand the number of holdings in the portfolio, then you need to either come up with new money or start trimming.

After about ten years, the growth of a portfolio is greater than any new money you might add. It becomes increasingly difficult to fund a new full position from new contributions. For example, the amount that I recently invested in ADP is twice as much as my last five years of retirement account contributions COMBINED. So I fund new positions by trimming/eliminating old ones.

Chowder doesn’t like to “sell winners”, and selling losers won’t get you far unless you make a lot of mistakes, so this approach doesn’t work for him. He needs that dividend income to fund new positions.

Alternatively he might have begun with small positions in every stock he wants to own rather than beginning with a subset and building out from that? But when you are beginning with $5k or $10k at a time, it is hard to sliver that 30 different ways. And only recently have we enjoyed $0 commissions.

Finally, if you want a young investor to buy into the concept of DGI, it can be helpful to have meaningful dividends thrown off by the portfolio from the start. I believe Chowder’s approach is a psychologically easier one to manage."

MIGUEL LORCA a SEEKSQUALITY

"I’m pretty sure know that isn’t correct, right? Some of the stocks I mentioned were: DG, MA, V, ABT, NEE, COST, UNP, SYK, HD. They are just examples. Pick the DGR stocks you prefer.

Who cares if they immediately produce enough income to expand the number of holdings in the portfolio? ALL of them produce dividends. Are you saying after owning stocks like NEE, UNP, HD etc that they wouldn’t be producing enough dividends after 30 yrs, or, shall we say 5 yrs before retirement to start buying some higher yielders. What’s the rush?

Put differently, if it’s OK for Chowder to reinvent his portfolio into 14 C-corp and 8 CEFs during (or at the beginning of) his retirement why can’t his son trim some positions like V, MA, COST (super low yield) at retirement in order to tack on some 4-5% high utilities, REITs and even CEFs, if needed?"

SEEKSQUALITY a MIGUEL LORCA

" let’s say you started with those nine stocks in 2000 (and they include a few that are definitely not lower-yield). They’ll do as well as any. Pool the dividends, let the original purchases ride. How much cash do you have after ten years? Is that enough to add two new full positions, equal in size to the other nine? Or are those new positions you add permanently smaller than the original nine?

I’m pretty sure I’m correct in what I am saying. If it doesn’t sound like it makes sense to you, then you aren’t understanding what I am trying to say (which wouldn’t be the first time).

“why can’t his son trim some positions…”

If you read what I said above, I specifically stated that he COULD trim some positions. He’ll just have trouble building new full positions from dividends and new cash if he chooses not to trim. They grow too fast and don’t throw off enough dividends for the numbers to work on that.

You could, of course, accept that the higher-yield positions will be much smaller than the original positions. That isn’t an unreasonable position either, but you end up with a very different portfolio than what Chowder is developing, with a much higher proportion of growth stocks and a lower proportion of income stocks."

CHOWDER

"By purchasing those companies you listed first, the amount of cash to invest initially, as is the case for a lot of young people, too damn small to take advantage of the growth you are now chasing. In order for growth to maximize its benefits, you need to own it in size.

When a young person can’t invest a lot of money initially, the best way to generate more cash so you can purchase those growth companies is through dividends. My son owns every company you mentioned but wouldn’t have them all if he didn’t have the extra cash to invest that dividends provide.

Trimming might buy him a few shares, but why in the world would I want to trim a $2K sized position? That’s what I would have had to do to own the companies he now owns if I didn’t build his dividend cash flows.

As to retirement, where you may have to change strategies, as did I, my son won’t have to. It doesn’t matter to me whether you think it’s no big deal to buy income later. My son won’t have to, and he won’t have to chase growth either. He is smarter than you and I in that he started much earlier in life."

MIGUEL LORCA

" A young investor does NOT have to buy in size. All they need are regular investments over a long time period and they will turn into size.

$5k invested in the growth stocks your son owns and kept for 20 yrs would now equal over $900k today with NO additional money added. In your son’s case he would have continued adding to those positions and other growth stocks.

Case in point: “In order for growth to maximize its benefits, you need to own it in size.” I’m pretty sure this is incorrect. Small purchases held for 30-40 yrs can turn into a massive amount of money.

In addition, there shouldn’t be anything wrong with pointing out that a young investor doesn’t have to start with a foundation of high yield first. They can start off with growth and very likely do better by the time they are ready to retire. How is this too personal to bring up? Is this me saying, "I INSIST your son switch to my method? We are simply talking about how a younger investor might successfully get to retirement age. "

8 Me gusta

Tengo la impresión de que entre que te situas en el trabajo, creas o no una familia y te das cuenta de que es esto de la inversión a largo plazo con dividendos ya estás en la cuarentena.

Con estas edades el planteamiento puro de dividendos bajos con crecimiento alto es perfecto para tus herederos. Tengo mis dudas de si se puede conseguir la IF en 20-25 años siguiendo este modelo. Porque si se consigue al llegar a los 80 mi opinion es que el sacrificio no vale la pena.

8 Me gusta

En mi opinión, si se siente como un sacrificio, nunca vale la pena. Personalmente, disfruto ahorrando e invirtiendo y creo que a alguien que no lo vea así le resultará muy complicado llegar o acercarse a una hipotética independencia financiera.

