Yo que soy accionista de IRM no lo considero como un REIT al uso (si bien su forma jurídica es un REIT) ya que en el fondo es una empresa de prestación de servicios de almacenaje más que de explotación de inmuebles. No es que lo considere mejor o peor.

Un saludo.

4 Me gusta

Estoy contigo @juanjoo, para mí es empresa que ofrece servicios de almacenaje, con clientes muy fieles y barreras de entrada enormes. Por ello, muy contento con esta adquisición.

En cuanto a REIT al uso querría incorporar O y SPG o WPC. Lo de URW mientras no cambien las retenciones europeas, nada.

4 Me gusta

De los Reits hay que esperar a una bajada sectorial, sí. De mi cartera solo estoy añadiendo a estos precios a SPG.

Llevo también O, FRT, SKT, VTR y ESS.

3 Me gusta

Yo también estoy razonablemente confiado con IRM. De REITs tengo BPY, GEO, OHI y Merlin; y valorando CorePoint Lodging y SKT.

2 Me gusta

Entre los REITs americanos solo contemplo WELL, VTR , DLR, NNN, PSA, O, SPG y WPC

5 Me gusta

¿Por qué ruindog?

Básicamente a través de filtros que voy poniendo: S&P Credit Rating igual o superior a BBB, 10 años aumentando o manteniendo el dividendo, 5-year dividend growth aceptable, M* Stewardship…

4 Me gusta

Big Thunder (Seeking Alpha)

High Quality Companies that May Currently Be Undervalued

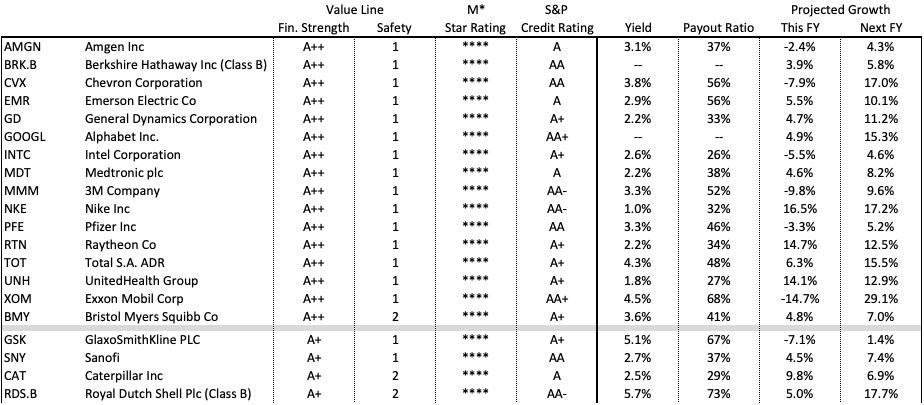

I ran a Value Line screen to find stocks rated A++ or A+ for financial strength and 1 or 2 for safety. From that list of 134 companies, I then found those that Morningstar currently rates either 4 or 5 stars for value, which indicates that Morningstar considers these stocks undervalued. (Others may disagree with M*'s assessment.) Of those, I eliminated any company with an S&P credit rating below A- as well as those with no credit rating. The remaining 20 companies are listed in the table below. Then I consulted FAST Graphs to provide each company’s current yield, payout ratio, and projected earnings growth for this fiscal year and the next. This will give you a quick look at whether any of these companies could potentially be worth further investigation. Note: I don’t follow all of these companies, so there may be headwinds, challenges, pitfalls, etc. that you would only discover in conducting your due diligence. In a rallying market, anything undervalued could be suspected of having some sort of issue.

12 Me gusta

Antes de leer vuestros comentarios acababa abrir posición en Exxon y convertirla en mi segunda posición de la cartera por capital aportado. Entré a 75 $ sin comisiones.

Estuve revisando los números recogidos en OCU, leyendo información sobre su negocio y viendo que en las gráficas aportadas por @ruindog es una fija entre en las mejor valoradas por segura y undervalued ( esta por debajo de la media de las 1000 sesiones). Yo viendo esto junto con el historial de 37 años años de dividendos crecientes no veo necesario más estudio ( tampoco me apetece  )

)

7 Me gusta

A mí Unibail rodamco me parece de lo mejorcito… Y ahora más.

