El tema es que el dividendo es altísimo, y parece que es pagable por ahora.

Una posición grande lo veo arriesgado quizás, pero un 1% de la cartera, pensando a largo plazo (a partir de 10 años), no debe ser mala opción.

Lo de que cada vez se fuma menos llevo mucho tiempo oyéndolo, pero parece que solo son momentos puntuales:

Y encima le sumamos la moda del vapeo y que parece que la marihuana se va a legalizar.

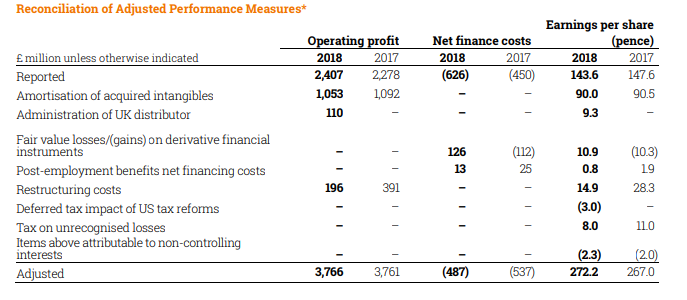

La diferencia entre el ajustado y el reportado creo recordar que venia por un tema de una pérdida contable ( unadepreciación de un negocio que tenian valorado a X y que finamente asumen que vale Y, y se dan la pérdida) No estoy seguro, pero creo recordar que era por un tema de estos.

Mi duda viene más por si cuando hablan de que el BPA se mantiene estable, se mantendrá estable respecto al BPA reportado (el que vale) o al ajustado.

Me da a mi que del ajustado van a hacer como que no se acuerdan, por que en las cuentas semestrales ya reportaron cerca de 70p, que va bastante en línea con los 140p anuales del año pasado.

Yo personalmente, beneficios ajustados no los considero nunca. Hay que cojer siempre lo que te reportan en CCAA,.

Yo de momento la valoraría a PER 12, asumiendo que no tengo capacidad para analizar más ni ver valor más allá

Los intangibles, siempre los malditos intangibles. Esto supongo es una compra que pagaron cara en su día. Pero por mucho que quieran remarcar que es un gasto no recurrente, la pérdida está ahí? Tienes el link de donde sacas esto? Hay algun párrafo de explicación?

@anbax Ese cuadro también lo ví, pero no lo entiendo. ¿Porque consideran la amortización como algo a sumar al beneficio para llegar al beneficio ajustado?. Además no es que metan un poquito del total de la amortización, es que la calzan prácticamente al 100% (en 2018 fueron 1.266m y meten 1.053m). Siento como si me tratasen de colar el ratio EBITDA (vale quitando impuestos e intereses) en lugar del benecio neto. No es lo mismo.

Sí lo entiendo si se tratase de una amortización extraordinaria en one-shot, pero parece que es recurrente año a año… por otra parte no bajan en el balance los intangibles y esperaría que si se trata de reconocer un muerto puntual en el armario los intangibles bajasen… pero no lo veo.

Sí es cierto que sale una amortización desmesurada en relación a la competencia, pero no entiendo porqué.

Los beneficios proforma hay que tomarlos siempre con escepticismo.

En “El inversor Inteligente” dice Graham: “Si desea leer una brillante sátira sobre cómo sería la vida diaria si justificásemos nuestro comportamiento del modo en que las empresas ajustan sus beneficios declarados consulte “My Pro Forma Life” de Rob Walker, en (”… un reciente almuerzo después de una sesión de gimnasio compuesto por un chuletón en en Smith & Wollenksy y tres chupitos de bourbon son tratados como gasto no recurrente. ¡Nunca lo volveré a hacer!").

En situaciones así, es recomendable acudir al estado de flujos de cash-flow. Le he echado un vistazo por encima y lo he visto robusto y sin pegas.

Acquired goodwill and the distorting effect of amortisation

After re-joining the stock market as an independent company in 1996 (following ten-years as a wholly owned subsidiary of Hanson Trust PLC), Imperial Tobacco spent more than £17 billion acquiring other companies en route to becoming the world’s fourth largest tobacco manufacturer. This acquisition spree ended in 2008, coinciding with the Great Financial Crisis. Since then, further acquisitions have totalled less than £5 billion.

What does all this have to do with misleading reported earnings? Well, as with most acquisitions, the price paid for these companies far exceeded their tangible assets. After each acquisition, the premium paid above tangible assets ended up on Imperial’s balance sheet as accounting goodwill, an intangible rather than tangible asset. That’s relevant because intangible assets are, for the most part, depreciated over anywhere from three to 30 years, just like tangible assets (although for intangibles it’s called amortisation). Eventually, Imperial Brands ended up with more than £20 billion of intangible assets and that requires a lot of amortisation.

Amortisation is a non-cash expense which reduces the company’s profits by varying amounts, but it currently runs close to £1 billion per year. That’s a big recurring non-cash expense, especially for a company where pre-amortisation profits are only around £3.5 billion. The result of so much amortisation is that the company’s dividend is often uncovered by reported earnings, but only because of a huge non-cash expense largely caused by acquisitions made more than a decade ago.

