IBM’s Acquisition of Red Hat & The Modern Tech Stock

The Conservative Income Investor, October 30, 2018

IBM’s Acquisition of Red Hat & The Modern Tech Stock

The Conservative Income Investor, October 30, 2018

Entiendo que han pasado de ser cíclicas a tener un crecimiento sostenido, ya que tienen caja para comprar otras empresas y con margenes muy amplios incluidas las jubilaciones de sus ingenieros.

Yo creo, que la próxima evolución de la humanidad tiene que ser tecnológica y empresas tipo google, apple, IBM, Intel, Microsoft, etc etc, son las que serán la punta de lanza.

Asi lo expresa. En ultimos meses semiconductores han pasado de estar sobrecomprados a sobrevendidos. Hay varios que han caido un 50% o mas.

Texas instruments se ha puesto en radar de muchos.

Ante la ralentizacion sobre el crecimiento de dividendos en sector consumo, la tecnologia (moviles, internet etc…) se ha hecho tan de consumo diario para tantos millones de personas, que empresas como Intel, Qualcomm, Cisco, Apple, IBM, etc… pueden ser un gran complemento a muchas carteras diversificadas

Miraros bien qué hace IBM, actualmente se gana la vida dando servicios y consultoría experta… y luego sus dos puntas de lanza:

Yo no veo que sea una tecnológica que tiene productos que triunfan y que los va mejorando o sacando nuevos, tipo Apple, Microsoft, Google-Youtube, Facebook-Whatsapp-Instagram, Amazon, tampoco tiene un mono- duo-polio en componentes como Cisco, AMD, Intel, Nvidia, Netflix; la veo como una empresa con una estructura gigante que se está re-inventando al estilo HP

La compra de RedHat es una buena noticia y más si parece que no la van a asimilar a su estructura, el precio ha sido alto

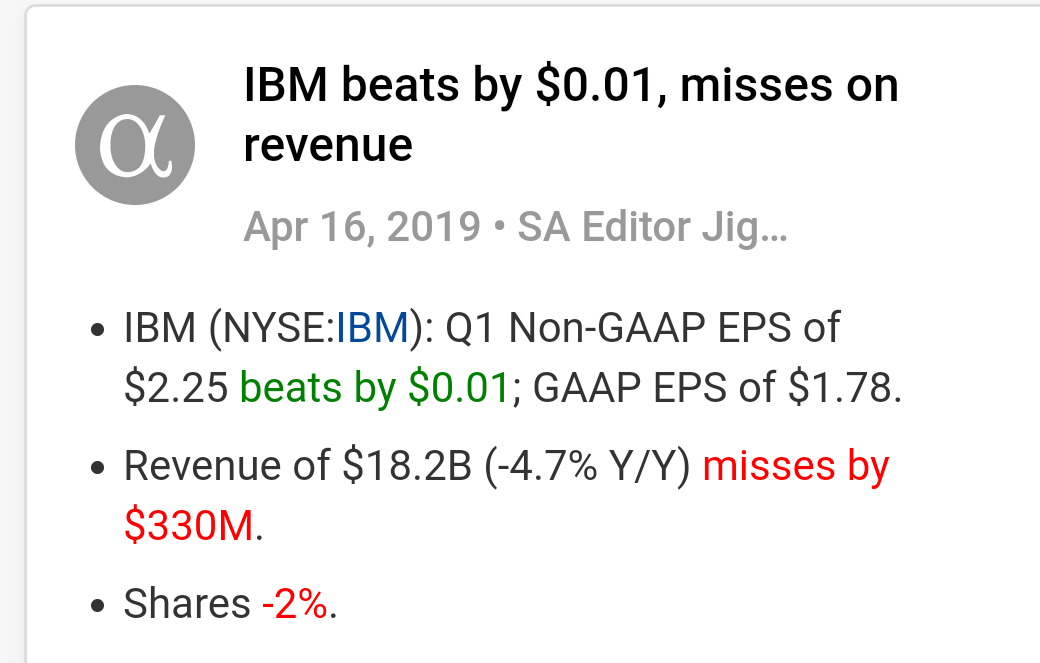

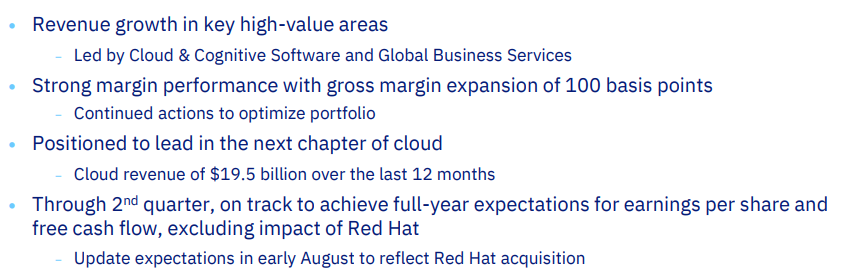

Peores de lo esperado, pero por lo menos parece que empieza a dar resultado la apuesta por el cloud:

Por lo que había leído la apuesta de IBM para los próximos años se sustenta en tres pilares, que no se pueden entender de manera aislada:

También será muy importante ver cómo acaba funcionando la compra de Red Hat…

Sin olvidar su tradicional nicho de Mainframes y Servidores empresariales.

A lo que hay que añadirlos los avances en computación cuántica…

IBM incrementa el dividendo trimestral de 1,57$ a 1,62$

Sigue en recomendación de compra de OCU.