Yo la tengo a 200 y muy tranquilo. Promediare seguramente

1 me gusta

A mi me ronda el pack de verano WBA ABBVIE IRM y T

1 me gusta

Lo mismo digo, al final tiene muchos centros comerciales en pleno centro de las ciudades, pero claro una adquisición siempre supone que pagan mucho…

Ya llegará su momento y ampliaré en cuanto tenga un buen report

1 me gusta

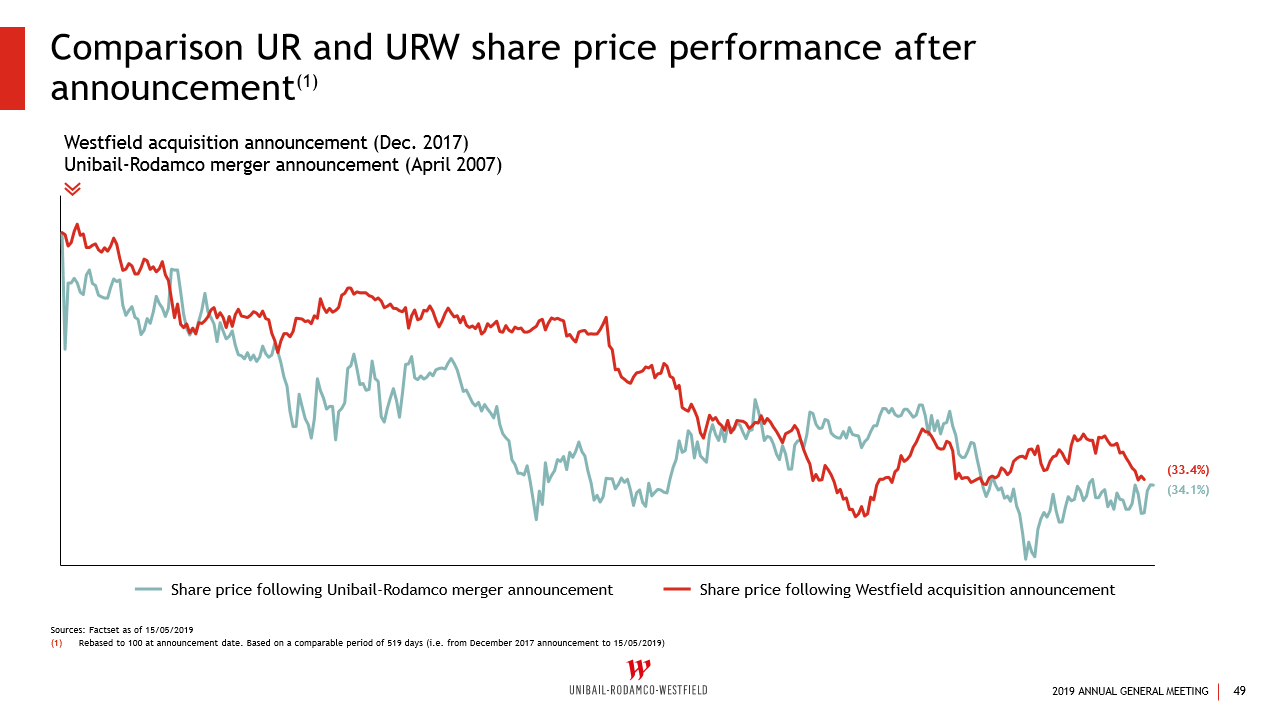

Cuando se produjo la fusión de Unibail y Rodamco hubo una caída muy similar en el precio. Que no significa que esta vez vaya a ser igual claro…:

