Yo reits llevo ohi, geo, irm, bpy y Merlín. No me importaría añadir algún otro: Skt, ltc, esrt o store.

1 me gusta

yo también llevo IRM

me gustaría tener WPC y STAG pero no a estos precios. todavía me lamento no haber comprado el pasado enero (pero vamos tengo un montón así  ; la pasta no llega para todo…)

; la pasta no llega para todo…)

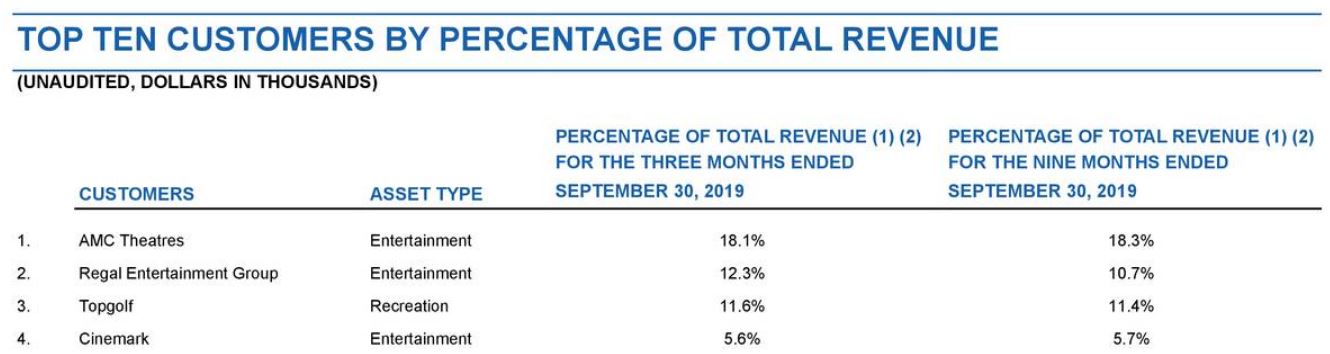

EPR me gusta el pago mensual pero no se que me da que sus 4 clientes principales supongan el 46% de la facturación. Casi casi, en vez de mirar los números de EPR, habría que mirar la salud de estos 4.

Además, 3 de los 4 son de entretenimiento (cines, teatros etc.). Puede que sea muy escéptico pero en este caso no la veo tan clara.

4 Me gusta

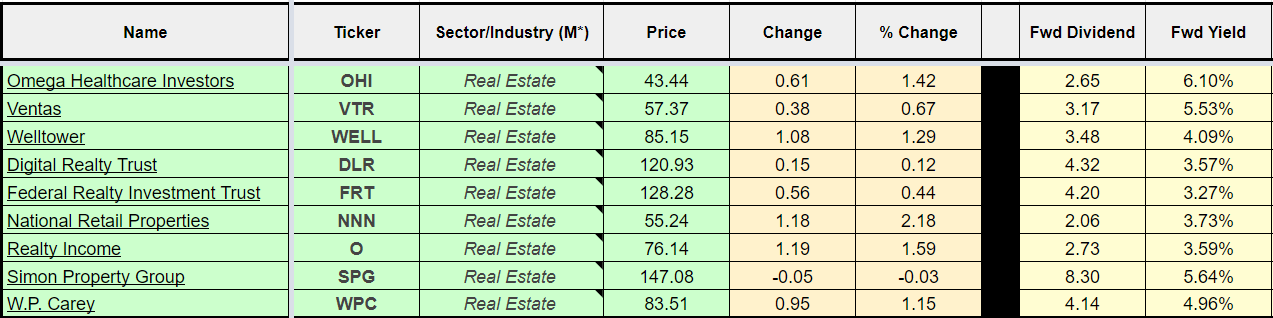

“See if REITs are yielding over 6% with a manageable debt, and restrict yourself to the excellent management teams of firms like Realty Income and W.P. Carey” The Conservative Income Investor

7 Me gusta

Es lo que me gusta, el sector en el que esta, y no solo teatros, tambien algun parque de atracciones, campos de golf, escuelas y estaciones de esqui.