To get a better view of Imperial Brands, I think (and following in the footsteps of a certain Mr Buffett) a more accurate picture of a company’s operating performance is given when amortisation is excluded from earnings. There are various ways to do this, but one simple approach is to look at free cash flow instead of reported earnings.

Free cash flow is an attempt to measure the amount of cash generated by the company’s business operations (known as net operating cash flow), minus any cash reinvested into the business to pay for new capital assets such as property, plant and equipment (otherwise known as capital expenses or capex).

Like any performance measure, free cash flow isn’t perfect, but it does exclude Imperial’s huge non-cash amortisation of goodwill expense. It also replaces the non-cash expense of deprecation (which reflects the reduction in historic value of old capital assets) with the cash expense of capex (which reflects the current cost of new capital assets). Replacing depreciation with capex is generally a conservative move because capex is usually a larger expense than depreciation. That’s because a) growing companies will usually be investing more in fixed assets today than they were five or ten years ago and b) the cost of replacing assets goes up over time thanks to inflation.

More generally, free cash flow is probably a better measure than reported earnings if you’re looking for reliable dividend payments.

Growing free cash flow easily covers a progressive dividend

Unlike reported earnings which are down over the last decade, Imperial Brands’ free cash flow per share has increased by more than 30%, with an annualised growth rate of 4%. That’s better than the company’s 1.6% annualised revenue growth and reflects increasing margins thanks to the company’s focus on cost cutting and higher margin products.

More importantly, free cash flow has covered the dividend every year, with an average free cash flow dividend cover of 1.9. Free cash flow dividend cover has been decreasing, though, going from around 2.5 a decade ago to 1.5 today. The reason is that management has seen fit to increase the dividend by an average of almost 11% per year for a decade. This makes for happy shareholders, but it isn’t sustainable. At some point in the next few years the dividend’s growth rate will have to be reduced if it’s to remain well-covered by free cash flows.

Gracias @anbax con eso me quito veo que mis dos mosqueos son en realidad dos problemas diferentes.

Este primero se elimina con una valoración por EV/EBITDA por la que IMB sale muy barata en relación a sus comparables. El otro mosqueo es por el FCF y lo del inventario que supongo sí tiene que ver con el Blu.

De momento no compro. Esperaré a ver cuentas anuales y me fijaré en FCF y que ocurre con el Working capital. Seguramente estaré perdiéndome una buena oportunidad.

Pues yo he comprado unas cuantas. He cambiado alcohol (ABI) por tabaco y no soy fumador.

A ver si se comporta bien a medio plazo. La verdad es que veo el sector para largo plazo.

Lo que si veo es a mucha gente joven fumando pese a todas las advertencias.

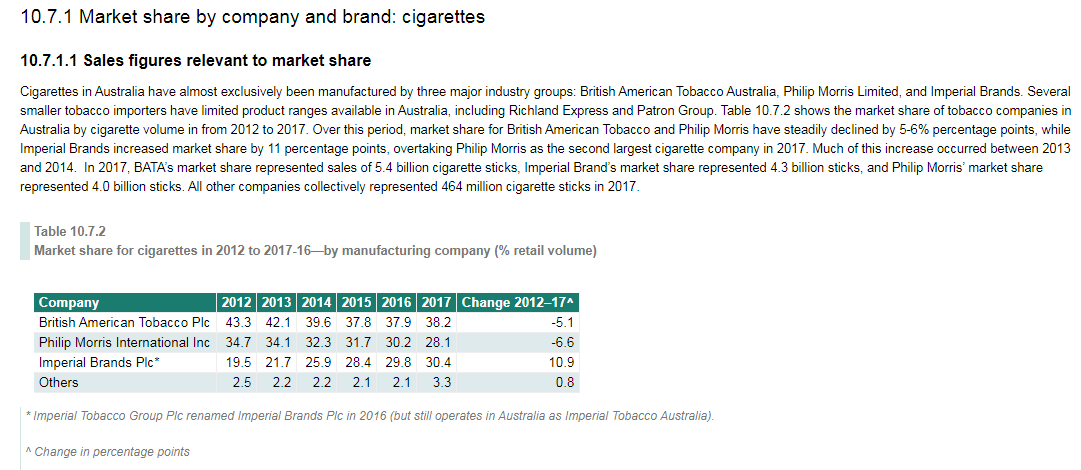

Se puede ver como IMB ha superado a PM en unos pocos años. Australia es conocido por ser uno de los paises mas restrictivos con su legislacion sobre el tabaco. Pioneros en el plain packaging e implementando grandes subidas de impuestos. ¿Y que ha pasado? Pues que la empresa que se supone de mas calidad PM ha perdido el segundo puesto en cuota de mercado frente a la empresa de menos calidad IMB. Y es que las marcas premium (PM) sufren mas cuando se ataca al tabaco frente a las marcas mas baratas (IMB). Asi que IMB podria sobrevivir a un apocalipsis tabaquil mejor que PM cosa que las valoraciones actuales ni consideran.