3 Me gusta

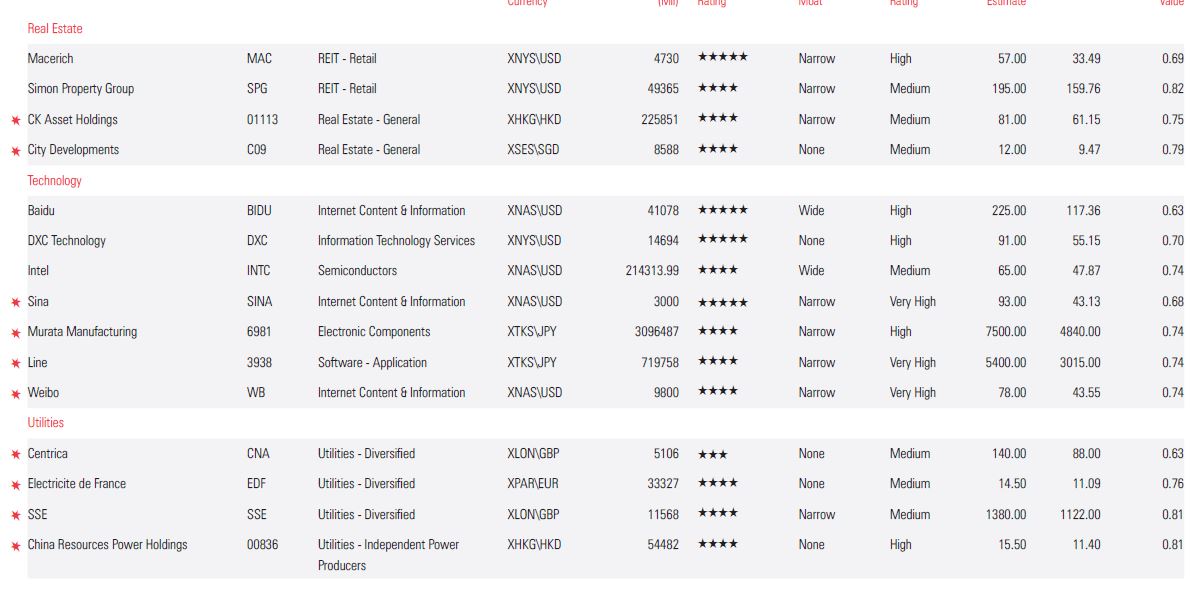

Our Europe Large-Mid Cap Pick List highlights our most undervalued stocks

on a risk-adjusted, sector-weighted basis. While the list is not intended to

be a model portfolio, we model our picks on a predetermined sector weight,

reflective of sector weight within the subset of Morningstar rated stocks in the

Morningstar DM Europe Large-Mid Cap Index. This weighting is recalibrated

annually to reflect substantial changes in our coverage and our respective

benchmark. As a result, our pick list offers idea generation for the diverse

needs of investors, ensuring ideas across a number of sectors. All picks are

constituents of the Morningstar DM Europe Large-Mid Cap Index.

