Yo la doy por muerta. A ver si hace un rebote del gato idem , la vendo y hago sitio en el armario.

1 me gusta

Pero no para meter otro muerto, hombre

Esa es la idea, que el armario lo tengo superpoblado. Estoy cambiando la operativa para no volverlo a llenar. Vamos a ver como me sale la cosa.

2 Me gusta

Esto es un proceso largo y hay muchas cosas que hacemos que luego tenemos que corregir, hay que hacerlo poco a poco y cuando se puede, lo importante es darse cuenta

2 Me gusta

No encuentro que ha pasado con ella. Ha pasado algo raro?

Que igual la vacuna funciona, y la gente ya no se va a quedar en casa comiendo ketchup y mac&cheese.

Ayer, muchas de las acciones que se han visto beneficiadas por la pandemia no subían apenas o bajaban. Zoom creo que bajo un 20%

2 Me gusta

Supongo que Kraft era un valor “refugio” barato para estos tiempos de confinamiento y ahora ese dinero sale para ir a los mas castigados.

2 Me gusta

Hermanos, bendecidos seamos los que acabamos de cobrar el dividendo de KHC, pues ¿no estamos frente al advenimiento de un milagro? ¿no se alzará el caído en pos de la vida eterna? Tal es el camino de nuestra KHC y la senda que recorremos sus accionistas.

¡Prosperidad, eternidad!

15 Me gusta

Aquí otro que se está subiendo al autobús. Que la fuerza nos acompañe.

5 Me gusta

3 Me gusta

A ver si se anima la acción con la mejora de beneficios

Kraft Heinz vende su negocio de snacks Planters a Hormel Foods por 3.350 millones

El gigante de la alimentación busca reducir deuda e impulsar el crecimiento

5 Me gusta

A ver si la paciencia con el título se ve recompensada

2 Me gusta

Vaya, pues parece que entra volumen de compras

Como coja carrerilla hay hueco para subir

2 Me gusta

Bendita alegría, no contaba yo con este empujón de KHC… ¿Alguna justificación?