9 Me gusta

Estoy de acuerdo. Sacrificio no es la palabra sino esfuerzo

6 Me gusta

Totalmente de acuerdo que la edad es un factor crítico a la hora de decidir qué factor predomina en la composición de la cartera de acciones. El interés compuesto necesita tiempo (a partir de 10 años ya se hace evidente su acción).

El caso que puse se refería en cuanto a la creación para una persona de 24 años y de ahí surge la conversación.

La mayoría de los cuarentones que estaos por aquí hemos pasado por varias fases, una de ellas centrada en el dividendo puro y muchas veces cuanto más alto mejor (desconocimiento de muchas cosas). Al final acabamos con una mezcla de ambos tipos de acciones y dando mucha importancia a la calidad.

Si desde el principio ya tuviésemos eso claro (como parece sucede en USA por los blogs que se leen), otro gallo nos habría cantado.

Así que, un equilibrio entre ambos tipos es el resultado.

Me pareció interesante resucitar el hilo, quizá porque voy dándole vueltas a cómo orientar la inversión de mis hijos. Ambos con acciones del SAN gracias a una decisión tomada en época de analfabetismo inversor. Ahora sus acciones (y las mias) valen un escupitajo. Son jóvenes y ambos tienen el Amundi world. Pero estoy valorando si vendo a grandes pérdidas y todo al fondo o creo cuenta en broker barato y todo a dos empresas de crecimiento. Esto último da pereza porque obliga a papeleo y más control que de normal.

Si tuvieseis que elegir dos empresas únicamente, de crecimiento. Y darles 15-20 años. ¿cuáles elegirírais para vuestros hijos?. Empezamos con 3-4k total.

4 Me gusta

Mi opinión desde el estómago: Nestlé y PG. No se si de crecimiento o de confianza.

1 me gusta

Con respecto al debate low yield+high growth vs high yield+low growth, yo creo que lo mejor es diversificar también en ese aspecto.

En mi caso empecé por la calle del medio, ~3% y crecimientos decentes, y luego fui diverisificando, añadiéndole picante tanto con yields por arriba como por abajo (porque un yield bajo también es añadirle picante, aunque de una especia diferente, pero picante  ).

).

@luisg , 2 son muy pocas xD, pero si me dejas tirarme a la piscina con 3, ordenadas según la escala debatida en este hilo, otro día en persona debatimos más xD:

- UNH, 1.74% yield, 10 años incrementando, 27 años sin reducir, payout ~30%, incremento medio últimos 5 años 24%, últimos 20 años un 40%, crecimiento EPS últimos años > 10% anual

- ADP, 2.52% yield, 45 años de incrementos, payout ~60%, incremento medio dividendo últimos 5 años 13%, últimos 20 un 12%, crecimiento EPS últimos años > 10% anual

- JNJ, no necesita presentación y permíteme incluirla aún como crecimiento, 2.93% yield, 57 años de incrementos, payout ~50%, incremento medio últimos 5 años 6%, últimos 20 años 10%, crecimiento EPS últimos años > 6%

Yo diría que con esas tres ahora mismo me parece que no pagas sobreprecio y están incluídos 3-4 sectores, porque ADP es realmente industrial-tecnológica y JNJ podría considerarse hasta salud-consumer staples; UNH es más pure play salud. Pagas lo que valen. A esas 3 me encantaría incluirte Microsoft pero no puedo justificar su 1% de yield.

Y con esas 3 también diversificas un poco en low yield+high growth vs high yield+low growth.

12 Me gusta

Raúl, muy buenas recomendaciones.

Pero ya sabes que los nanos son < 10 años. La vida y el interés compuesto por delante. Dije 2 empresas porque no es lo mismo compra de 1000 que 1500€, teniendo en cuenta comisiones, a menos que sea en Degiro (IB cobraría 120$/año mantenimiento y Charles Schawb queda descartado por requerimiento 25k).

En IB podría habilitar la compra en fracciones en hacer DCA durante 1-2 años…

Así pues, sin tener en cuenta yield… yo pensaba meter MSFT. UNH genial. ¿Esas AMZN de Juanjo?. ¿AAPL? Ya hemos hablado en alguna reunión (y tú dominas el tema), que las tecnológicas actuales pueden ser las consumer staple del próximo futuro con sus pagos recurrentes…

La próxima quedada hablamos ![]()

1 me gusta

Indexado al SP500 y otro indexado a Asia ex-japan. Mis dos centavos.

Apple capitaliza más que todo el PIB de España. FAANG capitaliza más que todo el PIB alemán (hablo de PIB, no del Dax, ojo). Pueden ser las nuevas staples o no. Blackberry y Nokia también eran fantásticas en su día. Si entramos en una recesión profunda veremos cuánta gente sigue comprando un móvil nuevo de 1000 euros todos los años; o en cuanto se reduce el gasto en publicidad por parte de las grandes marcas (FB, Google). Netflix nunca me ha gustado. Amazon me parece la mejor de todas, pero siempre queda la duda de si ya llegamos tarde y quedaremos con cara de idiotas en unos años.

5 Me gusta

Yo iria a lo mas seguro, J&J y PG y un par de crecimiento, GOOG y AMZN

5 Me gusta