8 Me gusta

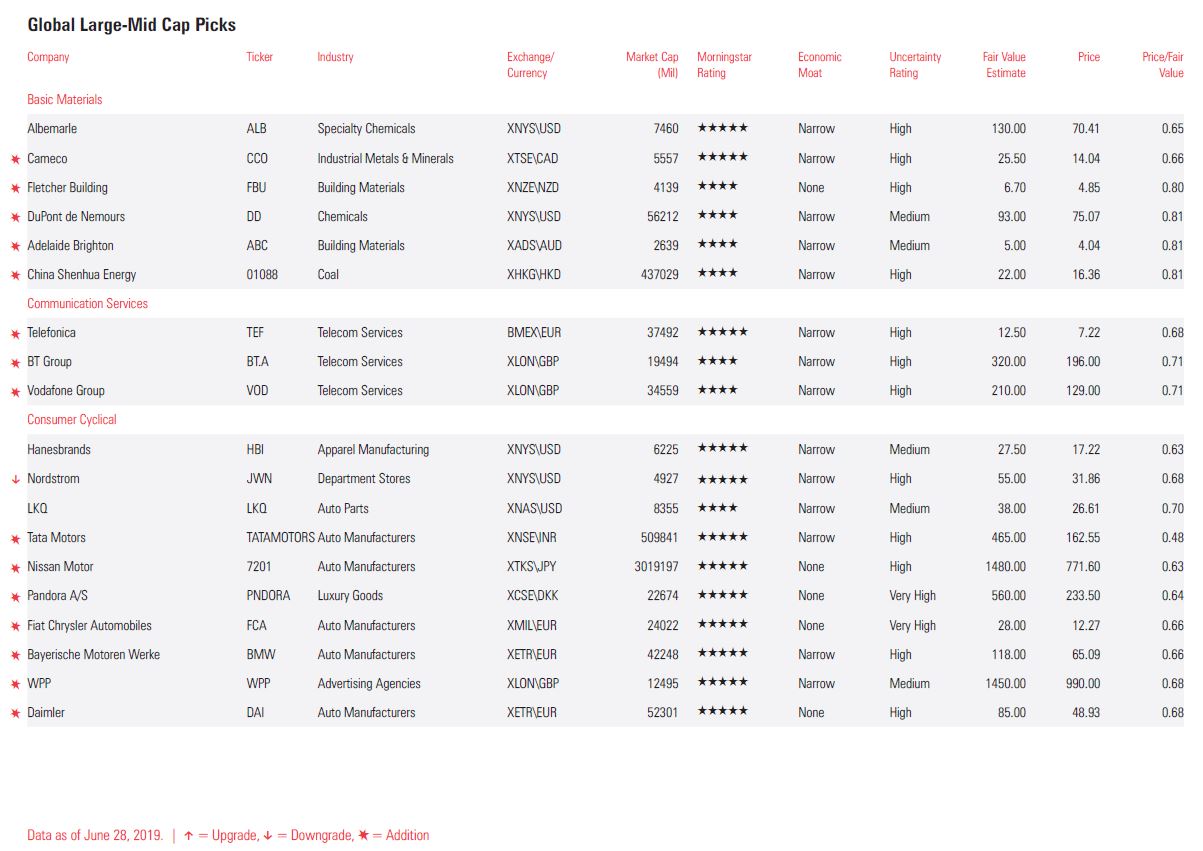

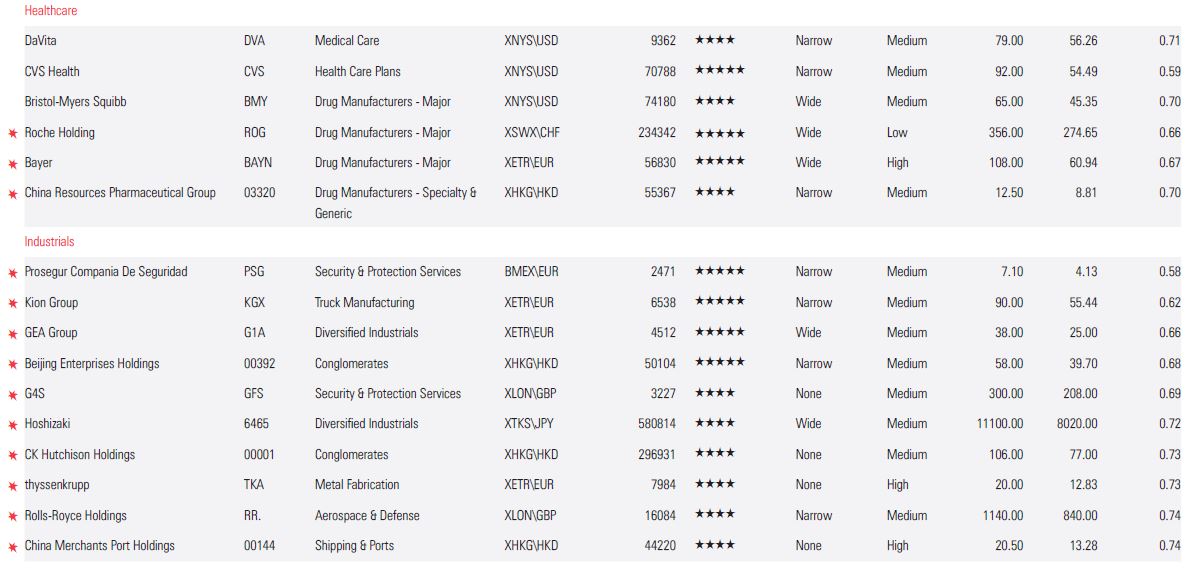

Our Global Large-Mid Cap Pick List highlights our most undervalued stocks

on a risk-adjusted, sector-weighted basis This pick list highlights constituents of the Morningstar Global Markets Large-

Mid Cap Index that we believe offer investors the best risk-adjusted return

prospects. Because the list is intended to be a source of idea generation rather

than a model portfolio, the number of picks we make in each sector reflects

our coverage count in that sector rather than our view as to whether the

sector offers relatively greater or fewer buying opportunities. The number of

picks in each sector is recalibrated annually to reflect substantial changes in

our coverage and our respective benchmark.

10 Me gusta

Miguel Lorca (Seeking Alpha)

Some of the stocks I’m looking to add to are: ABBV, AMGN, BLK, BTI, JPM, LEG, MO, SPG, UPS, USB, WFC, VLO, XOM.

6 Me gusta

Y otro aporte de un reputado analista ![]()

Ruindog (Foro Cazadividendos)

Top 80 Watchlist USA/Canada

Energy: ENB, CVX, XOM, EDP, MMP

Industrials: AOS, MMM, CMI, DOV, ETN, EMR, ITW, PNR, GWW, CAT, LMT, ADP

Consumer Staples: ADM, BF.B, KO, PEP, CHD, CL, KMB, PG, GIS, HRL, MKC, WBA, MO, PM

Heathcare: AMGN, ABBV, PFE, JNJ, MDT, ABT, BDX, UNH

Utilities: CU, FTS, NEE, SO, PPL, WEC, BIP, CNP, D

Financials: TD, BLK, BRK.B, TROW, MA, V

Reits: VTR, WELL, DLR, NNN, PSA, O, SPG, WPC

Technology: AAPL, INTC, QCOM, GOOG, MSFT, CSCO

Telecom: T, VZ

Materials: APD

Consumer Discretionary: NKE, VFC, GPC, DIS, MCD, SBUX, HD, LOW, TJX

17 Me gusta

Menos BLK, JPM, USB, WFC y XOM llevo el resto.

1 me gusta

Te compro la mayoria por no decir todas

3 Me gusta

En mi caso llevo 52 de esos valores en cartera. A las restantes nos le quito el ojo por si se alinean los astros. Voy a intentar preparar el Watchlist europeo este fin de semana.

9 Me gusta