1 me gusta

A quien pueda interesarle

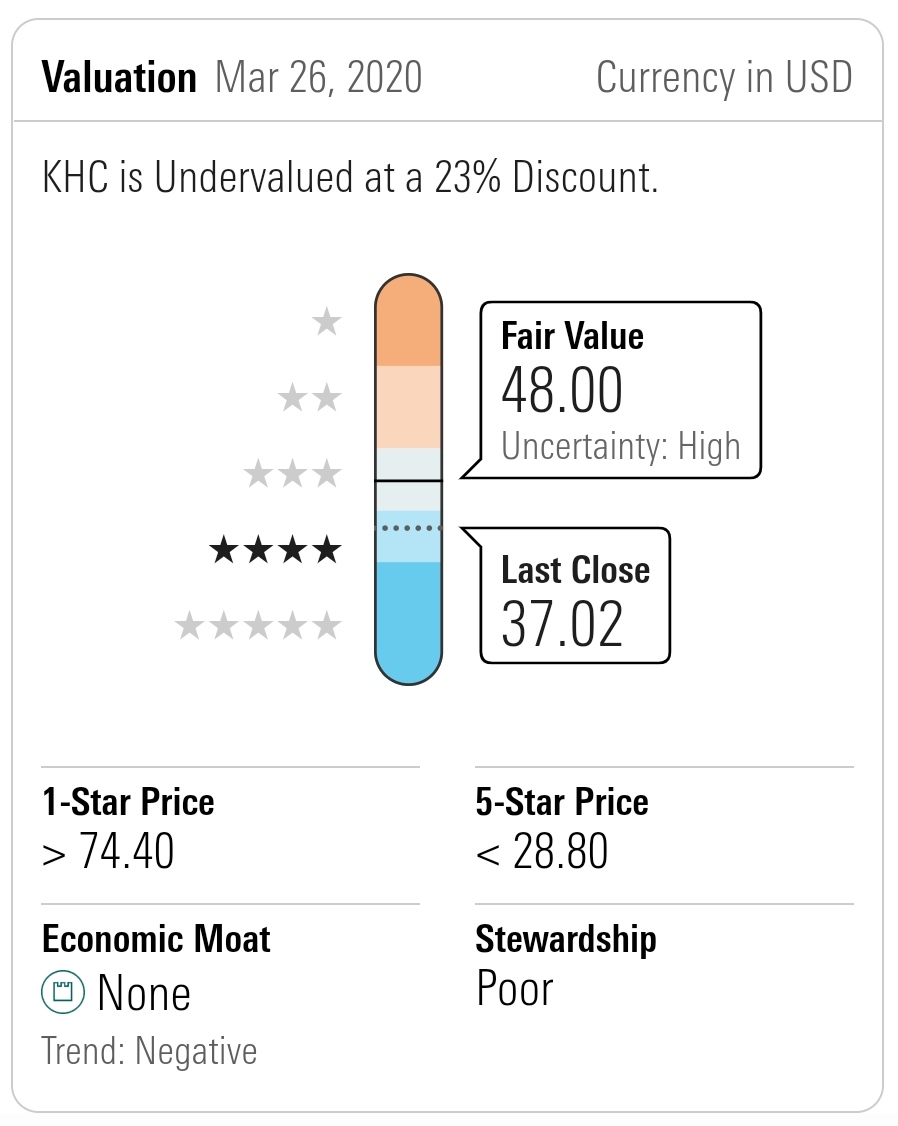

Fair Value and Profit Drivers | by Erin Lash Updated Nov 25, 2020

After reviewing results through the first nine months of fiscal 2020, we aren’t making any changes to our $48 fair value estimate for Kraft Heinz, which implies a fiscal 2021 enterprise value/adjusted EBITDA multiple of 14 times. We believe with shelter-in-place and social distancing initiatives, at-home food consumption should remain elevated in the near term, aiding firms like Kraft Heinz that sell the bulk of its wares through the retail channel (which we estimate at 85% of its total sales). However, we don’t expect this growth will persist at the same cadence, as consumers work through their at-home inventory and ultimately venture out to restaurants. We also expect competitive intensity could increase, especially against a more challenging macroeconomic backdrop. This aligns with management’s newly minted long-term targets (launched along with the dissemination of its revised strategic playbook) for 1%-2% organic sales growth and 4%-6% adjusted EPS growth. As such, our longer-term forecast calls for around 2% annual sales growth and operating margins holding in the low 20s.

Over the next few quarters, we expect increased demand and factors related to the coronavirus are likely to result in higher costs, particularly related to safety, logistics, maintenance, and labor. But despite these near-term costs, we’re encouraged by the firm’s commitment to investing behind its brands, even amid this uncertain climate (with a focus on marketing and media, which was up 40% between the second half of 2019 and the first half of fiscal 2020). And we don’t believe these were one-off investments, with management calling for a 70% jump in spending between the first and second halves of 2020. We aren’t surprised that previously planned innovation is on hold as the firm focuses its manufacturing resources on supplying retailers with the most in-demand offerings in the near term, which we view as prudent. We believe this ability to reliably deliver product to store shelves during the current pandemic could buoy the company’s previously impaired relationships with its retail partners. But to ensure this persists over a longer horizon, we think the firm will need to keep its foot on the gas. We forecast marketing, research, and development to expand to more than 5% of sales in the aggregate over our 10-year forecast versus less than 5% the last few years.

7 Me gusta

Mira por aquí ![]() :

:

https://twitter.com/Divgro22/status/1360516463099080704?s=20

6 Me gusta

OCU la pasa a recomendación de compra.

El grupo norteamericano de alimentación ha fijado unos nuevos objetivos para el período 2021-2024. Si bien no son demasiado ilusionantes, sí nos parecen coherentes y creíbles. Después de años de reducción de costes con el fin de aumentar los márgenes, Kraft Heinz continuará por esta misma senda (2.000 millones de dólares durante el período 2020-24), pero esta vez el ahorro obtenido servirá para impulsar el desarrollo del negocio. Al incrementar el gasto en marketing (+30% entre 2020 y 2024) y en nuevas inversiones (+20% entre 2020 y 2023), Kraft Heinz prevé dar un nuevo brío a los resultados.

2 Me gusta

Pues entonces es venta. Va a caer en picado.

4 Me gusta