Tambien puede ser que PM haya decidido “pasar” de los australianos y concentrarse en mercados mas rentables.

A mí me preocuparía un poco más la sostenibilidad del dividendo en IMB si el resto de tabaqueras tuvieran RPDs del 4-5%, sugiriendo que el problema es intrínseco y exclusivo de IMB.

Pero es que MO a 40 USD está con una RPD del 8.4%. PM en sus mínimos creo que daba más de un 7%, BATS me imagino que otro tanto. El sector está de capa caída, aunque es evidente que las mayores dudas parecen estar con IMB.

Imperial Brands Prepares Strategy to Deal With Investors

By David Hellier

27 September 2019, 05:00 BST Updated on 27 September 2019, 08:10 BST

Even before Imperial Brands Plc’s profit warning, the tobacco company was discussing a confidential report that criticizes its presentation of financial information following investor complaints.

The company has become a target of shareholder ire after losing more than half its value since a 2016 peak. Investors and analysts have voiced concerns about Imperial’s earnings calculations and its strategy, including its commitment to small, local brands such as West and Gauloises at a time when many smokers are shifting away from cigarettes.

The report, by financial communications adviser Tulchan, argues for more financial transparency. A spokesman for the tobacco company confirmed the existence of the report and said its recommendations will be taken into account when Imperial reports full-year results Nov. 5. “Tulchan’;s stakeholder audit was welcomed by the board,” he said. Tulchan declined to comment.

Vaping challenges have hurt Imperial Brands shares Imperial is not alone in feeling the effect of a U.S. crackdown on vaping following a mystery illness, but the company suffered a particularly hard blow with its profit warning. The 13% drop in its share price Thursday, which wiped out almost 2.6 billion pounds ($3.2 billion) of market value, heaps more pressure on Chief Executive Officer Allison Cooper.

On Friday the shares fell a further 2.4% in early London trading. Owen Bennett, an analyst at Jefferies, said it’s difficult to get investors interested in buying the stock. “In our previous conversations when expressing our optimism about Imperial, the pushback a number of times has been, ‘Yes, but I can’t get involved as Imperial finds a way to let you down every time,”’ he said in a note.

Chairman’s Departure Chairman Mark Williamson in February announced plans to step down after 18% of shareholders opposed his re-election at the company’s annual general meeting. Earnings growth has ground to a halt as the company has struggled to keep up with rivals expanding in vaping and now faces the backlash from regulators and consumers over new alternatives to cigarettes.

In June, Liberum analyst Nico von Stackelberg slammed Imperial’s earnings calculations, saying the company includes non-operational factors such as gains from asset sales and uses profit as a factor in setting executive bonuses. Von Stackelberg also expressed concerns about Imperial’s limited development in next-generation products and investors’ demands for clearer financial reporting.

The analyst said Imperial is one of the most attractive investment opportunities in consumer staples if only it would revamp its strategy. Imperial also faces competition as it seeks a new chairman to succeed Williamson, as larger rival British American Tobacco Plc is also planning to replace Chairman Richard Burrows.

Hola, muchas gracias @vash y el resto por el debate

Esto me ha dejado un poco confuso. ¿Es cierto que solo se llama amortización al “gasto” de los intangibles y los tangibles tienen otro nombre / otro tratamiento?

Yo pensaba que era amortización en ambos casos (y lo pienso).

Que me perdonen los contables del foro pero a efectos practicos es lo mismo. Aqui lo explican con mas detalle:

Puede decirse que no existe gran diferencia ya que el objetivo tanto de de Depreciación y Amortización es el mismo, de igual manera el procedimiento y su metodología son los mismos. Como mencionamos la depreciación hace referencia exclusivamente a los Activos Fijos y la Amortización hacer referencia a los Bienes Intangibles y diferidos.

Yo diría que la diferencia es que la depreciación es un gasto más real, porque muchas veces son máquinas o camiones o algo físico que tienes que reponer y por tanto cuyo dinero debes iré poniendo año a año (no tanto en Reits)… mientras que en la amortización pueden ser compras de otras empresas en las que difieres en varias años el importe de la compra… como parece ser el caso.

La diferencia entre amortizar y depreciar es la siguiente: Amortizar es, podriamos decir, el caso normal. Por ejemplo, compras una máquina que, según las normas contables, se amortiza en 5 años. Pues cada año te daa como gasto un 20% del total del valor(100/5=20).

Depreciar, por contra, es el caso “extraordinario”. Compras la máquina y al segundo año se te rompe, por lo que, el primer año habrás amortizado un 20% y el segundo año tendrás que depreciar por el valor total de la máquina, es decir el 80% restante.

En el caso de Imperial brands, en qe ha habido compras de negocios, la depreciación se da cuando viene el auditor viene y te dice, oye, este negocio que tienes valorado en 100, en realidad vale 20, por lo que depreciate 80

Gracias por la explicación @jaume. Sólo me queda una duda: el valor de la depreciación, 80 en tu ejemplo, ¿lo fija el auditor o la propia empresa? Parece más lógico que lo haga la propia empresa, ¿no?