2 Me gusta

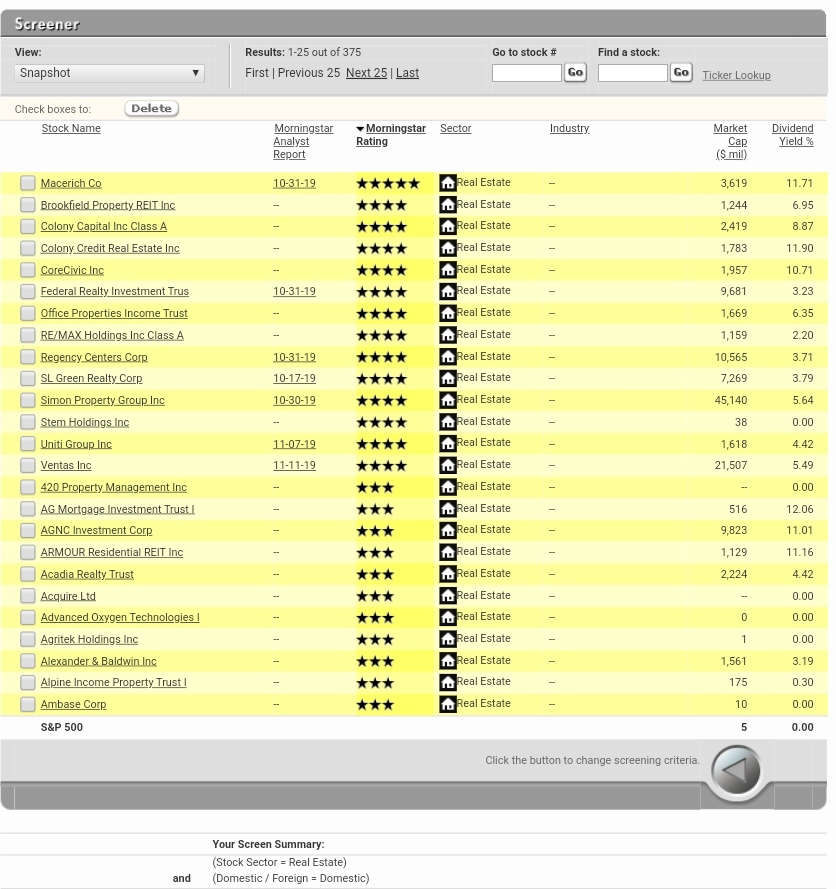

Se que os encantan los Reits pero, desde una perspectiva de largo plazo, DGI, o al menos B&H, no creéis que prácticamente todos los de mayor calidad están muy caros, excepto SPG? Y específico SPG porque tiene 4 estrellas, es uno de los mayores del mundo, con Moat Narrow y con una de las mejores calidad crediticias de su sector.

Si jugamos con los filtros de M*, no hay ni uno con 5 estrellas americano, exceptuando Macerich que es small cap, si además le añades que tengan Moat al menos Narrow, desaparecen la gran mayoría, incluso los de excelente gestión como O y WPC…

Dicho esto, cuando habláis de todos los REITs que veis para entrar, es con una perspectiva a largo plazo o corto-medio plazo?

7 Me gusta

Pues depende del REIT.

SPG largo plazo tal como comentas. Ahora está en un momento flojo, tendríamos que aprovechar para entrar? Yo lo he hecho, tengo la posición no se si completa pero si lo que quiero tener.

Tengo WPC por su diversificación y me gustaría entrar en O. Ninguno más.

El resto de los que tengo, para mi son generadoras de cash brutales, vacas lecheras. Cuanto tiempo estarán en mi cartera? Pues depende de la evolución de mi tasa de cobertura.

A medida que la tasa de cobertura de gastos cubiertos por dividendos aumente, irán desapareciendo poco a poco. 3, 5 años, no creo que mucho más.

4 Me gusta

Yo por lo menos tengo de los dos. Creo que me quedare “para siempre” en reits generalistas como BPY y Merlin y en reits sanitarios como OHI. Creo que IRM si que le daría voletos en sus máximos hsitóricos de 41$. Y luego tengo GEO que no se muy bien en que grupo meterlo.

Dicho esto creo que es algo “injusto” valorar los reits con los criterios normales. Yo asumo que si me dan un RPD del 5-10% y eso va acompañado de un payout del 90% pues ese dividendo puede verse afectado en épocas malas. Pero así es el sector, y como dice Miguel Angel generan un cash brutal para otras compras.

3 Me gusta

Yo a IRM le daría un cierto margen de confianza.

En cambio GEO, que también da muy buenos dividendos, a la que pegue un estirón igual la vendo.

2 Me gusta

Bueno digamos que a largo plazo no veo mal el sector de GEO más allá de los vaivenes políticos. El sector de IRM lo veo algo más cuestionable a LP, el papel irá a menos. Pero desde luego si consiguen crecer en tema de custodia de material informático y en el tema de prestar servicios a empresas también podría ser una empresa a tener toda la vida.

1 me gusta

Perfecto, ahora os entiendo un poco más. Sin lugar a duda son un generador de cash muy grande, si se cogen en ciclo expansivo como ahora y se pueden aguantar un tiempo sin que bajen el dinero que pueden generar durante todos esos años es enorme.

