yo las tengo compradas de enero, imaginaos el roto que llevo, y en yoc se me quedan bastante bajas. No obstante no venderé ya que las pérdidas serían grandes puesto que ocupa una posición importante en mi cartera.

Mi tesis es una recuperación rapida del petróleo en el Q3 y Q4 e incrementos de divis en sucesivos años.

De todas formas dudo que vuelvan en mucho tiempo al entorno de los 23 libras a las que compré mas o menos.

Reconozco que fue un error invertir tanto de golpe en esta empresa, lo hice antes de migrar a IB y con ING ya se sabe o compras bastante o las comisiones te comen.

Llevo 20 años invertido en el sector petróleo y es actualmente, con diferencia, mi mayor ponderación de la cartera. En estos 20 años ha habido de todo, recortes de dividendos, bajadas de un 70% del precio, subidas… y tras dos décadas, sigue siendo tremendamente rentable. Para ello sólo he tenido que hacer tres cosas: no mirar constantemente el precio de la cotización, reinvertir religiosamente cada tres meses más alguna compra más y esperar… esperar y esperar…

El recorte de un dividendo es, en principio, lo peor que pueden hacernos si en lo que estamos es en reinvertir, pero no tiene por qué ser así. No paro de leer en este foro que mucha gente va a largo plazo, pero ve un recorte y enseguida abandona la posición (o desearía hacerlo pero no se anima porque las pérdidas son altas).

Lo he visto con las acciones de petróleo y con alguna más, BHP BILLITON por ejemplo, pego recorte y eso me permitió sumar más acciones a las que tenía. Cuando lo recupero todos querían subirse al carro…

Shell está entre las 5 mejores petroleras del mundo (posiblemente entre las 3 primeras) y debe ser una de las 20 o 30 empresas más rentables del mundo, con y sin dividendo.

El petróleo y el sector energético/materias primas es así, reinversiones a precios bajos hace que en 20 años la cifra en la cuenta llame la atencion, eso es invertir a largo plazo.

Salu2 y suerte

Yo estoy en la lista de damnificados y todavía no tengo claro que haré con las acciones pero me ha parecido muy interesante este punto de vista que he leido en Seeking Alpha a un forero

Shell is not a dividend growth company. It’s a company that pays a dividend.

As such, the dividend is more of an afterthought than it is a committment to shareholders.

If you bought this for dividend growth, there hasn’t been any. If you bought if for capital appreciation, there hasn’t been much of that for a while.

So what would be the compelling reason to buy stock in this company?