IBM Stock: All Those Cash Dividends

The Conservative Income Investor, May 19, 2019

Between 1978 and 2012, IBM stock delivered returns of at least 12% during every ten-year or greater time frame except for the 1998-2008 and 1999-2009 measuring periods. Up until the past decade or so, it was “the” tech stock. It was the company in the tech industry that survived every change and found itself in the taxable accounts, retirement accounts, trust funds, and charitable accounts of even the most conservative of equity investors. “Big Blue” had survived a century, putting a together a track record of 14.5% annual returns from 1945 until 2012. We are talking about real multi-generational wealth here.

As those same investors know, IBM has been struggling competitively since 2012, as net profits have declined from $16 billion to $12 billion. The blow has been softened somewhat due to IBM repurchasing almost 300 million of its then-existing 1.1 billion shares outstanding in 2012 to bring the total down to the 800 million range today, but ultimately, earnings per share have declined from $14.37 to $13.90 over the past seven years.

But you know what is often neglected? That IBM has paid out $40.26 per share in dividends over that same time frame. For someone who has owned the stock since 2002, the total dividends collected have been 147% of the purchase price. It creates a bizarre disconnect where the investor would see the actual revenues decline, see the online blog articles declaring that IBM is doomed, see the EPS more or less stagnate, but simultaneously have collected his entire investment and then some back in the form of seventeen year’s worth of dividends.

If those dividends were collected as cash and extracted, the initial capital remaining in the form of IBM stock would be “riskless” in the sense that it had already been repaid and now the investor was, in a sense, playing with house money (though I am not too fond of this analogy because it can be used to justify all sorts of irrationality in future decision-making on the heels of past success).

On Christmas Eve, IBM stock fell to $107 per share. Against stabilized profits per share of $13.90, we were looking at a valuation of 7.7x earnings. With dividends of $6.48 per share, we are talking about a yield that briefly crossed 6% a mere five months ago. I’m not saying I would have rather bought IBM over Apple at $146 during this time frame, but I will say that somewhere out there, there is a guy collecting 6% yield-on-cost on his IBM stock who is probably going to collect $35 in total over the next five years on every $100 invested in IBM stock on December 24, 2018.

I know that most of the investor community regards IBM’s impending acquisition of Red Hat as an overpay, and while that is probably right, it is going to be nice for IBM to own something that is earning $3.8 billion in revenues that are rising at 12% currently (and have risen at 20% annually over the past ten years).

Do I think IBM is something that needs to be added to one’s portfolio? No. Would I rather own Alphabet or Apple over the next fifteen years? Of course. But I do not need to own something or regard it as the most attractive investment in order to learn something from it. And the lesson is that these cash cows that spit off cash can continue to generate a whole lot more value for shareholders than what one might expect during an extended period of underwhelming period.

If you are a true buy-and-hold investor, and particularly if you make investments in a taxable account where decades of capital gains would trigger a steep tax bill in the event of selling, you may encounter the situation where you are sitting on $400,000 in IBM stock that cost you $35,000 in the 1980s. I would sit on my rear, collect the $19,280 in dividends, and deploy them elsewhere. A highly appreciated stock position in dividend mode can deliver a lot of cash to shareholders that can act a self-funding device for your other investments.

And lest we forget, IBM is still earning $12 billion in net profits. There are only 37 other companies headquartered in the United States that could say the same thing. For comparison, there is a Starbucks on every corner and Starbucks still only brings in $3.5 billion in profits per year. The investment community writes about IBM like it is an ossified carcass, but the cash still pours into headquarters and then into the pockets of shareholders as dividends.

A legacy IBM position, or that of any stagnant cash generator, is no tragedy. Take the dividends and get your growth elsewhere.

No acabo de entenderlos demasiado bien pero en el premarket cae casi un 2%

Pues al final gustaron que sube un 7%

Parece que vamos saliendo de la larga travesía en el desierto…

Lo de “chutzpah” creo que significa echarle un par de huevos

Ted Fischer (Seeking Alpha):

“It wasn’t an awful earnings report. Would be nice to see an outlook including Red Hat, but I guess no outlook is better than a misleading outlook.

Continued revenue declines. Their healthy business segment is growing at a 5% rate. But that is also their most profitable, so all is good (for now).

You gotta admire the chutzpah of a business that borrows tens of billions of dollars for an aggressive acquisition and THEN borrows another billion to buy back shares. Not sure that is sound cash management practice, but it is definite chutzpah! And contributes to that bottom line “beat””

“If the Red Hat business continues 15% growth, that will be a small boost for the company overall (but a good acquisition). If it spurs other divisions of IBM into growth mode, then IBM stock will take off. If the moribund IBM culture infects Red Hat, then the acquisition will be a complete disaster.”

IBM reports 2019 third-quarter results (16/10/2019)

Third Quarter:

2019 Full-year Expectations:

The paradox with IBM is that all investors know what the problem is. IBM suffers from bad leadership. Ginni Rometty, who has been at the helm for 7 years. During her tenure, the stock has declined by 27% while she has pocketed more than $100 million in salary. A look at Glassdoor shows that only 73% of her staff approved of her job. The CEOs of Microsoft, Salesforce, Google, Cisco, and Intel have an approval rating of 97%, 96%, 92%, 93%, and 88% respectively. This tells you that all is not well with her.

https://seekingalpha.com/article/4310549-ibm-shareholders-should-be-concerned

IBM aún no está muerta.

https://www.expansion.com/empresas/banca/2020/01/16/5e1f8332e5fdeab6648b45b2.html