Gracias, lo desconocía. Al rico spin-off.

De la noche a la mañana la misma empresa anuncia que va a vender un poquito de una empresa que posee y ya solo por eso vale un 10% más…

El mercado no hay quien lo entienda…

Estoy hasta el gorro de los Spin Off

")

Una charla entorno a Intel, Apple, semiconductores y TSMC.

El resumen que yo he sacado: TSMC lo controla todo.

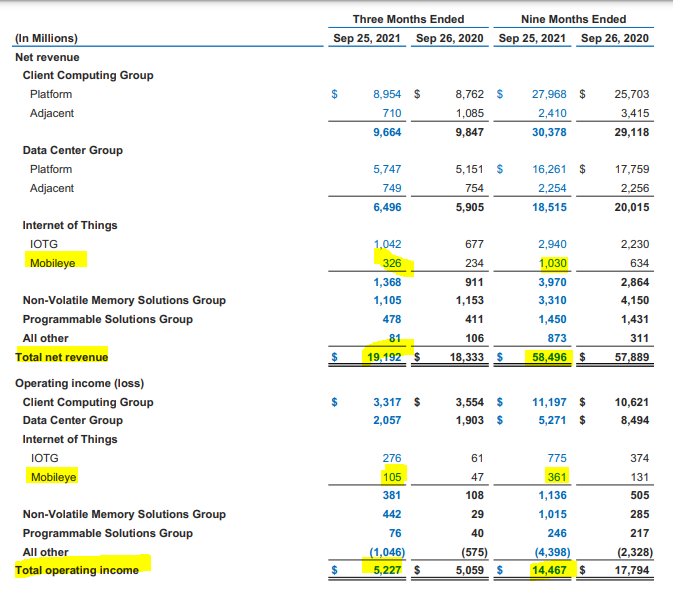

Haciendo unas cuentas rápidas con la última presentación de resultados.

Mobileye representa el 1,75% de las ventas de Intel y aporta el 2-2.5% del beneficio. Eso sí, ambas variables creciendo mucho.

Si damos por bueno la noticia de que va a sacarla a bolsa por 50B$, dado que Intel capitaliza poco más de 200B$ estarían vendiendo Mobileye por el 25% de la capitalización.

Parece que han gustado las especificaciones de los chips de la familia Core para portátiles, así como el anuncio de 22 nuevos CPUs de 12ª generación para equipos de sobremesa.

Parece que Occidente quiere aumentar la producción de semiconductores para disminuír la dependencia de Asia.

Entonces al final no la ponen entre Don Benito y Villanueva de la Serena no? Mecachis…

1000 milloncejos y solo 12 años de espera.

¡Qué gusto que le suban a uno el sueldo esos múltiplos!

Han dado guidance? Ha caído bastante en el after

Intel’s Strong Q4 Results Overshadowed by Soft Q1 Gross Margin Guidance; Shares Remain Undervalued

Intel reported impressive fourth-quarter results, as revenue came in ahead of both guidance and our estimates thanks to PC and data center strength. The firm is dealing with an assortment of headwinds ranging from a resurgent AMD that is pressuring Intel’s CPU market share, Apple’s shift to internal CPUs for its Mac PCs, and the transition from general-purpose computing to accelerated computing that relies on the likes of Nvidia’s GPUs. Nonetheless, we remain positive on Intel’s IDM 2.0 strategy to get its manufacturing back on track and develop a more substantial foundry offering while outsourcing more products to TSMC. Shares fell about 2% after-hours, which we attribute to the soft gross margin outlook for the first quarter.

We are maintaining our $65 fair value estimate for wide-moat Intel, as we think 2022 will be the near-term trough for margins as the firm invests in its future technology roadmap.

Fourth-quarter revenue was up 3% year over year to $20.5 billion, which was about $1.3 billion higher than guidance of $19.2 billion. Client computing group, or CCG, sales grew 5% sequentially, but were down 7% year over year due to a tougher comparison and the ramping down of Apple CPU and iPhone modem businesses. When excluding the divestitures of Intel’s modem and connected home units, full-year CCG sales were up 6% in 2021. Industry-wide component shortages continue to restrict lower-end system sales, whereas commercial, desktop, and higher-end consumer notebooks remain strong. Quarterly desktop and notebook ASPs were up 11% and 14%, respectively, year over year, thanks to this more favorable mix.