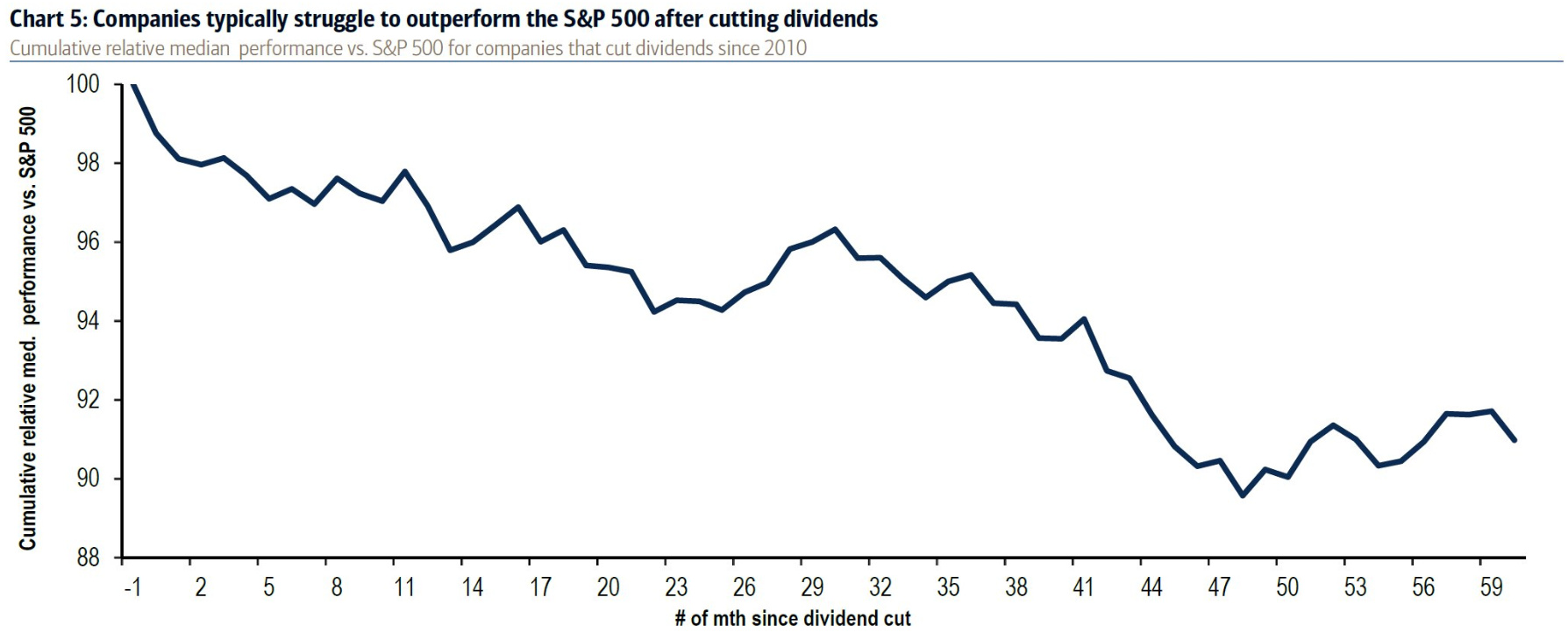

Más madera. Parece que vender después de un recorte de dividendo es “en promedio” una sabia decisión

Perdonar aunque ya habéis hablado de esto en el hilo…me aparecen los divis en degiro en dólares…nunca antes me habían aparecido asi… las llevo en Ámsterdam… sabéis porque esta vez?.. encima que recortan mareando al personal…psss

Shell faces spending scrutiny after dividend cut

Shareholders push for clarity on strategy following slashed payout*

Royal Dutch Shell is facing growing pressure from investors for clarity on its spending plans after the company announced a dramatic two-thirds cut to its quarterly dividend.

In discussions with the Anglo-Dutch group’s chairman, chief financial officer and investor relations team in recent weeks, some of the world’s biggest asset managers and pension funds have pushed for disclosure on its capital allocation strategy — from new projects to shareholder payouts.

At least four of Shell’s biggest investors said they had separately held conversations with the oil company urging it to outline how it planned to create value for shareholders in the coming years in the wake of the dividend cut.

One top 20 investor said: “If you can’t understand where the company is going, and they aren’t paying a dividend [as large as before], why would you own the stock? We are pissed off with them because they cut the dividend.”

In April Shell reduced its quarterly payout to 16 cents a share from 47 cents — its first dividend cut since the second world war. The company said it was part of a rebasing as it made a “fundamental shift” over the next 30 years to become a net-zero emissions business by 2050.

The move, which coincided with a dramatic hit to earnings from the coronavirus pandemic, marked a U-turn from 2019 when it pledged $125bn in shareholder handouts over the next five years.

“We have asked them what they are planning to do with this cash [that they will save from the dividend cut]. They are struggling to answer that,” the top 20 investor said.

Shell argues that this is money the company does not necessarily have in the first place.

Ben van Beurden, chief executive, said in May that it was “not wise, prudent or even responsible to pay out a dividend if you know for sure that you have to borrow for it, deplete your liquidity and, at the same time, also reduce the resilience [of the company’s finances] in a world that will be totally unpredictable for some time to come”.

The hefty dividend had always been central to Shell’s investment case but analysts had long questioned its sustainability given the pressure on the company to shift from hydrocarbons to lower-margin, cleaner energy businesses in the future.

But investors said that given Shell’s decision was akin to making a call on how the energy market would play out in the future, the oil major also needed to set out an updated capital allocation plan for the coming years.

On a group call with big investors in May, chairman Chad Holliday faced a barrage of questions over why Shell had not combined the dividend shift with a clear strategy for the future.

Another top 20 investor said it had been holding “lots of one-to-ones” with Shell because the oil group had “an issue with clarity of capex plans”.

A third large shareholder said that more than a month after the dividend cut, investors urgently needed details on the company’s capital allocation plans.

The company said it would give investors a strategy update when it was clearer how it would get through the coronavirus crisis.

Shell said in March that it would not continue with the next tranche of its share buyback programme. The company also said it would cut capital expenditure to $20bn or less this year, from $25bn in 2020 and reduce operating costs by up to $4bn.