Particularmente para largo plazo intento mirar los que todos sabemos, SPG, O, WPC, PSA… (de estas solo llevo SPG) y fuera de USA llevo URW.

Pero entiendo perfectamente que se quieran coger en ciertas caídas aquellos que solo se quieren para un medio plazo, de hecho, yo llevo algo de IRM y he llevado otras (OHI y HCP).

La única pega que puedo poner es que todo está sensiblemente caro, aunque entiendo que con las RPDs que manejan los REITs sigan compensando

3 Me gusta

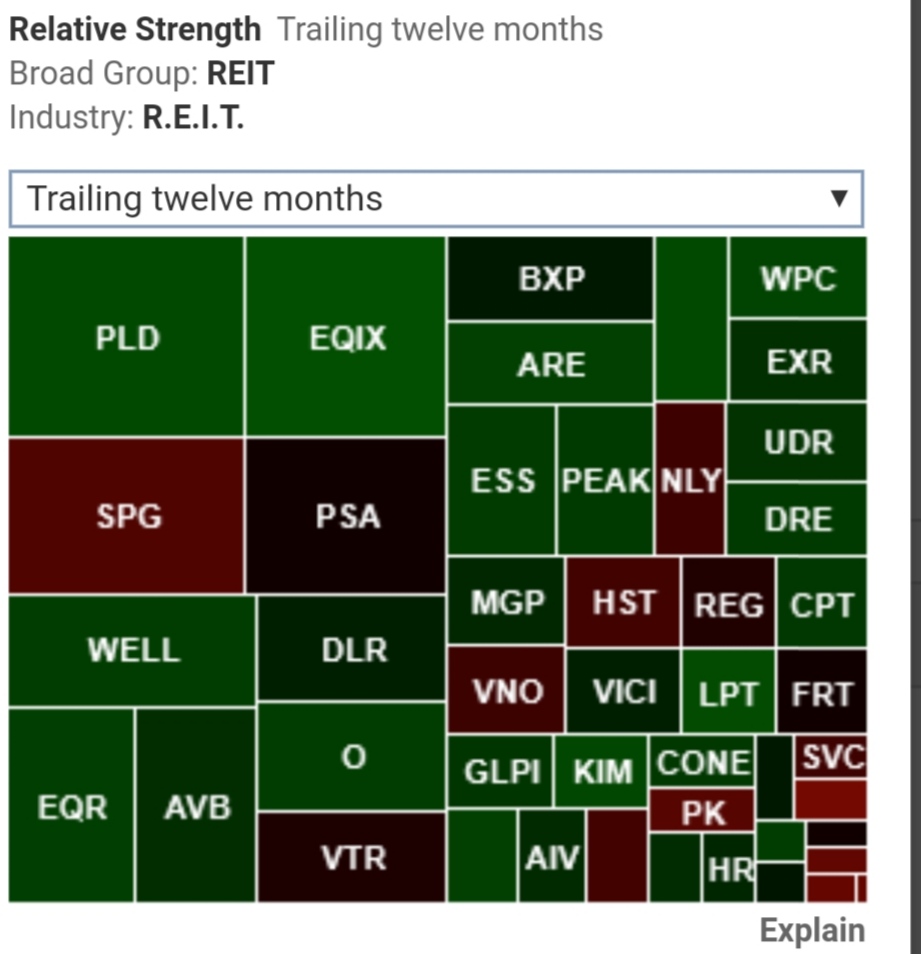

Vuelvo a poner el mapa de calor de ValueLine para los REITs

Tengo que decir que la fuerza relativa (precio de las acciones con respecto a la media evaluada por valueline) está más baja (los valores están tirando más a rojo) y en teoría los REITs estarían a mejor precio que hace unos meses.

Dejo también la perspectiva del sector para ValueLine:

