Web corporativa: https://www.tysonfoods.com/

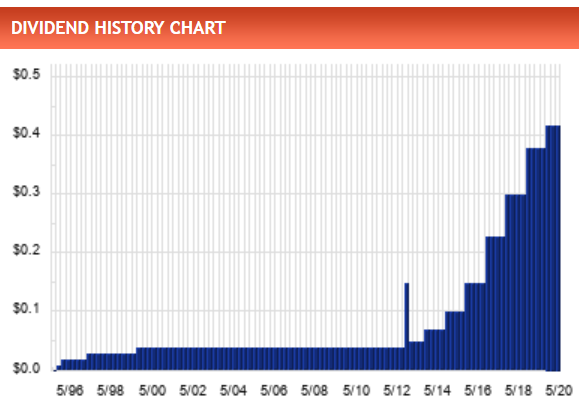

Dividendos:

Web corporativa: https://www.tysonfoods.com/

Dividendos:

Inicio posición en TSN, bastante castigada por infecciones de covid 19 en sus plantas de producción, tiene crecimiento de dividendos de más del 15%, PER 11, cuando su media es el 13.

Qué más puedes contar de Tyson Foods? No la conocía, parece un consumer staple interesante

Tiene pocos años de crecimiento de dividendos, pero crece DGi1 a 17%, DGI 3 a 35% y DGI 5 a 28%, yield 2,69% y payout 0,30%.

Yo llevo observándola un par de semanas, tiene muy buenas puntuaciones en simplysafedividends, un 99 very safe… y tal y como dices buen crecimiento de sus dividendos, pero a la vez a ido subiéndolos año tras año pero aumentando su payout. Quitando eso, igualmente tiene un payout bastante bajo.

Como la veis el resto?

Un saludo

Parece que el tema covid lo tienen ya más o menos controlado, realizando pruebas a todos los empleados y poniéndolos en cuarentena. Se lo tomaron en serio.

Suena bien la empresa. Es un sector que tengo muy muy infraponderado. La analizaré un poco. Hoy baja otro 6%

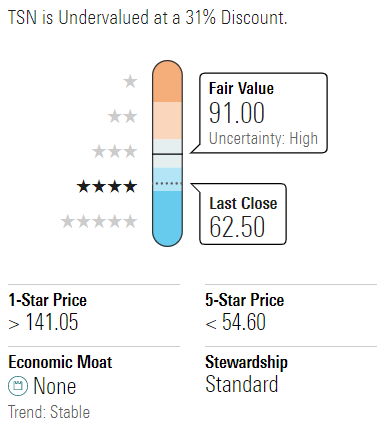

(Morningstar)

No-Moat Tyson Facing Several COVID-19 Challenges, but Shares Compelling for Long-Term Investors

We plan to lower our $91 fair value estimate for no-moat Tyson by a mid-single-digit rate, as we now think strength in retail will not offset weak food-service demand, and incremental costs should modestly lower operating margins (beyond our 8% prior outlook). We initially assumed strength at retail (45% of 2019 sales) would offset declines in food-service (31%), but as some food-service capacity cannot be adjusted for retail, we plan to modestly lower our fiscal 2020 sales forecast.

Tyson’s second-quarter results (sales grew 4.2% and the operating margin declined 170 basis points to 4.6%) were overshadowed by the broad disruption ensuing from the coronavirus outbreak. For one, Tyson is experiencing outsize worker absenteeism in its production facilities. Protein processing is labor-intensive, with employees standing near one another, which has led to COVID-19 outbreaks at several plants. We estimate about a third of beef and pork capacity is impacted, with plants either closed for several days, or running slower line speeds. This disruption has caused livestock prices to fall, while prices for cuts of processed meat have increased, which lowers Tyson’s cost while increasing its selling prices. We think this benefit will be substantial, as livestock is the largest cost component for Tyson’s beef and pork segments, which account for nearly half of operating profit. As such, we expect this benefit to offset a material portion of incremental costs, such as $120 million (0.3% of sales) in frontline bonuses, temperature scanners, protective equipment, guaranteed pay related to disruptions in shifts and sick time, and fixed cost deleveraging as plants are temporarily idled for cleaning, quarantines, and/or weak demand.

Shares fell 8% on the report, trading in 4-star territory. We think Tyson is best suited for long-term investors. Even given volatile swings in profit margins that can occur in commoditized businesses, we think the margin of safety is attractive.

Gracias ruindog, no la tenía en el radar pero me he puesto a “mirarla” y me gusta.

Voy a intentar hacer una compra de 1.000 $ a menos de 60…¿ Lo ves factible ?.

Gracia y salu2

Factibilísimo

Vale, lo voy a intentar.

Gracias y salu2

Acabo de comprar 20 acciones a 58,04 $

Hoy está teniendo un “subidón” bien hermoso. ¿ Tendrá alguna explicación diferente a la irracionalidad del mercado ?

Leí en reddit en un foro de cocina de que el pollo está bastante caro en los states desde hace un tiempo. La llevo de hace casi 2 años y al mirar la cotización pensé en lo pésimos que eran los análisis entonces.

Tendría que volver a mirarla pero, ¿imagino que la situación es similar a una empresa de materias primas?

Pues no me parece nada descabellada tu apreciación por muy staples que sea.

Lleva varios años haciendo suelos sobre los 57 $ ( que yo he ido aprovechando ) y techos sobre los 90 $.

A mí me encanta cuando está “por los suelos” porque su dividendo supone un yield bastante razonable y sus fundamentales son bastante sólidos.

Lo malo para mí, que busco rentabilidad por dividendos, es que cuando se va a su techo el yield se queda raquítico. Ya vendí el 19 de Enero la mitad de mi posición y seguramente venderé la otra mitad.

No sabía si ponerlo aquí o en el de humor. Parece que el muchacho se equivocó de cama…