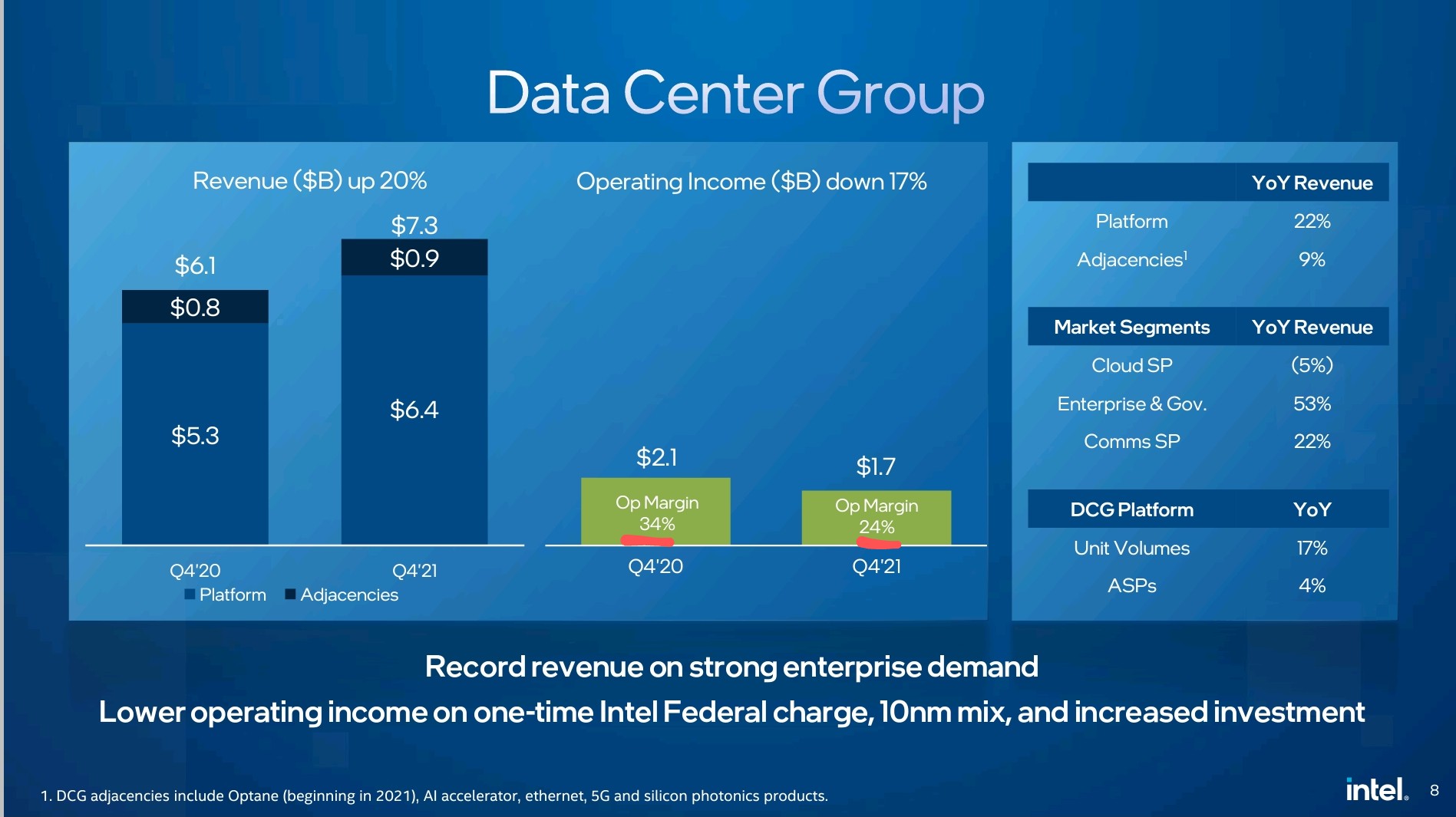

Data center group, or DCG, sales grew 20% year over year due to strong enterprise and government demand as well as Intel’s 10-nm Ice Lake server CPU ramp. Within DCG, enterprise and government sales were up 53% year over year, whereas cloud sales were down 5% year over year. We suspect Intel is both losing share and cutting prices in its cloud segment.

Intel por no perder las buenas costumbres.

Ellos se ponen en la presentación “best year ever” y el mercado los tiene en un -3%…

Pues yo en la presentación la palabra que más leo es “Down”, que no entiendo mucho pero creo que no suele ir asociado a nada positivo…