Industry: REAL ESTATE INVESTMENT TRUST

Pubdate: January 3, 2020Page Number: 1510{/STORY;reit}{industry}The REIT (Real Estate Investment Trust) Industry is currently ranked (22) for year-ahead price performance. As a result, the group is well positioned, relative to the Value Line pack.Most REITs likely closed out the full year 2019 with a respectable showing. Further, we look for continued progress in 2020, which is just getting under way. Meanwhile, it should be noted that these businesses, which are tied to the real estate markets, tend to be conservative, and progress tends to be moderate, but steady. In this way, the REIT group is seldom as exciting as some other areas of the market, like the technology or medical sector, for instance.Attractive Operating ClimateREITs generally perform well when interest rates are low. Of note, the Federal Reserve reduced interest rates on three separate occasions in 2019. While we do not anticipate another series of cuts will be forthcoming in the months ahead, the central bank has affirmed its commitment to a supportive monetary policy, and will most likely use the tools at its disposal to keep the economy vibrant. In the current climate, fixed-income investments have become less attractive for investors. As a result, many on Wall Street have turned to conservative equities that offer large dividend yields. Among this group, some investors favor tax-efficient vehicles, such as Limited Partnerships (LPs) and REITs. Of note, as part of their corporate structure, these businesses are exempt from paying corporate taxes, but are required to distribute the bulk of their income to shareholders. This partially explains the high yields provided by these types of stocks.In addition, REITs benefit from a low rate climate in other ways. Foremost, REITs own vast amounts of property and land, and often maintain development pipelines that require capital funding. In order to support these investments, it is necessary to secure mortgage or commercial debt. In a low rate climate, the cost of capital should move down, which is a plus for businesses that borrow. Consequently, operators, such as REITs, can secure new debt at attractive terms, and can retire, or refinance, older higher-cost obligations. Many REITs have taken this course of action, and have managed to significantly improve their finances, by lowering interest expense and extending maturities.Some Sectors To WatchThe apartment operators are probably the most common type of REIT investment for a number of reasons. For one,

many retail investors see these vehicles as an attractive alternative to full ownership of apartment units. They provide some of the benefits of property ownership, with none of the hassles associated with being a landlord and having to provide management services. Further, apartment REITs can be easily understood by most investors, and are less complicated than specialized operators in the office, industrial, or healthcare arenas. Apartment REITs have performed relatively well over the past year. Value Line covers a number of these issues. Some of the biggest are Equity Residential, AvalonBay Communities, and Essex Property Trust. Specifically, AvalonBay and Equity Residential have vast portfolios that span much of the country, while Essex Realty owns property mostly situated on the West Coast, making it more specialized. Generally, the outlook for apartment REITs remains bright. Occupancy levels are optimal, and should be enhanced by incremental rental rate increases, along with well-controlled operating costs.The healthcare REITs have been somewhat mixed lately. There have been concerns about intense competition in the senior housing area. However, looking out, demand for housing aimed at the elderly population will probably strengthen, as individuals are living longer and receiving better healthcare coverage. The medical office and life science areas look attractive. Many healthcare REITs have been expanding their portfolios here. Tenants are usually universities and corporations, and operate with limited regulation. Some large REITs in this area, include Welltower, Healthpeak Properties, and Alexander Real Estate Equities.Among the specialty REITs, there is a group that invest in correction facilities. The shares of these stocks have come under considerable pressure over the past few years, as the political and legislative climate has shifted away from for-profit correctional facilities. Value Line covers CoreCivic and GEO Group, and both of these issues provide large dividend yields at this time. But investors should note that there may well be risks associated with these vehicles.REITs may be of interest to income investors, as they offer dividend yields significantly above the Value Line median. Too, these issues tend to be stable and less volatile than the broader market. As always, we recommend that all subscribers consult the full page report pertaining to any stock that is under serious consideration. As always, investors should take note of Timeliness and Safety Ranks before making decisions.

6 Me gusta

Eso es, con RPDs del 7-9% mantenerlos una temporada te nutre de cash de una manera constante

3 Me gusta

Una especialización de REITs. Datacenters.

En resumen: alquilan sus m2 para albergar Servidores.

4 Me gusta

Yo llevo unos cuantos: SPG, SKT, MAC, IRM, WPG y para una cartera familiar URW. Y he tenido OHI y VER.

3 Me gusta

Yo ahora llevo IRM, SPG, SKT, GEO y URW, pero he llevado O, EPR, WPC, OHI, STAG y alguno mas que no recuerdo

4 Me gusta

Me jodieron con VNQ así que ahora llevo una minicartera de REITS formada por:

O, OHI, URW, NNN, VTR, IRM, STAG, WPC, DLR, SPG y PSA

¡Qué asco el que le he cogido a URW!

3 Me gusta

Hola buenas tardes,

Estoy valorando añadir un reit americano a mi cartera. He estado leyendo por varios foros y por lo que he visto, la retención en origen no está clara si es un 30% o un 15% como en el resto de acciones.

¿La retención en origen es del 30%, aún disponiendo de el formulario W-8BEN ?

¿Alguien tiene claro que es lo correcto?

Gracias

No se qué es lo correcto pero ING retiene el 15% en origen en los REITs

1 me gusta

Gracias Vash. ¿Y Degiro lo sabes por casualidad lo que retiene?

1 me gusta