It is also scrapping bonuses this year, delaying projects and firing contractors. The company has cancelled its purchase of a fourth executive jet due for delivery in May to conserve cash, after taking delivery of three new aircraft to replace an older model between February 2019 and February 2020.

Pues me parece lógica la actitud de los accionistas. La diferencia entre ellos y nosotros es que a ellos les harán caso

Una empresa como Shell con su historial de dividendos tiene detrás grandes grupos financieros e incluso países que depositan sus fondos de inversión. Ha sido tan drástico y tan de sorpresa que deberían, al menos, explicar que linea quieren seguir a partir de ahora. Se ha quedado un dividendo para el riesgo y la volatilidad que tiene la empresa que no sale a cuanta entrar a estos precios:

3,92% de div frente a un 6% de AT&T, el 8% de ENAGAS o el 8,25% de ALTRIA…

BP está casi en un 10%, EXXON en un 7% y CHEVRON en un 5,36%

Creo que sigue siendo una muy buena empresa que seguirá dando alegrías al accionista, pero tienen que despejar dudas sobre el recorte, el paro de recompras de acciones y el paro de inversiones.

Hola alguien se ha acogido a la “reinversión” de dividendos en ING de Shell?

Es por saber si ya os han adjudicado las nuevas acciones porque a mi todavía no me las han dado.

Gracias y un saludo

Gracias

A mi tampoco me las han asignado y si cobrado desde hace una semana algo menos de un euro.

He llamado a ing y me ha tocado el típico que no tiene ni pti. Está claro que hay algún tipo de incidencia en el volcado de las nuevas acciones a las ya existentes en este valor porque el cargo en la cuenta ya está desde el día 29 de Junio.

Me han dicho que me espere una semana o dos cuando en otras ocasiones cuando se realiza el cargo te dan la acción.

Llamaré mañana a ver si doy con alguien que tenga idea

Las tengo en holanda, no se si se puede hacer eso…

¿Split de Shell?

Summary:

RDSA@AEB announced a forward split effective 20200813.

The terms of the split are 2 : 1.

Please note that this action is a mandatory action.

Esto lo pone bastante a menudo IB cuando hay scrip dividend o casos así. Con Shell es bastante habitual que lo indique así.

Pero vamos, es el próximo dividendo. Menguado, eso sí

Para mí que estos de IB tienen algún bug en el sistema porque el 13/08 es la fecha ex-dividend del dividendo (0.16$) que abonarán el 21/09

Tengo las RDSA en Amsterdam. Con muchas pérdidas que me van a “venir bien” para compensar otras ganancias que he tenido este año. Me parece que esta semana voy a vendelas y al mismo tiempo comprar las RDSB en Amsterdam en euros. Para mantenerlas al menos un par de meses para no imcumplir los plazos y volver a cambiarlas por las otras. Voy a largo con la empresa, a estos precios es un 5% de dividendo (si no lo recortan más) y en principio está bastante barara.

La razón de tenerlas en € es porque quiero tener una cantidad importante de empresas en EUR (porque es la que uso en el día a día y porque creo que no lo va a hacer tan mal como se piensa) y ahora mismo tengo la mayoría en USD (que tiende a la depreciación) y una cantidad decente en GBP (que no pinta demasiado bien).

Supongo que nadie en IB ha pedido cobrar el dividendo las RDSB en EUR. En principio no creo que las tenga mucho hasta que haga el cambio y me da igual cobrar en libras, pero por curiosidad…

¿Estás seguro de que hacienda no puede considerar valores homogéneos las acciones de RDSA y las de RDSB?

Estoy en el mismo caso que tú, y sería muy interesante lo que propones

En teoria si tienen 2 ISIN diferentes, cuela, no?

Hay gente que hace con las ADR, no?

Tienen isin diferente, % diferente de la empresa y distintos derechos (las B cobran después en caso de quiebra por ejemplo). Casi seguro que no son homogéneos.

En concreto, se consideran homogéneos el conjunto de valores negociables procedentes de un mismo emisor, que formen parte de una misma operación financiera o respondan a una unidad de propósito, incluida la obtención sistemática de financiación, y que tengan igual naturaleza y régimen de transmisión, y atribuyan a sus titulares un contenido sustancialmente similar de derechos y obligaciones.