Morningstar

Business Strategy and Outlook | by Kevin Brown Updated Apr 02, 2020

Simon Property Group, the largest mall real estate investment trust and second-largest U.S. REIT, manages one of the top retail portfolios in the country. It owns and operates Class A traditional regional malls and premium outlets in markets with dense populations and high incomes; these malls frequently have domestic or international tourist appeal. The high-quality properties will continue to provide consumers with unique shopping experiences that are hard to replicate elsewhere, and as a result, we think Simon’s portfolio will be sought after by retailers that are increasingly pursuing an omnichannel strategy.

E-commerce continues to pressure brick-and-mortar retail as consumers increasingly move their shopping habits online. When excluding categories of retail sales that are generally found neither in malls nor online, like autos, gasoline, groceries, and building materials, e-commerce now accounts for more than 20% of all retail sales. While we believe that online sales will continue to grow at a significant spread over brick and mortar, we also believe physical retail sales growth will still be positive over the next decade. Retailers are becoming more selective with their physical locations, opting to locate storefronts in the highest-quality assets that Simon owns while closing stores in lower-quality malls.

Additionally, many e-tailers are beginning to open stores in Class A malls to take advantage of the high foot traffic, as a physical presence provides additional marketing, a showroom for products they want to highlight from their online store, and another source of sales.

However, Simon must deal with the fallout of the current coronavirus pandemic. Malls are closed and shopping at brick-and-mortar locations has dramatically fallen. While Simon’s revenue is somewhat protected by long-term leases, we see retailer bankruptcies causing a significant drop in occupancy and Simon being forced to offer rent concessions to keep others afloat. We believe that Class A malls will rebound and that these high-quality malls will eventually return to their prior occupancy and rent levels, but the short-term impact to Simon’s cash flow will be significant.

Fair Value and Profit Drivers | by Kevin Brown Updated Apr 02, 2020

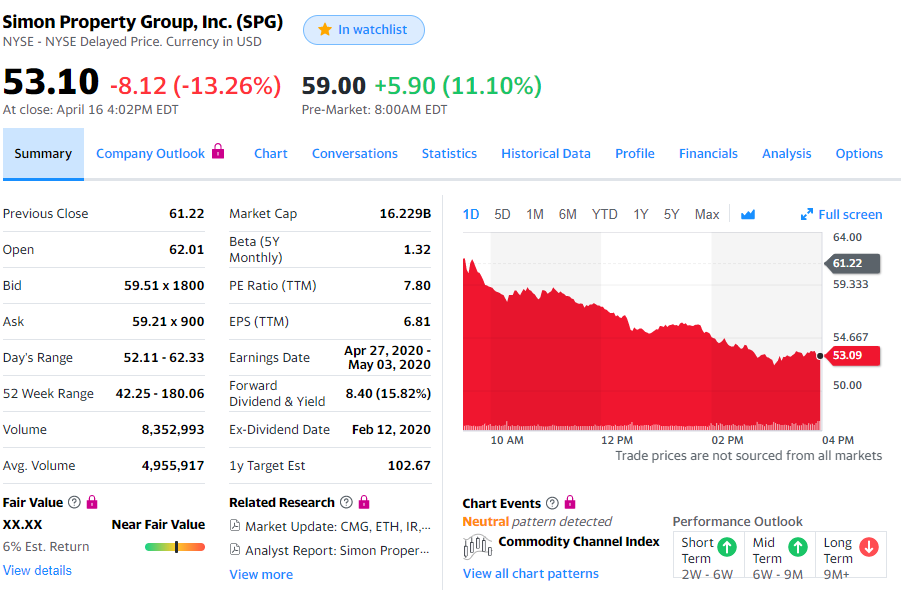

We are decreasing our fair value estimate to $154 per share from $187 after updating our internal growth assumptions for the short-term and long-term impact of the coronavirus. Our fair value estimate implies a 3.9% cap rate on our forward four-quarter net operating income forecast, 21 times multiple on our forward four-quarter funds from operations estimate, and a 5.5% dividend yield, based on a $8.40 annualized payout.

We assume that the coronavirus will cause occupancy to drop to under 80%, a 15% year-over-year decline, though occupancy will increase over the coming years back to a 92.5% level. We also believe that long-term brick-and-mortar retail sales will slightly weaken. Simon should continue to see positive sales growth, but re-leasing spreads are likely to turn negative. The occupancy, minimum rent growth, re-leasing spreads, and margin assumptions drive total company annual same-store NOI growth averaging 0.9% across our 10-year forecast. While we assume that Simon closes on the $3.6 billion acquisition of Taubman Centers in the third quarter of 2020, we don’t believe Simon will have any other significant acquisition opportunities as most Class A malls are already owned by long-term investors. We project $1.2 billion of investments in the company’s pipeline of new development and redevelopment projects at an 7.5% average yield in 2020 that slowly declines over time to $1.0 billion at a 6.9% average yield as construction costs rise and accretive projects become harder to source.

We estimate Simon’s net asset value to be approximately $102 per share based on a 5.5% cap rate assumption. We use NAV as an assessment of potential private market value, essentially viewing the firm as a portfolio of assets. To calculate NAV, we utilize recent asset transactions to assign a cap rate to each segment of the portfolio, apply the cap rates to arrive at gross asset value for the company’s real estate, put a multiple on the company’s non-real estate assets, add the non-income-producing tangible assets, then net out the company’s liabilities (excluding corporate overhead considerations). We find NAV to be a useful data point in gauging the underlying value of the firm, especially the likelihood of realizing this value through potential asset sales, recapitalization, or merger and acquisition activity.